Personal loans can beat credit cards, but debt consolidation has risks

A lower rate only helps if the new loan cuts total interest and you stop adding balances. Fees, term length and spending habits decide whether consolidation saves money.

When consolidation saves money

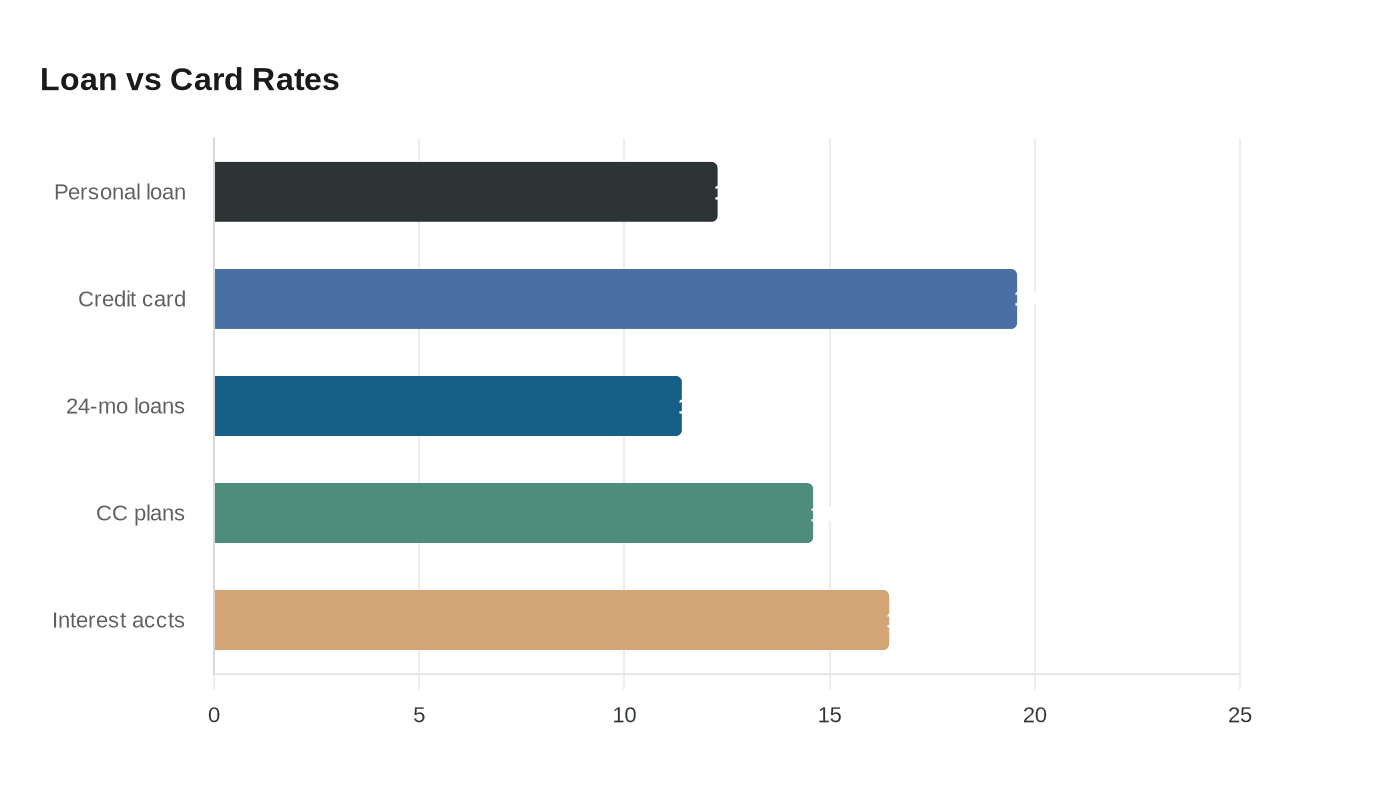

Personal loans can look like the smarter debt move right now because the rates are often lower than credit cards. Bankrate said the average personal loan rate was 12.27% on April 29, 2026, for a borrower with a 700 FICO score, a $5,000 loan and a three-year term, while the average credit card APR was 19.57% the same day. Federal Reserve consumer credit data points in the same direction, showing 24-month personal loans at commercial banks at 11.40% in February 2026, compared with 14.60% for credit card plans on all accounts and 16.45% for accounts assessed interest.

That spread matters, but only if the math works in your favor. Bankrate’s own rule of thumb is blunt: the best debt consolidation loan is one that lowers either the monthly payment or the total interest paid. If the loan merely replaces one expensive balance with a longer, still-costly payment schedule, the headline rate can hide a larger overall bill.

Start with the decision test

The first question is not whether a personal loan has a lower rate than your card. It is whether the loan lowers your total cost after fees, term length and repayment behavior are included. The Consumer Financial Protection Bureau says debt consolidation loans are one way to combine debt into one payment, but it also warns that consumers should think through the risks before moving forward.

That means looking past the monthly payment and into the full life of the debt. A shorter loan can save interest but push the monthly bill higher; a longer loan can ease cash flow but stretch the debt far beyond the point where a credit card balance might have been paid down faster. If you are carrying high-rate revolving debt, a lower-rate installment loan can be a real improvement, but only if you do not refill the cards afterward.

The checklist that decides whether it helps or hurts

A practical debt-consolidation decision comes down to four factors: your credit score, the fees, the repayment term and your discipline after the refinance.

- Credit score: Better scores generally unlock better loan pricing. Bankrate’s benchmark rate is based on a 700 FICO borrower, which is a reminder that the advertised average is not the rate everyone gets. If your score is weaker, the loan may not beat your card by enough to justify the switch.

- Fees: Many lenders charge origination fees, and NerdWallet says those can run up to about 10% of the loan amount. On a $5,000 loan, that would mean as much as $500 upfront, which can quickly erase savings if the balance is small or the term is short. A lower APR does not help much if a large fee is deducted before you even pay down the principal.

- Repayment term: The monthly payment can fall simply because the term is longer, not because the debt is actually cheaper. That is why the total interest paid matters as much as the monthly bill. A loan that looks affordable each month can still cost more over time if it keeps you in debt longer than your original cards would have.

- Spending discipline: Consolidation only works if the old balances do not come back. If you pay off cards with a personal loan and then keep charging new purchases, you end up with both the installment loan and the renewed revolving debt. At that point, the consolidation has become a delay tactic, not a solution.

Why personal loans can still be a good fit

Used carefully, a debt consolidation loan can simplify life. NerdWallet describes these loans as a type of personal loan that combines unsecured debts into one fixed monthly payment, which can make budgeting easier and reduce the chance of missing multiple due dates. For borrowers juggling several cards, the predictability of one fixed payment can be a major advantage.

They can also improve credit scores when handled responsibly. A lower utilization rate on credit cards after paying them off can help the score mix, and on-time installment payments can strengthen a payment history over time. That benefit, however, disappears if the new loan creates a cash squeeze that leads to late payments or if the borrower falls back into card debt.

When counseling may be the better route

Debt consolidation is not the only way to organize payments. The CFPB says credit counseling organizations can help with budgets and debt management plans, and those plans work differently from a loan. Under a debt management plan, the consumer makes one payment to the counseling organization each month or pay period, and the organization pays creditors.

That option can make sense when the problem is not just expensive credit, but also a broken budget. Credit counseling can add structure without taking on a new loan obligation, which may be useful if your credit profile will not qualify you for a meaningfully lower rate. It is also worth considering if the main challenge is keeping track of multiple payments rather than finding the cheapest possible refinance.

Watch the labels on the offer

The CFPB also warns that some companies advertising debt consolidation services may actually be debt settlement companies. That distinction matters because settlement is not the same as consolidation: one aims to combine debts into a single payment, while the other may encourage you to stop paying creditors while negotiations happen. The names can sound similar, but the risks and credit consequences are very different.

That is why borrowers need to verify who they are dealing with before signing anything. If a company promises easy relief but avoids clear explanations about fees, creditor payments or how the plan works, that is a red flag. The safest path is to understand whether you are being offered a loan, counseling or settlement, because each one changes your finances in a different way.

The bottom line

The numbers suggest why consolidation is appealing right now. A 12.27% personal loan rate can look far better than a 19.57% credit card APR, and the Federal Reserve’s February 2026 data shows the same basic gap. But rates alone do not decide the outcome. Fees, term length and your ability to avoid new debt decide whether the move trims costs or simply reshuffles them into a longer obligation.

If the new loan lowers either the monthly payment or the total interest paid, and you have the discipline to stop using the old cards, consolidation can work as a clean reset. If it only buys time, adds a fee and stretches repayment, the borrower may end up deeper in debt than before.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?