Tyson Foods beats earnings estimates as chicken sales offset weak beef demand

Chicken demand helped Tyson beat profit estimates, even as beef volumes fell 13.1% and the company widened its beef loss outlook. The results point to grocery shoppers trading down as meat prices stay high.

Chicken sales helped Tyson Foods clear Wall Street’s earnings bar, even as its beef business remained under heavy pressure from expensive cattle and weaker demand. The company’s shares rose about 2% in premarket trading after it reported second-quarter fiscal 2026 results showing that the protein giant’s mix of chicken, pork and prepared foods was cushioning a difficult stretch in beef.

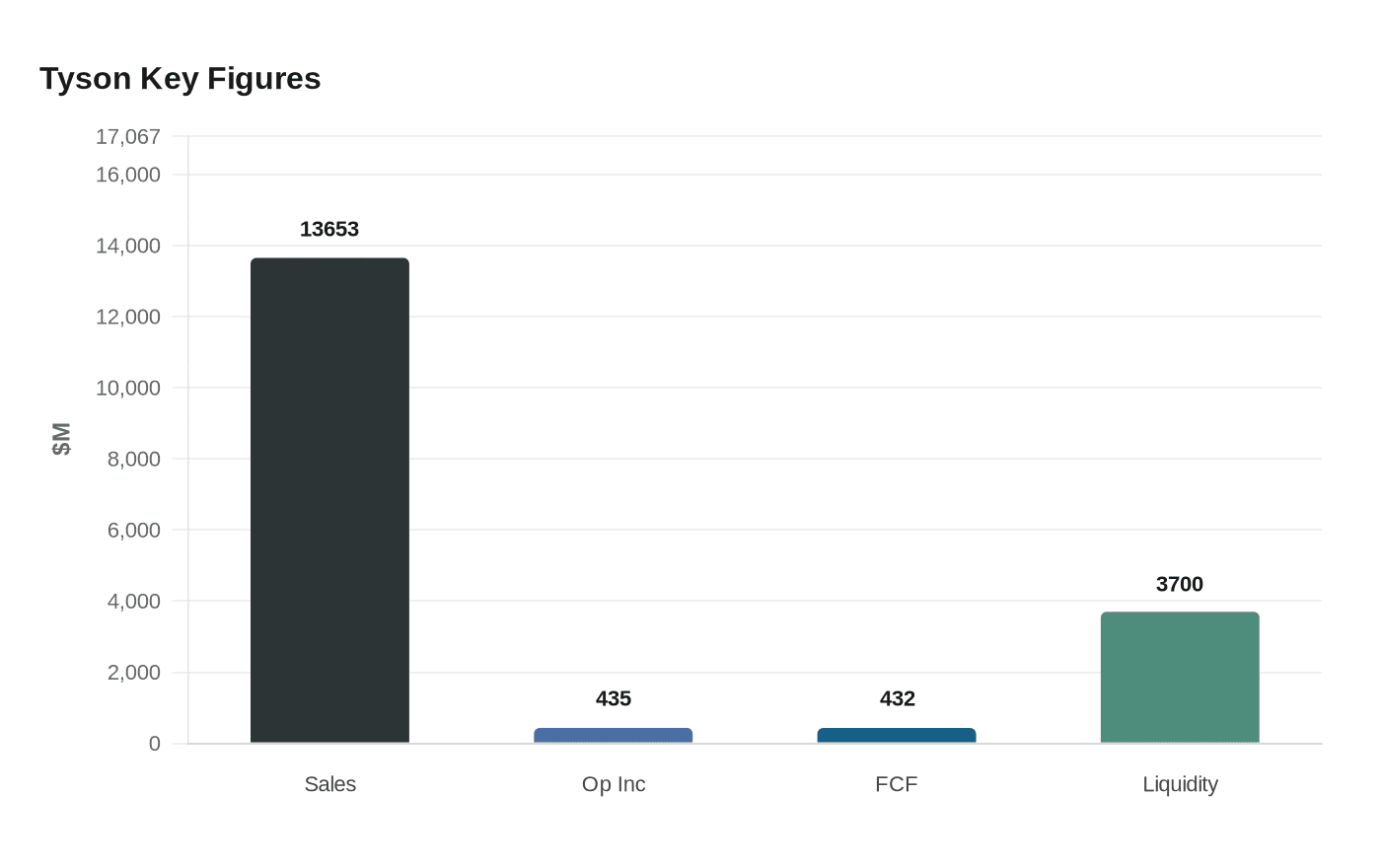

Tyson said sales in the quarter reached $13.653 billion, up 4.4% from a year earlier, while adjusted earnings per share came in at $0.87, down 5%. GAAP operating income jumped to $435 million from $100 million a year earlier. For the first half of the fiscal year, sales totaled $27.966 billion, up 4.8%, and Tyson generated $432 million in free cash flow, up $50 million from a year earlier, while reducing total debt by $747 million. Liquidity stood at $3.7 billion as of March 28, 2026. Tyson, based in Springdale, Arkansas, said it produces approximately 20% of the beef, pork and chicken in the United States and described the quarter as being driven by “Chicken and Prepared Foods Momentum.”

The underlying message from the grocery aisle is hard to miss. Tyson said consumers have shifted toward more affordable proteins such as chicken and pork as record beef prices squeeze household budgets. In the quarter, beef sales volumes fell 13.1% even as beef prices rose 11.5%, a combination that points to both supply tightness and reluctance from shoppers to pay more. Chicken volumes moved the other way, rising 1.7%, and Tyson lifted its full-year outlook for the segment, now expecting chicken adjusted operating income of $1.9 billion to $2.05 billion. The company also projected prepared foods adjusted operating income of $1.25 billion to $1.35 billion, pork at $250 million to $300 million and international at $150 million to $200 million.

Beef remains the weak spot. Tyson now expects an adjusted operating loss of $350 million to $500 million for fiscal 2026 in that division, worse than its earlier guidance. That forecast lands against a cattle market still distorted by drought-era herd losses and a U.S. cattle and calf inventory of 86.2 million head on Jan. 1, 2026, the lowest since 1951. Tyson’s decision in November to permanently close its Lexington, Nebraska beef plant, which employed roughly 3,200 people and could slaughter almost 5,000 cattle a day, showed how deep the pressure runs. For now, chicken is doing the work of protecting Tyson’s earnings, but the broader signal is clearer: inflation has changed what many Americans can afford to put in the cart, and beef is losing ground.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?