Eastern England's Pastoral Fields Offer Escape From Distant Iran Conflict

A war 3,500 miles away is reshaping what gets planted in England's potato belt this spring, through a chain of diesel shocks, fertilizer scarcity, and spiking ship insurance premiums.

The flat, fertile expanse of Lincolnshire in early April carries the scent of turned soil and the low rumble of tractors beginning another potato season. Cambridgeshire, Norfolk, and Suffolk share that same unhurried rhythm. Together, these eastern counties lead the United Kingdom in potato output, and the industry they anchor is worth £2 billion a year. The landscape looks, by any romantic measure, insulated from the world: ancient hedgerows, wide skies, the kind of pastoral scene that has drawn painters and poets for centuries.

But trace the cost of every input going into that ground in spring 2026 and a very different picture emerges. The Strait of Hormuz, a narrow waterway roughly 3,500 miles from Lincolnshire, was nearly entirely closed after the United States and Israel attacked Iran on 28 February 2026. What followed was, by most assessments, possibly the largest supply disruption in the global oil market on record. The consequences did not stay in the Gulf.

The First Shock: Red Diesel

On a working arable farm, fuel is the first bill you feel when oil prices move. Red diesel powers every tractor, combine, and irrigation pump on the farm, and it is metered in vast quantities across a single planting season. Since the end of February, red diesel prices have jumped roughly 70%, rising from around 69 pence per litre before the conflict to approximately 117 pence per litre as global oil prices held above $100 a barrel. Across the wider road fuel market, diesel for road vehicles rose 29 pence per litre, around 20%, in the five weeks between 28 February and 23 March alone, according to a House of Commons Library analysis.

The Energy and Climate Intelligence Unit calculated that UK farmers, in aggregate, face a £337 million surge in fuel costs from this single shock. Using data from the Office for National Statistics, which captures higher consumption levels across agriculture, forestry and fishing combined, the total additional burden for those sectors may exceed £1 billion across the full year. Eastern England's potato belt, with its heavy mechanisation and large farm footprints, sits squarely in the highest-exposure bracket.

The Input That Cannot Be Easily Substituted: Nitrogen Fertilizer

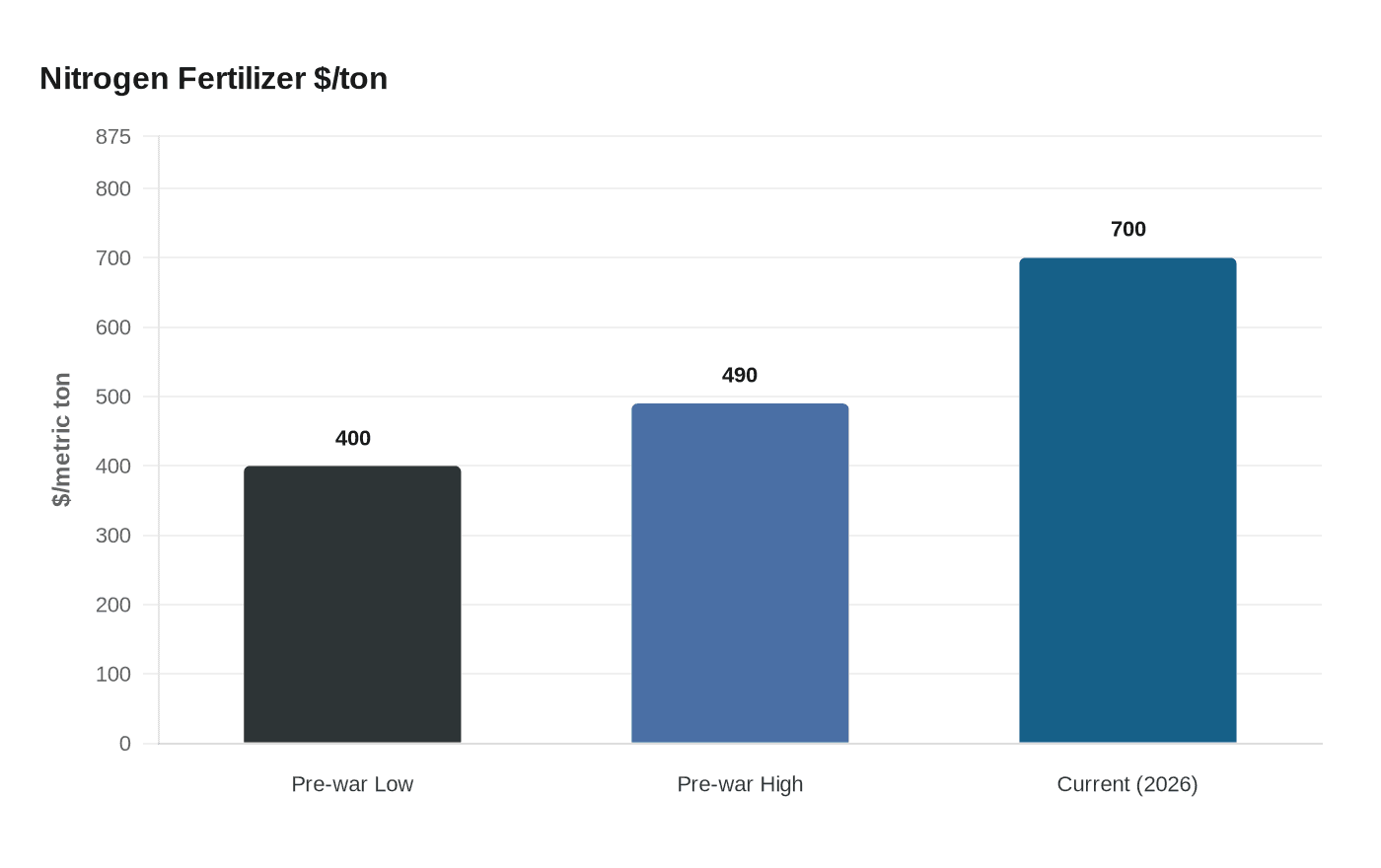

If diesel is the first shock, fertilizer is the deeper one because there is no ready workaround. Potato crops are among the most nitrogen-intensive in arable farming, requiring precise applications timed to each growth stage. Before the current conflict, nitrogen fertilizer was already expensive: prices had risen more than 30% between 2021 and 2023, compressing margins before any grower had heard of the 2026 Straits crisis.

Now the situation is structurally worse. Around one-third of all internationally traded fertilizers, particularly nitrogen-based products, normally transit the Strait of Hormuz, according to the United Nations. Gulf countries, including Saudi Arabia, Qatar, the United Arab Emirates, Kuwait, and Iran itself, are critical hubs in the global fertilizer supply chain. Nitrogen fertilizers depend on natural gas as both a feedstock and an energy source: the process burns gas at high pressure in the presence of hydrogen to synthesize ammonia. With Gulf gas and oil locked behind a closed strait, both the product and the raw material for making it elsewhere have become scarcer simultaneously.

The price consequence has been severe. Nitrogen fertilizer has reached $700 per metric ton globally, up from a pre-war range of $400 to $490. For a Lincolnshire potato grower ordering several hundred tonnes across a season, that gap runs to tens of thousands of pounds in additional cost per farm, applied to a crop whose supermarket price is notoriously difficult to push upward without consumers simply reaching for a cheaper alternative.

Shipping Insurance: The Hidden Multiplier

A less visible but compounding factor is the cost of war-risk ship insurance. Before tensions escalated to their current level, insurers charged 0.125% of the ship's insurance value per transit through the Strait. As military operations intensified, that premium climbed to between 0.2% and 0.4% per transit. The percentage points sound small but, applied to the value of a supertanker or a bulk fertilizer carrier, they add meaningfully to the landed cost of every tonne of cargo. Shipping firms pass those premiums to buyers. Buyers, in this case fertilizer importers and ultimately farmers, absorb them through higher invoice prices.

For UK farmers trying to price their 2026 crop contracts, this creates an unusual problem: fertilizer costs are not only higher than any historical baseline, they are volatile in ways that defeat normal forward planning. Contracts locked in before February now look like bargains. Those purchasing on spot markets face costs that can shift within weeks depending on whether peace talks move forward, whether alternative shipping routes through the Cape of Good Hope add further delays, or whether Gulf producers find ways to reroute supply.

Planting Decisions Under Pressure

The knock-on effect on what actually goes into the ground is already visible in the data. Smaller potato growers, particularly those without long-term supply contracts with major retailers, are weighing whether the arithmetic of planting justifies the risk. When diesel, fertilizer, and financing costs all rise at once, the break-even yield needed to cover inputs rises sharply. At the same time, the Bank of England, which had been expected to cut interest rates in 2026, now faces a stagflationary dilemma: rate cuts anticipated before February have effectively been shelved, and rate hikes are now considered possible according to the House of Commons Library briefing. For farmers carrying equipment loans or overdrafts tied to variable rates, that prospect adds a fourth pressure on top of fuel, fertilizer, and insurance.

The result is a quiet reshaping of planting decisions: some growers are cutting acreage, others are seeking to renegotiate supply contracts, and others are holding off on capital investments that would have improved efficiency in subsequent seasons.

What It Means at the Checkout

Potato prices in UK supermarkets have historically been one of the most stable lines in the weekly shop, kept low by competition and domestic overproduction. That buffer is narrowing. The UK has grown increasingly reliant on imported potato products, particularly frozen chips and processed goods, which travel longer supply chains and carry the full weight of elevated shipping costs. As domestic growers face margin pressure, acreage contractions feed through to tighter supply, and retailers eventually face a choice between absorbing cost increases or passing them on.

The implications are not contained to Britain. Global fertilizer shortages driven by the Hormuz closure are affecting every nation that imports nitrogen-based products, from Brazil's soy belt to Sudan's smallholder farms to Sri Lanka's rice paddies. In that sense, eastern England's potato fields are not a refuge from the conflict at all; they are simply one of the more visible stress-test points in a supply chain that wraps around the planet. The pastoral calm of April planting season in Lincolnshire sits directly downstream of decisions made in Tehran, Washington, and Tel Aviv, filtered through diesel pumps, fertilizer brokers, and marine insurance desks.

The fields look the same as they always have. The economics underneath them do not.

Sources used in reporting: House of Commons Library briefing CBP-10601; Energy and Climate Intelligence Unit analysis; FarmingUK; Carnegie Endowment for International Peace; UN figures cited via the 2026 Strait of Hormuz crisis; University of Cambridge agriculture research; PotatoPro UK market data.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?