Energy markets brace for life beyond the Strait of Hormuz

Even if Hormuz stays open, oil markets are learning to work around it, with shippers, buyers, and states hedging against a chokepoint that still moves 20 million barrels a day.

The Strait is still huge, but its leverage is not fixed

The market’s most important oil chokepoint is no longer being treated as a single point of failure. Even if the Strait of Hormuz remains open, traders, shippers, and producers are increasingly acting as though they need a plan for life beyond it.

That shift matters because the strait is still enormous in global terms. In 2024, about 20 million barrels per day of oil flowed through it, equal to roughly 20% of global petroleum liquids consumption. It remains the primary export route for Saudi Arabia, the United Arab Emirates, Kuwait, Qatar, Iraq, Bahrain and Iran, and the bulk of the oil that leaves the strait heads to Asia, especially China, India and Japan.

Yet the strategic meaning of that traffic is changing. The market is not abandoning Hormuz, but it is learning how to reduce dependence on it, one pipeline, one cargo route, and one stockpile decision at a time.

Why the chokepoint still frightens energy markets

Hormuz remains central because the world’s spare oil cushion is not spread evenly. The International Energy Agency warns that a prolonged disruption could remove much of the world’s spare production capacity, most of which sits in Saudi Arabia. That means a blockage would do more than interrupt tanker traffic. It would also strike at the reserve capacity that helps keep prices stable when the market tightens.

The U.S. Energy Information Administration says flows through Hormuz were still relatively flat in the first quarter of 2025 compared with 2024, a reminder that the world has not yet escaped its dependence on the route. The scale of the risk is easy to see in price moves. In one recent flare-up, Brent crude climbed from $69 a barrel on June 12 to $74 a barrel on June 13, a sharp reminder of how quickly shipping risk can be repriced.

The deeper fear is not just that oil is delayed. It is that the market will be forced to treat every tanker, terminal, and insurance policy in the region as a geopolitical wager.

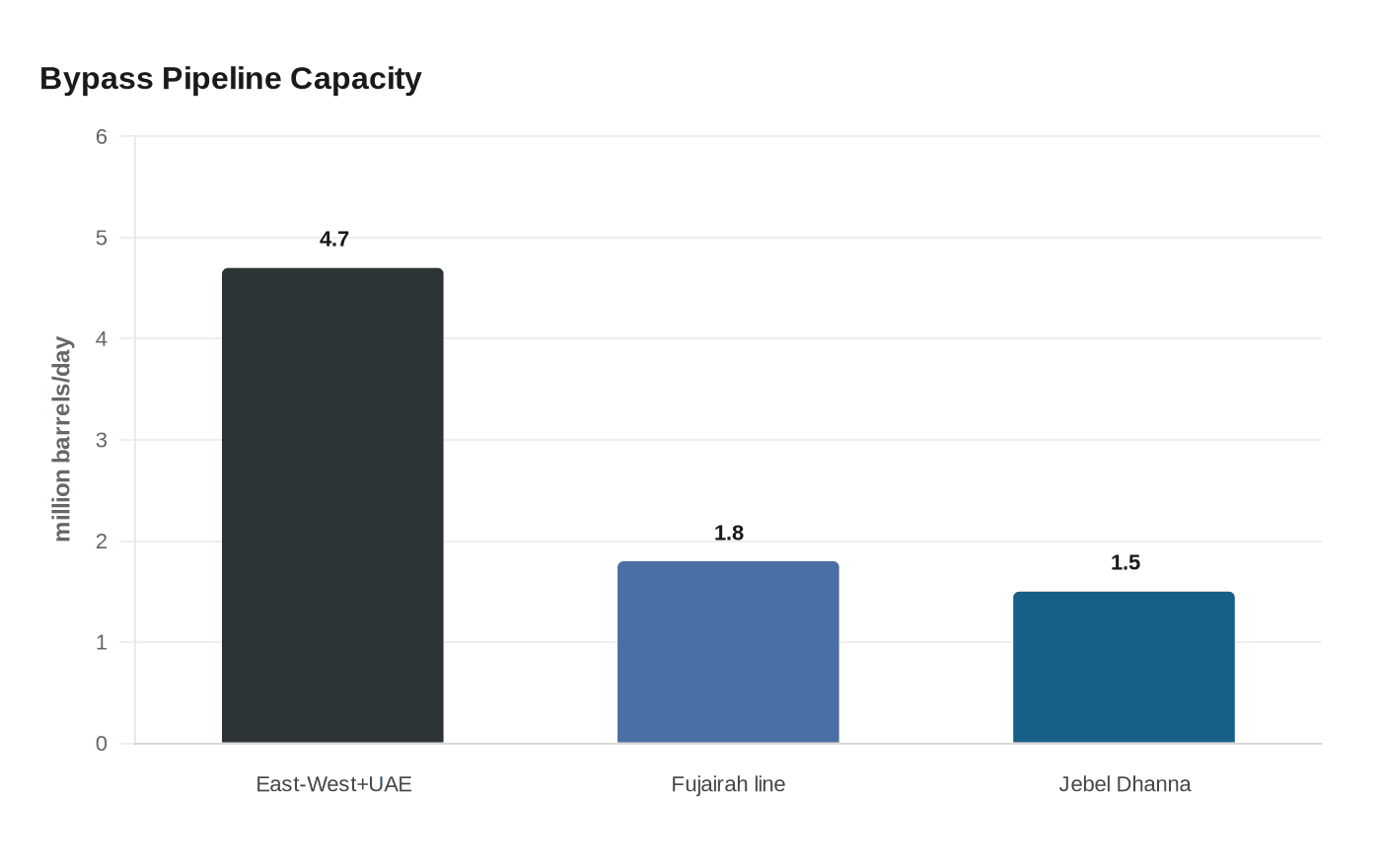

The rerouting map is growing, but it is still small

The alternative route network is expanding, but it remains limited compared with the volume that passes through Hormuz. The U.S. Energy Information Administration says Saudi Aramco’s East-West crude pipeline and the United Arab Emirates’ Abu Dhabi pipeline together can provide about 4.7 million barrels per day of bypass capacity in a disruption. The UAE already has an existing bypass line to Fujairah with capacity of 1.8 million barrels per day, and it plans another 1.5 million barrels per day pipeline from Jebel Dhanna to Fujairah by 2027.

Those numbers matter because they show where the market is putting its money: not in the fantasy of eliminating risk, but in building enough flexibility to survive it. The bypasses do not come close to replacing the full 20 million barrels per day that move through the strait, yet they do give large producers an outlet that can blunt the impact of a crisis and reduce the leverage of any one disruption.

There is also evidence that cargo patterns are already shifting. Between 2022 and 2024, crude oil and condensate transiting the strait fell by 1.6 million barrels per day, partly offset by a 0.5 million barrels per day increase in petroleum product cargoes. That is a sign of adaptation: the corridor is still vital, but the composition of what moves through it is changing.

Shippers, traders and governments are pricing risk differently

The change is not only physical, it is financial. Traders are increasingly factoring in war risk, tanker availability, insurance costs, and the possibility of temporary rerouting when they set prices. Shippers are looking harder at alternative load points and discharge options, while buyers are under more pressure to diversify supply and avoid relying too heavily on a single passage.

Policy is moving in the same direction. The International Energy Agency says its member countries are carrying out the largest-ever oil stock release amid Middle East market disruptions, a sign that strategic reserves remain one of the few tools capable of calming a sudden shock. Analysts and industry sources are also focusing on demand restraint, because in a tight market the fastest relief often comes from lower consumption, not just more supply.

That reaction is not abstract. The IEA says the conflict that began on February 28, 2026 created the largest supply disruption in the history of the global oil market, reduced global LNG supply by around 20%, and pushed some oil prices above $100 per barrel. For markets, the lesson is blunt: the risk is no longer theoretical, and gas can be pulled into the same geopolitical shock even when the immediate flashpoint is oil.

History still shapes every new crisis

The modern benchmark for a Hormuz crisis is the Tanker War of the 1980s. From 1981 to 1988, attacks on merchant shipping in the Persian Gulf and near the Strait of Hormuz turned the waterway into a war zone. Hundreds of ships were attacked and more than 100 merchant sailors were killed, a toll that still anchors market memory whenever tensions rise.

That history matters because it shows how quickly commercial traffic can be militarized, and how hard it is to restore confidence once shipping lanes are seen as targets. Even if cargoes keep moving, freight markets can seize up if insurers, captains, and charterers decide the risk has become unmanageable.

What life beyond Hormuz means for Gulf states and Iran

For Gulf producers, the long-term trend is both protective and limiting. New pipelines, stockpiles and route diversification reduce the damage from a single shock, but they also erode the chokepoint leverage that once gave the region outsized influence over global prices. Saudi Arabia and the UAE can still project supply flexibility, yet the more the market can bypass Hormuz, the less any one closure can dictate outcomes.

For Iran, that is a strategic problem. The strait has long been one of Tehran’s most potent sources of indirect leverage, even when it could not fully control the flow itself. If buyers, shippers and governments keep investing in rerouting and stockpiling, the threat of disruption becomes less powerful as a bargaining tool.

That is the structural shift now underway. Hormuz is still indispensable, but it is no longer the only answer the market is preparing to use. The energy system is being rebuilt for a world where the strait may remain open, but no one wants to depend on that assumption.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?