Honeywell Aerospace targets $6.5 billion in earnings by 2030

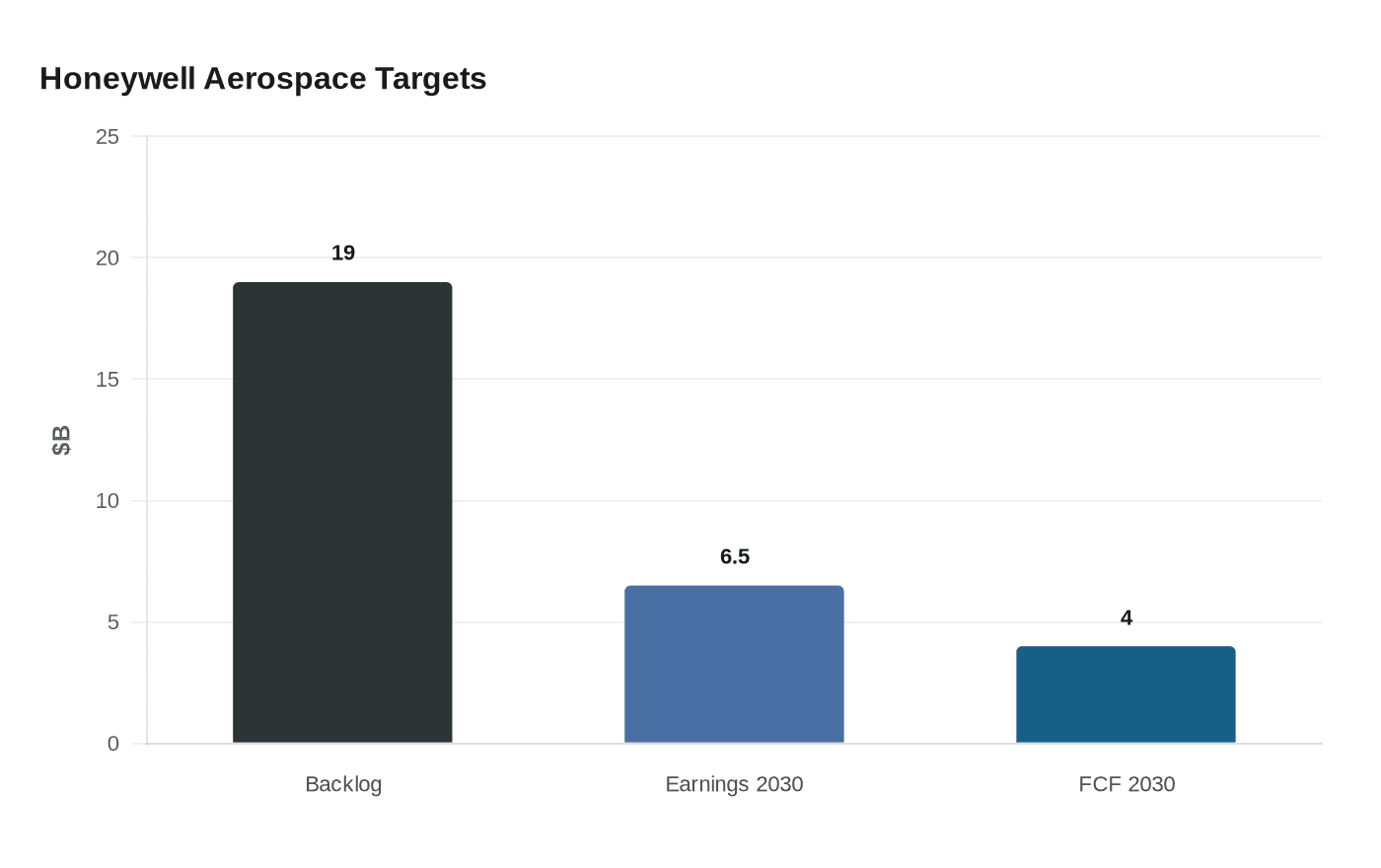

Honeywell Aerospace says it can turn a $19 billion backlog into $6.5 billion in adjusted earnings by 2030, testing whether a pure-play can outrun a conglomerate.

Honeywell Aerospace is betting that breaking away from Honeywell International will do more than tidy up the corporate chart. It wants investors to believe a stand-alone aerospace supplier can grow faster, spend more selectively and earn a premium for operating as a focused industrial company rather than a division inside a sprawling conglomerate.

At an investor day in Phoenix, Arizona, Honeywell said the aerospace business expects $6.5 billion in adjusted earnings by 2030 and will trade on Nasdaq under the ticker HONA when the separation closes on June 29. The automation business will keep the HON ticker and become Honeywell Technologies. Management says the split is meant to simplify decision-making and allow capital to be directed toward factories, suppliers and capacity instead of leaning on shareholder payouts.

That is the core wager: Jim Currier, the aerospace chief executive, said the company wants to reinvest where demand is strongest because the payoff from meeting orders is better than emphasizing dividends or buybacks. Honeywell is also pitching the new company as one of the largest publicly traded pure-play aerospace suppliers, with a strategy built around innovation, operational excellence and its “develop once, deploy everywhere” approach.

The numbers behind the pitch are solid, but the stretch to 2030 will still be judged against the realities of commercial aviation and defense spending. Honeywell said the backlog has reached about $19 billion, up 20% from a year earlier, with orders up 28% over the past 12 months and a book-to-bill ratio of 1.1. For 2026, the company expects sales growth of 7% to 9%, adjusted EBIT of $4.6 billion to $4.7 billion and second-half free cash flow of $1 billion to $1.5 billion. Longer term, it is targeting annual sales growth of 6% to 8% and more than $4 billion in free cash flow by 2030.

Honeywell is leaning hard on two markets that have held up despite broader uncertainty: jetmakers and defense customers. In March, it announced a framework agreement with the Pentagon tied to a $500 million investment to expand production of defense technologies, a deal Currier cited as evidence that a leaner structure can move faster on major customer programs. The company also points to a century-plus aviation heritage that traces back to the first autopilot demonstration in 1914, then through auxiliary power units, digital cockpits and runway safety systems.

The spinoff also fits a larger American industrial pattern. GE Aerospace showed that a narrower structure can give investors a cleaner story and sharper metrics. Honeywell is making the same argument, but it still has to prove that a newly independent aerospace supplier can scale manufacturing quickly enough to capture demand without getting squeezed by supply-chain bottlenecks. If it can, the breakup may look less like a corporate rearrangement than a bet that specialization now pays better than size.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip