Mortgage rates ease, Freddie Mac says buying and refinancing activity picks up

A 6.30% 30-year mortgage lowers a $400,000 loan payment by about $135 a month versus a year ago, while Freddie Mac says purchase and refinance demand is picking up.

A 6.30% 30-year mortgage changes the monthly math in a real way. On a $300,000 home with 20% down, the principal-and-interest payment is about $1,486 a month, and on a $400,000 home it is about $2,476. Both are lower than they would have been a year ago, when the same loan would have carried a 6.81% rate and cost roughly $1,566 on the smaller loan and $2,610 on the larger one.

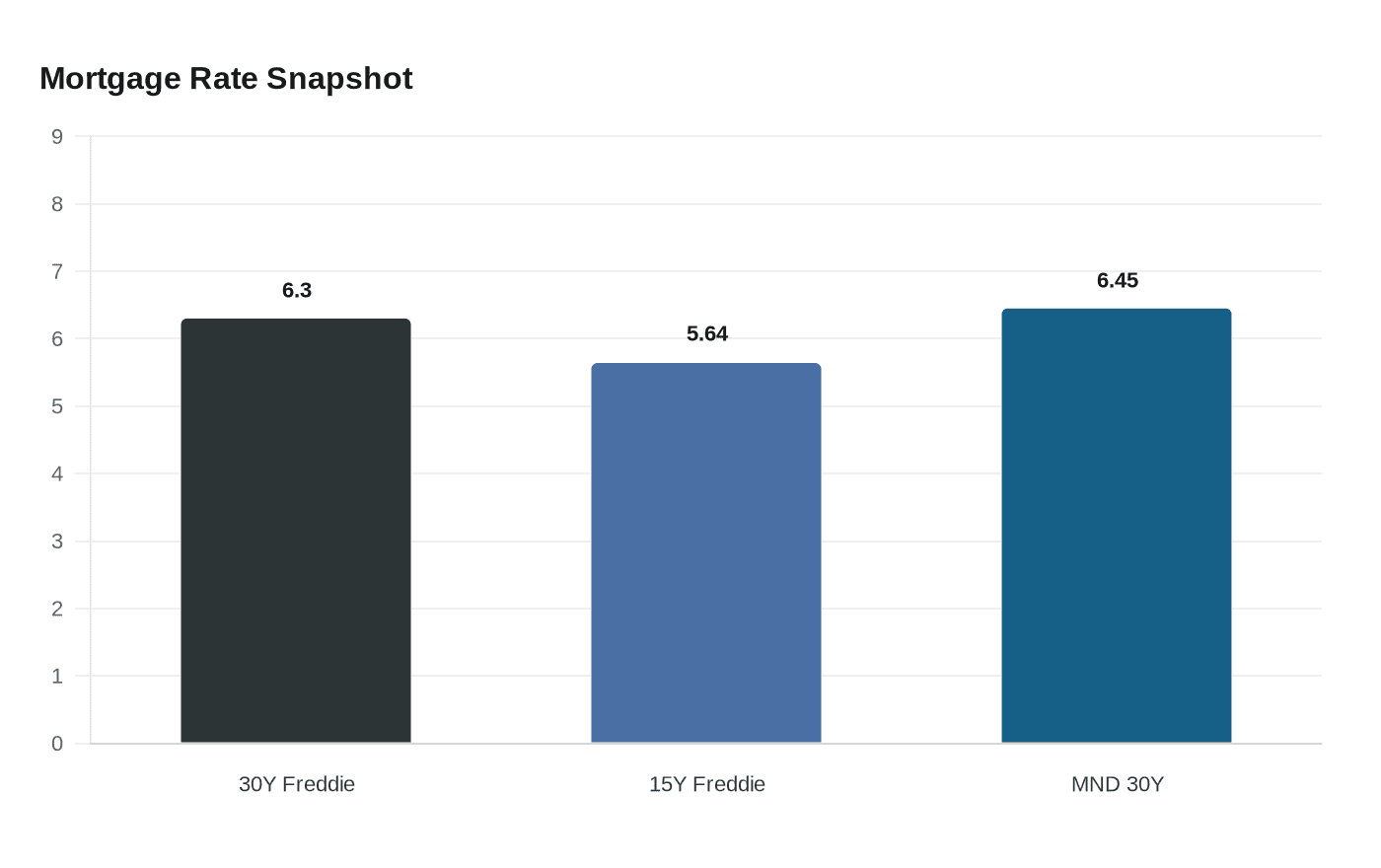

Freddie Mac said the 30-year fixed-rate mortgage averaged 6.30% as of April 30, 2026, while the 15-year fixed-rate mortgage averaged 5.64%. Its public archive showed the 30-year rate at 6.23% as of April 23, down from 6.30% the week before, and 6.81% a year earlier. Mortgage News Daily’s national average for the 30-year loan stood at 6.45% on April 30, a reminder that rate trackers can differ even when they are pointing in the same general direction.

The easing in borrowing costs has already started to show up in the housing market. Freddie Mac said lower rates arrived alongside a pickup in purchase applications and refinance activity, plus an increase in monthly pending home sales, a combination the company said points to improving momentum. For buyers, that matters because rate moves of even a few tenths of a point can change whether a household qualifies for a loan, or how much room it has left after taxes, homeowners insurance, mortgage insurance and closing costs.

Freddie Mac’s Primary Mortgage Market Survey is based on loan applications submitted by lenders across the country and is released weekly on Thursdays at 12 p.m. ET. Its mortgage-rate archive runs back to 1971, giving borrowers a long record to measure today’s numbers against.

The clearest buyers are those who are ready to move and have already found a payment they can live with, because waiting for a better headline rate can mean losing the house or the rate. Refinancers face a different test: the new loan needs to be low enough to pay back closing costs in a reasonable time. A borrower with a $240,000 balance would pay about $1,486 a month at 6.30% on a 30-year term, compared with about $1,979 on a 15-year loan at 5.64%, so the shorter loan can build equity faster but leaves far less breathing room in the monthly budget.

For households near the margin, the rate matters, but the full bill matters more. The move from 6.81% to 6.30% improves affordability, yet the final decision still turns on down payment, fees and how long the borrower expects to stay in the home.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?

%3Amax_bytes(150000)%3Astrip_icc()%2FCertificate-of-deposit-2301f2164ceb4e91b100cb92aa6f868a.jpg&w=1920&q=75)