Mortgage rates rise again, squeezing affordability for homebuyers

Mortgage rates climbed to 6.52%, keeping buyers and would-be sellers sidelined as first-time affordability stays stretched and inventory remains tight.

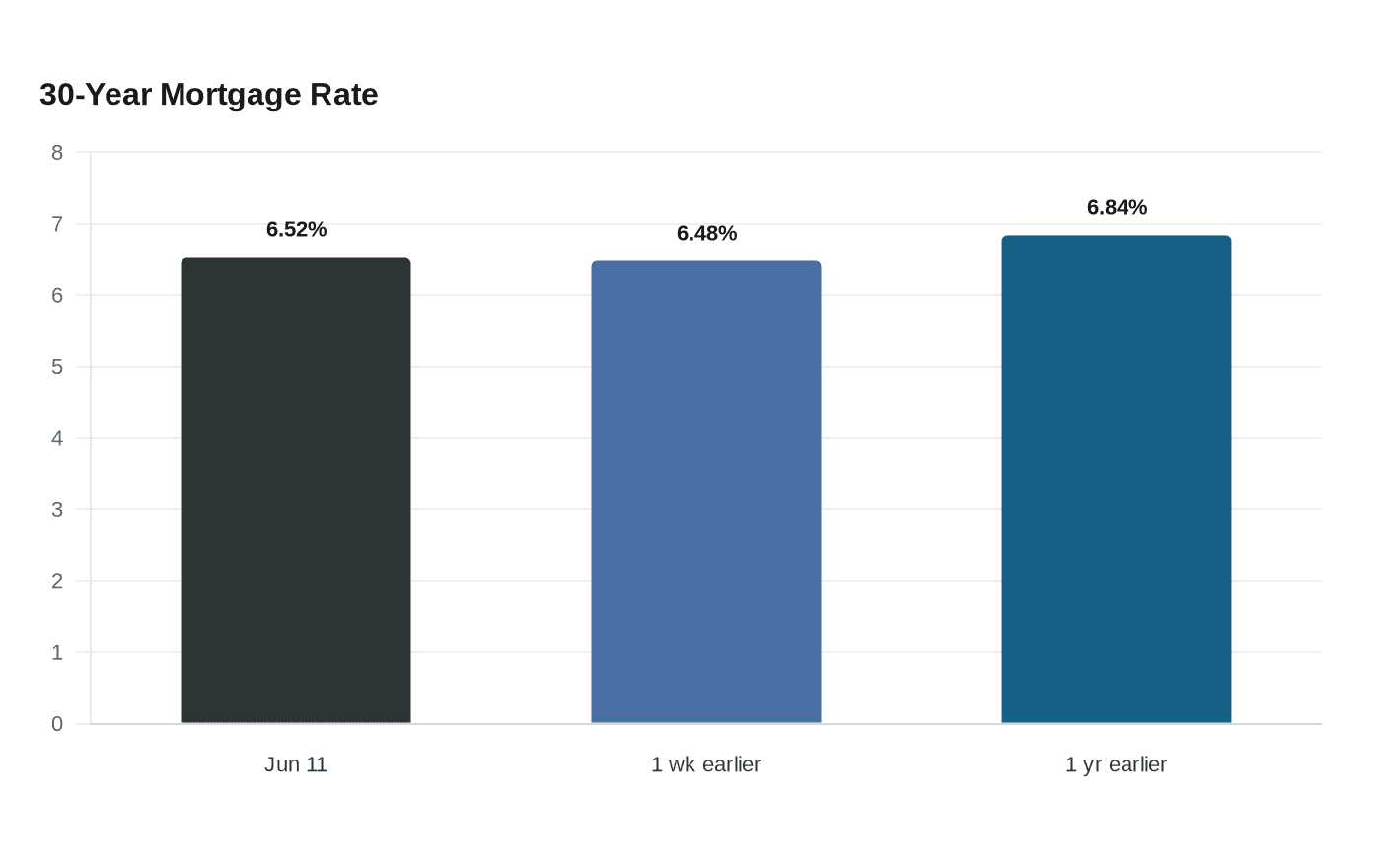

Mortgage rates edged higher again, deepening the lockout that is freezing both buyers and would-be sellers and tightening supply as much as affordability. Freddie Mac said the average 30-year fixed mortgage rose to 6.52% on June 11 from 6.48% a week earlier, while the 15-year rate climbed to 5.84% from 5.79%.

That leaves borrowing costs just below their highest level of the year and well above the rate environment that powered the pandemic-era buying rush. Freddie Mac said the 30-year average was 6.84% a year earlier, while the 15-year rate stood at 5.97%. Rates briefly slipped under 6% in late February, the first time since late 2022, but they have not returned below that threshold. Higher borrowing costs can add hundreds of dollars a month to ownership expenses, and the pressure is still filtering through the market.

The backdrop is an elevated bond market. Mortgage rates generally track the 10-year Treasury yield, and that yield was 4.53% in midday trading Thursday, up from 4.47% a week earlier and far above 3.97% before war broke out in late February. War-driven energy costs and inflation have kept long-term yields elevated, making investors demand more return and pushing mortgage costs higher.

Some buyers are still moving. Freddie Mac chief economist Sam Khater said stronger employment momentum helped existing-home sales reach a five-month high, and the National Association of Realtors reported that existing-home sales rose 3.2% in May to a seasonally adjusted annual rate of 4.17 million, the highest level of 2026. But the market remains tight. Unsold inventory stood at 1.55 million units, equal to 4.5 months’ supply, and the median existing-home price rose to $429,300, up 1.3% from a year earlier.

Affordability remains the central constraint. The National Association of Home Builders said that in the first quarter of 2026, a family earning the nation’s median income of $106,800 needed 32% of its income to cover the mortgage payment on a median-priced home. That leaves first-time and entry-level buyers under the most strain, even as households with stronger income, steady employment and existing equity keep participating. For the broader housing market, the message is clear: until rates move materially lower, inventory will remain restrained and monthly payments will stay far above pre-pandemic norms.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip