Sealed Air Goes Private in $10.3 Billion CD&R Acquisition Deal

The maker of Bubble Wrap and CRYOVAC food films went private Thursday as CD&R's $10.3 billion deal closed, financed by $7.9 billion in new acquisition debt.

Sealed Air Corporation, the Charlotte-based packaging group behind Bubble Wrap and CRYOVAC food films, completed its $10.3 billion take-private on April 9, 2026, with investment funds affiliated with Clayton, Dubilier & Rice closing the deal and removing the company's shares from the New York Stock Exchange.

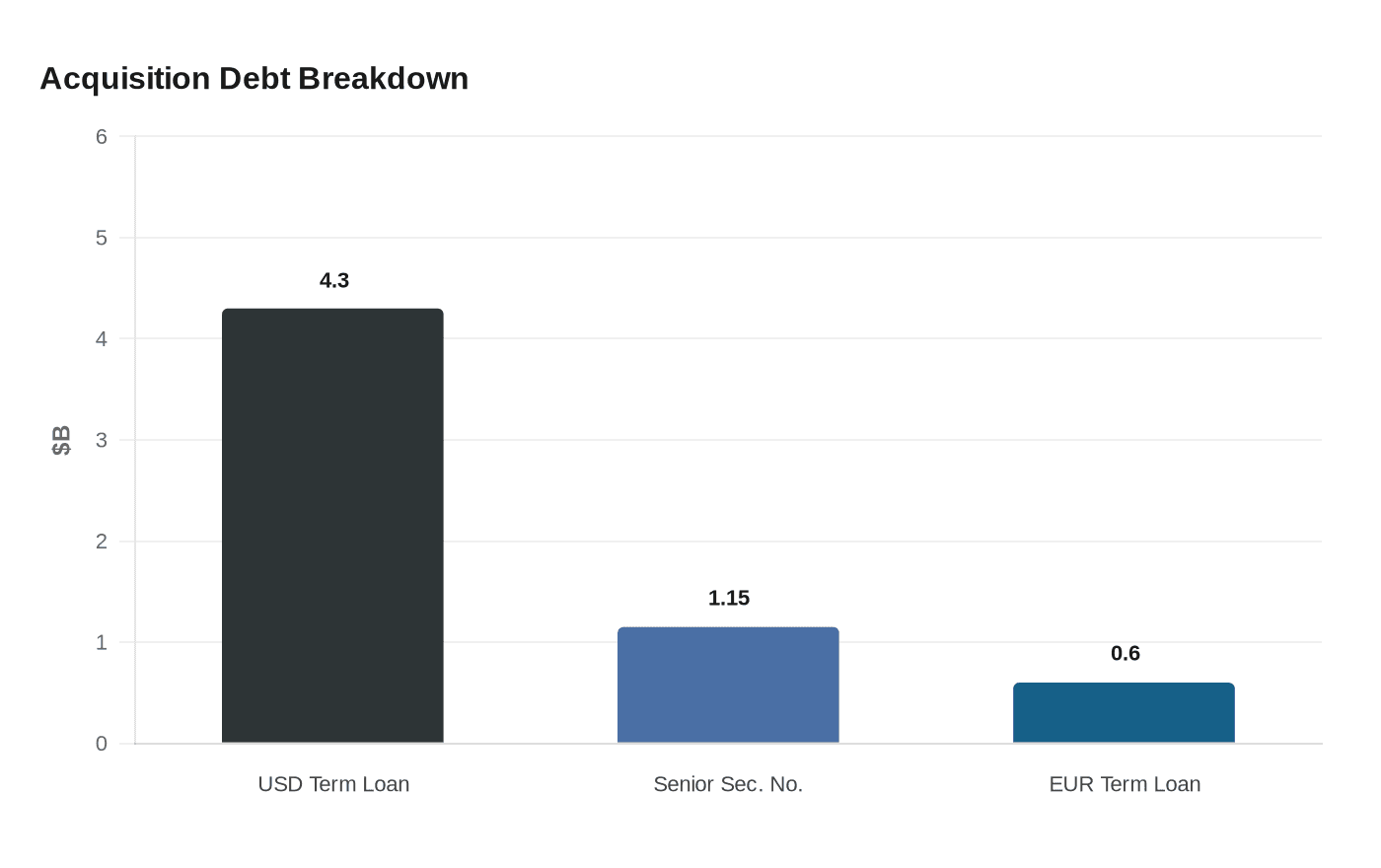

Public shareholders received $42.15 per share in cash, a premium to recent trading, for aggregate equity consideration of roughly $6.3 billion. Banks structured approximately $7.9 billion in debt to finance the acquisition, built around a U.S. dollar term loan of about $4.3 billion, a euro-denominated term loan of roughly $600 million, and $1.15 billion in senior secured notes. The new financing compares starkly with the $3.7 billion in net debt Sealed Air carried entering the deal at a 3.2 times net leverage ratio; post-close debt service obligations will be substantially heavier.

CEO Dustin Semach described the transaction as the start of "an exciting new chapter," saying CD&R would back growth initiatives across both the Food and Protective Packaging segments. The framing is standard for take-privates: freedom from quarterly earnings pressure unlocks long-term investment. The more pressing question for the company's approximately 16,400 employees and the food producers, retailers, and parcel carriers who rely on its materials is whether that investment precedes or follows restructuring moves to service elevated debt costs.

Sealed Air generated $5.4 billion in 2025 sales across operations in 117 countries. Its Food segment, anchored by CRYOVAC meat and dairy films used across the protein supply chain, is the more profitable of its two divisions. The Protective segment, which includes Bubble Wrap-branded materials used in e-commerce and industrial shipments, posted a 2% full-year sales decline in 2025 and represents the more obvious candidate for margin improvement under new ownership.

CD&R, founded in 1978 and headquartered in New York, has a track record of industrial operational overhauls. The firm carved Lexmark out of IBM's printer and keyboard manufacturing business in 1990 and acquired Borg-Warner's Industrial Products Division in 1987, restructuring it into the standalone company BW/IP International. Those precedents suggest a model that blends targeted capital investment with hard efficiency gains rather than simple financial engineering, though the scale of acquisition debt will demand meaningful earnings expansion regardless of strategy.

For companies shipping perishable proteins or high-value goods, Sealed Air's private ownership could accelerate automation investment and materials development in a sector facing intensifying sustainability and regulatory pressure. It could also introduce pricing shifts and supply disruptions if cost targets drive plant consolidation. The company's reach across 117 countries makes either outcome consequential far beyond any single market.

S&P Dow Jones Indices replaced Sealed Air in the S&P SmallCap 600 effective the morning after closing. Stockholder approval cleared in February 2026, and the European Commission granted regulatory clearance on March 23, determining the transaction posed no competition concerns. CD&R now controls pricing, capital allocation, and potential consolidation moves across a company whose materials wrap a significant share of the American food supply and move through every major logistics network in the world.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?