SpaceX IPO filing reveals tangled financial ties across Musk's empire

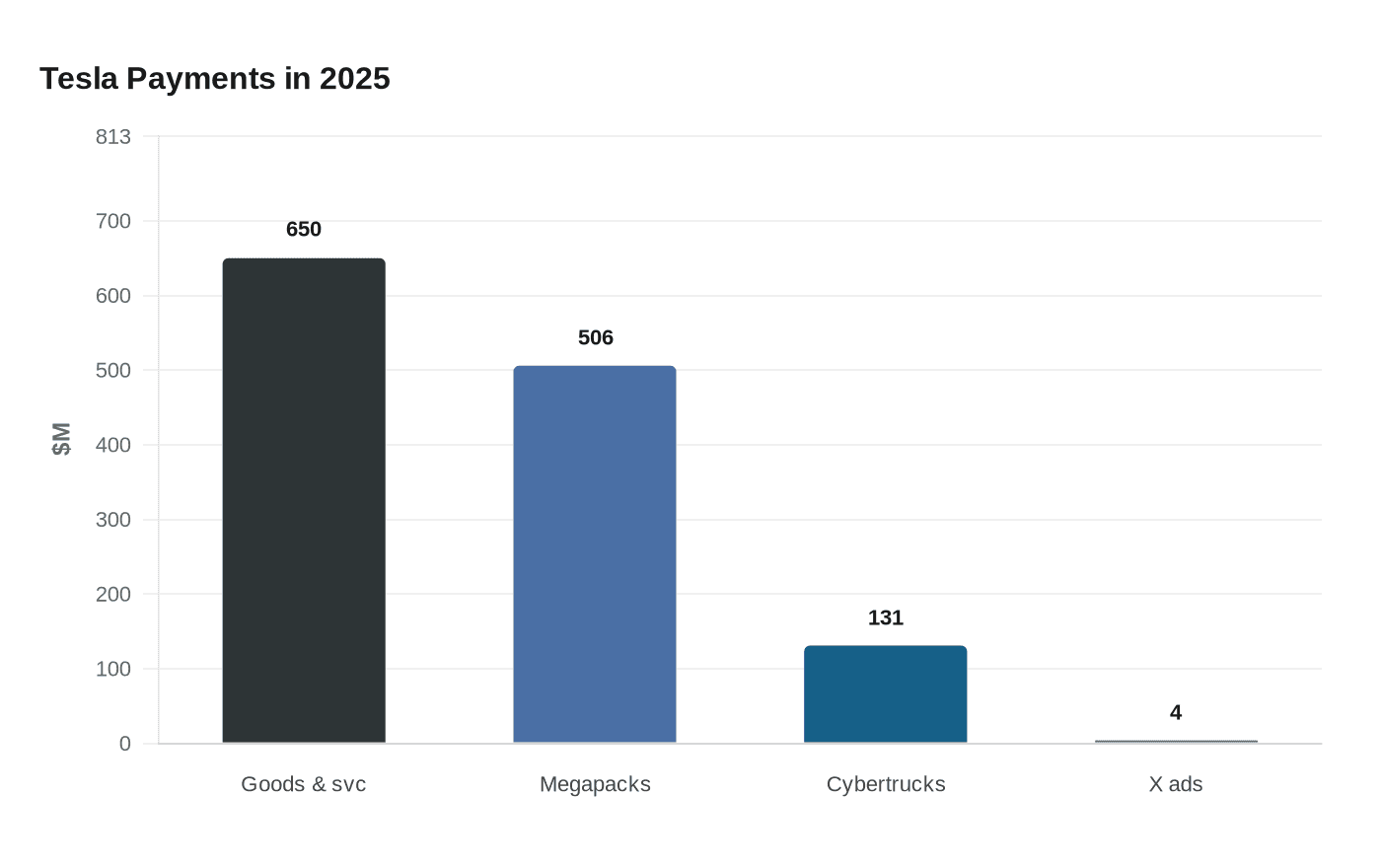

SpaceX’s filing put Musk’s web of deals on paper: Tesla bought $650 million in goods from SpaceX and xAI, while investors also face Musk’s legal baggage.

The biggest risk in SpaceX’s public debut is not just valuation, but control. The filing laid out how deeply Elon Musk’s companies are intertwined, giving ordinary investors a clearer view of a business whose fortunes can be shaped by Musk’s behavior, politics, legal troubles and capital allocation choices as much as by rocket launches.

SpaceX’s IPO filing showed that SpaceX and its xAI subsidiary bought about $650 million in goods and services from Tesla in 2025, including $506 million in Megapack battery systems and $131 million in Cybertrucks. Tesla also paid $4 million for advertising on X in 2025, while Tesla held nearly 19 million shares of SpaceX Class A stock after a $2 billion investment that later converted into SpaceX equity during Musk’s corporate restructuring.

The filing also pointed to more complicated ties. Reuters reported aircraft-sharing arrangements involving Tesla and Musk personally, security payments to a private company owned by Musk, and more than $20 billion in related-party artificial intelligence infrastructure lease obligations tied to equipment agreements between subsidiaries linked to xAI and private investment firm Valor Equity Partners. SpaceX and Tesla are also working on a multibillion-dollar joint project called Terafab, part of a broader push to pair SpaceX’s satellite and launch business with Musk’s artificial intelligence ambitions.

For investors, those ties matter because SpaceX is being pitched as more than a space company. The company is increasingly framed as an AI and compute infrastructure play, with reporting that Tesla is building a solar factory to supply custom photovoltaic hardware for SpaceX’s planned constellation of orbital AI data centers. That broader story helps explain why the offering is said to target a valuation of about $1.75 trillion and could raise about $80 billion, a scale that would make it the largest stock market debut in history if completed.

But the concentration risk is obvious. University of Florida finance professor Jay Ritter told Forbes that the “Elon Musk effect” could boost demand for the IPO while also increasing long-term volatility. He also warned that even if Starlink generates tens of billions of dollars in profit, Musk could steer resources toward Mars rather than shareholders.

Regulatory scrutiny adds another layer. The Securities and Exchange Commission said in May 2026 that it had filed an amended complaint and proposed final judgment against Musk’s revocable trust in the Twitter disclosure case, with a $1.5 million civil penalty proposed. SpaceX confidentially filed its registration in April 2026, and Reuters reported the company was aiming for a June 12 Nasdaq debut under the ticker SPCX, pending SEC review of whether the prospectus adequately discloses the risks. For public-market investors, the central question is whether SpaceX can be valued on its own merits, or whether Musk’s empire comes with too many moving parts to price cleanly.

Know something we missed? Have a correction or additional information?

Submit a Tip