Spain’s fitness industry turns to penetration and pricing for growth

Spain’s gym market is shifting from site expansion to user capture and better pricing, with Barcelona exposing the real barriers to volume.

Penetration is now the growth story

The cleanest lesson from the Wuics Congress is that Spain’s fitness market is no longer being judged by how many more clubs it can open. The real question is how many more people it can pull in, keep paying, and keep coming back. That is why penetration and price emerged as the sector’s two most important levers, not as abstract strategy talk, but as the next practical battleground for growth.

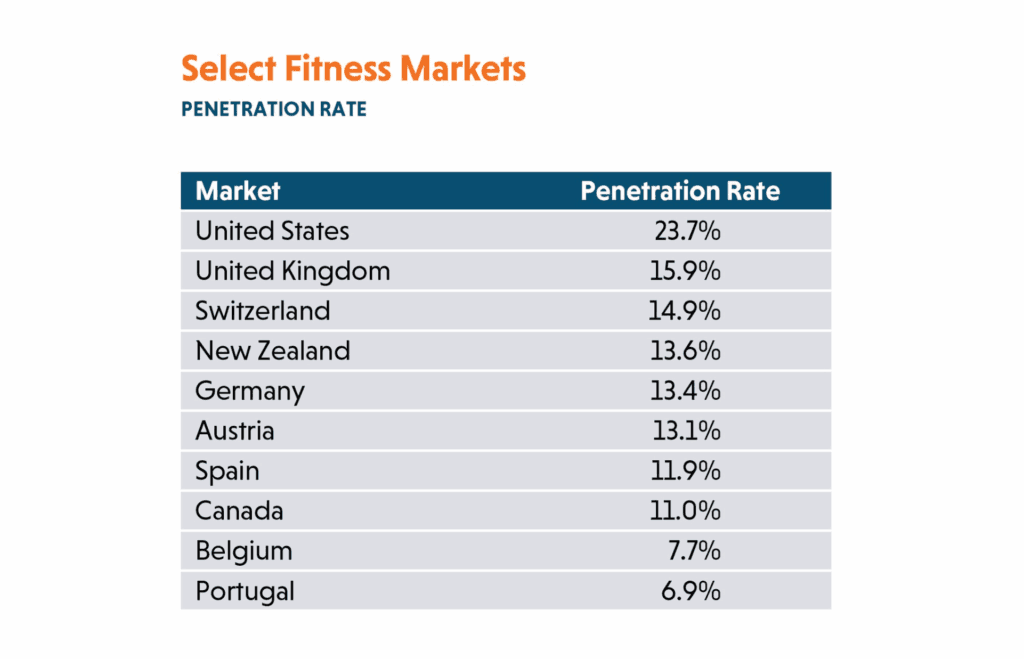

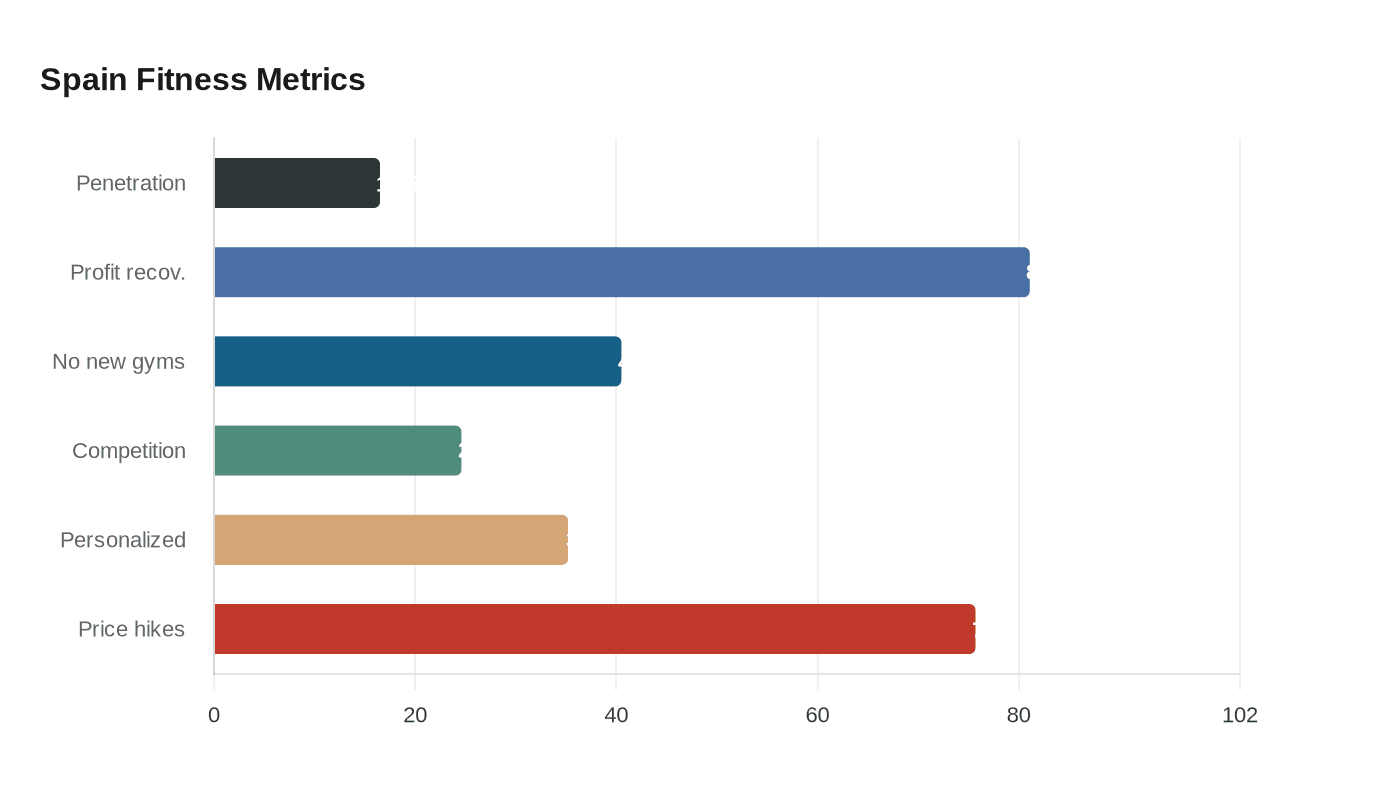

The numbers make the case. Palco23 put Spain’s fitness penetration at 16.5%, a figure that matches earlier sector studies showing 16.5% of the population going to the gym, across 4,561 gyms and 5.4 million users. Those same studies also put fitness at 3.3% of Spanish GDP and more than 400,000 jobs, which is enough scale to matter well beyond the gym floor. In other words, this is a large market that still has room to widen, but only if operators stop thinking only in square meters.

That was the point running through the 11th edition of the Congress Wuics, held at the Centre d’Alt Rendiment de Sant Cugat. The event featured eight talks, with August Tarragó, Jaime Gutiérrez, Josep Figueras, Rod Hill, Héctor Cruz, Rubén Gallart, Naomie Martín and Ernest López-Solá among the speakers. The common thread was simple: the sector has entered a phase where commercial discipline matters as much as coaching, equipment, or the feel-good language of wellness.

Barcelona turns the macro debate into a market test

Barcelona is the best place to see what that actually means. The city combines dense low-cost operators, boutique studios, PT-led concepts, and public or concession-based facilities in a way that few Spanish markets can match. The city council describes its municipal sports network as infrastructure that makes sport possible in every district, which matters because access is not just about club density, but about whether the city already gives residents a place to be active.

Private operators have built on that dense base. DiR says it operates 20 clubs between Barcelona and Sant Cugat, while VivaGym promotes more than 30 gyms in Barcelona. That level of competition is useful because it shows where the growth puzzle gets sharper: the market is not empty, but it is still under-penetrated enough that operators can win by converting non-users, occasional users, and lapsed users into recurring members.

- Which residents still sit outside the gym economy?

- Is the main barrier price, distance, intimidation, schedule, or lack of habit?

- What format wins the first visit, and what format keeps the monthly direct debit alive?

- How do operators add volume without turning the category into a discount bin?

If you translate penetration into real questions for Barcelona, they become very concrete:

That is the right lens because Barcelona does not need more vague optimism. It needs offers that feel easier to enter without feeling cheaper to own.

Pricing is not about discounting, it is about value

The most useful twist in the BDO report is that it shows a mature market acting like one. In its sixth report on fitness in Spain, published on November 21, 2025, BDO said 81.1% of the sport industry had recovered pre-pandemic profitability. It also found that 40.5% of companies did not expect to open any new gym by the end of 2025, and that competition, at 24.6%, had become the main business risk, ahead of energy costs.

That is the backdrop for the price debate. The old temptation in fitness was to win volume by going cheaper. The newer play is to raise prices while making the proposition broader, especially by adding health, wellness, and personalized training services. BDO said personalized service had reached 35.2% as a capture strategy, its highest level on record, while 75.7% of operators expected to raise prices in 2025. That is not a sign of a sector losing control; it is a sign of one trying to protect margin while improving perceived value.

In practice, that means price is no longer a blunt weapon. The question is not whether to charge less. It is whether the entry tier is accessible enough to pull in new users, and whether the higher tier feels justified enough to keep them. The sweet spot is a ladder of offerings, not a race to the bottom.

Why concessions, consolidation, and low cost all matter

Jaime Gutiérrez put a spotlight on the concessionary segment, which he sees as increasingly concentrated and likely to see more mergers in the coming years. That matters because concessions often sit closer to the public-private interface, where scale, operating efficiency, and municipal relationships can decide who grows and who stalls. If that segment keeps consolidating, the winners will be the operators that can run lean without looking thin.

August Tarragó added the historical perspective that makes the current moment easier to read. He said the sector has changed more in the last ten years than in the previous twenty, and he forecast five to ten spectacular years ahead. He also pointed out that penetration has moved from 11.5% in 2024 to 16.5% in 2026, which is a striking jump and a reminder that growth is coming from market expansion, not just from adding more clubs to the map.

Pere Solanellas sharpened the point further in April 2026 when he argued that low cost has less room to expand than concessions and that investment funds are now focused on maximizing their platforms before exiting. Taken together, those views describe a market that is still growing, but in a more selective way. The easy wins in low cost are getting narrower; the value creation now sits in better segmentation, better pricing discipline, and better use of the customer base already within reach.

What operators should take from the new playbook

The Wuics discussions point toward a fitness industry that is becoming more professional around usage, conversion, retention, perceived value, and cost structure. That is a welcome shift, because it forces the sector to ask better questions than “How many clubs can we open this year?”

The operators that win the next phase will likely do three things well:

- Build an entry offer that is genuinely easier to try, whether through access, convenience, or a clearer first-month value.

- Use price increases carefully, tying them to visible service gains such as coaching, wellness support, or more personalized programming.

- Treat retention as a commercial metric, not just an operations issue, because a member who stays is more valuable than a cheaper lead who never settles in.

Spain’s fitness market is not short of activity. It is short of conversion at the margins, and Barcelona shows exactly where the opportunity sits. The sector’s next growth run will come from persuading more people to walk in, pay up, and stay in, without making the product feel like a bargain-bin version of itself.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?