Aviation’s SAF scale-up faces funding gaps and rising costs

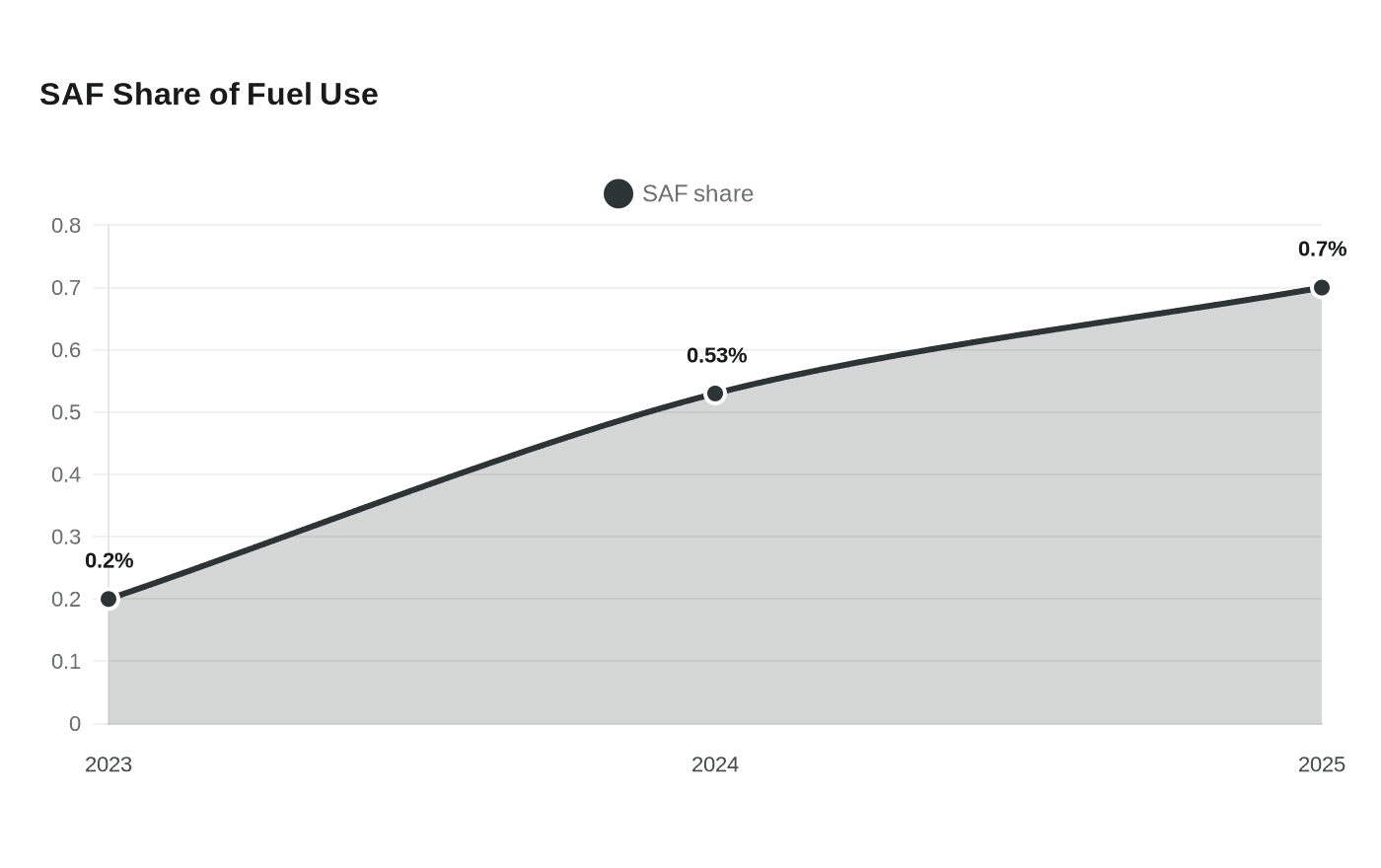

SAF is still only 0.53% of jet fuel use, and the real choke points are feedstock, financing and policy risk, not refinery scale alone.

The SAF market is running into a familiar bottleneck: policy is forcing demand higher, but the project stack is still too expensive to finance. IATA on June 1 said SAF production is expected to reach 2 million tonnes in 2025, equal to about 0.7% of airlines’ total fuel consumption, yet that still adds $4.4 billion to the global fuel bill. Feedstock scarcity, expensive clean power and hydrogen for e-fuels, and weak offtake visibility are keeping much of the industry stuck between pilot plants and final investment decisions.

A sector still has to scale far faster

Aviation is not a marginal emissions problem. In 2023, it accounted for 2.5% of global energy-related CO2 emissions, and aviation emissions reached almost 950 Mt CO2, more than 90% of pre-Covid levels. The International Energy Agency says low-carbon fuels, better aircraft and engine design, operational improvements and demand restraint all have to contribute if the sector is to get on track toward net zero by 2050.

That framing matters because SAF is being asked to carry too much of the burden too early. Even with policy support, the market remains tiny relative to jet-fuel demand, and the current scale is nowhere near enough to absorb the cost premium without either mandates, subsidies or both.

Feedstock is the first choke point

The cheapest molecule in SAF is still the one that is hardest to secure. Feedstock generally accounts for 60% to 80% of production costs in liquid biofuels, and the constraint is structural: there is only so much used cooking oil, tallow and soybean oil to go around. Europe and the United States are especially tight markets, while Brazil has relatively better feedstock self-sufficiency.

That shortage is why SAF prices remain elevated even where conversion technology is mature. HEFA can scale faster than newer pathways because the process is commercial and familiar, but it still runs into the same feedstock ceiling. In practice, the industry is bidding against renewable diesel, the broader biofuels pool and other users for the same limited inputs.

Mandates create demand, not cheap molecules

Europe’s policy regime has been the biggest near-term demand driver. The European Union and United Kingdom SAF mandates took effect on January 1, 2025, and IATA says those rules have made SAF in Europe about five times more costly than conventional jet fuel because of compliance fees charged by producers or suppliers. Willie Walsh, IATA’s director general, has said airlines are facing “price gouging” from fuel suppliers, a reflection of how compliance surcharges can be layered onto an already expensive product.

The result is a market that is supported, but not yet normal. IATA says most SAF is now flowing to Europe because the mandates are in force, yet the volume remains small enough that even modest cost inflation shows up quickly in airline fuel bills. That is the classic financing problem: demand exists, but the market structure still lets value leak out before enough capital can be pulled into new plants.

The finance gap is wider for e-fuels

The hardest projects are not the ones making HEFA. They are the ones trying to build power-to-liquid and other next-generation SAF routes that depend on clean electricity, hydrogen, carbon capture and large amounts of capital before any revenue arrives. The European Union Aviation Safety Agency says global SAF production represented only 0.53% of jet fuel use in 2024, up from 0.2% in 2023, while current annual SAF capacity in the EU is just above 1 million tonnes, almost all of it HEFA.

That leaves a very thin pipeline beyond today’s commercial technology. EASA says no power-to-liquid SAF plant in the EU has yet advanced beyond pilot stage, and the International Energy Agency says it has revised down its e-fuel forecast because there have been no final investment decisions for e-kerosene projects in the EU to meet 2030 ReFuelEU targets. In other words, policy is creating demand, but investment certainty is still missing.

The IEA says the EU could reach 3.5 million tonnes of annual SAF capacity by 2030 if projects under construction come online, but that still falls well short of the later-decade ramp regulators are trying to force. The problem is not only technology readiness. It is the bankability of long-term offtake, the cost of clean power, and the willingness of lenders to underwrite plants whose economics depend on policy staying intact.

What can scale, and what stays broken

Some SAF costs can fall with scale. Plant utilization, engineering standardization and tighter logistics can all help, especially for HEFA and other pathways that build on existing refining know-how. But the stubborn costs are the ones the market cannot easily engineer away: scarce feedstock, low-cost hydrogen, abundant clean electricity and policy certainty.

The United States has chosen a different support model. The IEA says the Inflation Reduction Act offers up to $1.75 per gallon of SAF produced, and by 2024 the federal government had announced $245 million in grants and nearly $3 billion in Department of Energy loan guarantees for SAF scale-up. That support matters because SAF still costs three to five times more than regular jet fuel, and the industry cannot close a financing gap of that size with offtake optimism alone.

The IEA expects SAF consumption to rise from 1 billion litres in 2024 to 9 billion litres in 2030, enough to meet about 2% of aviation fuel demand in its main case. That is real growth, but it is still a small slice of the market. Until feedstock, clean power and long-term financing line up, SAF will keep expanding by mandate before it reaches something close to a self-sustaining commodity market.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip