Sustainable aviation fuel faces policy hurdles despite farm industry hopes

Farm groups see a new corn and soy outlet, but IATA's 2026 SAF forecast shows the market is still tiny.

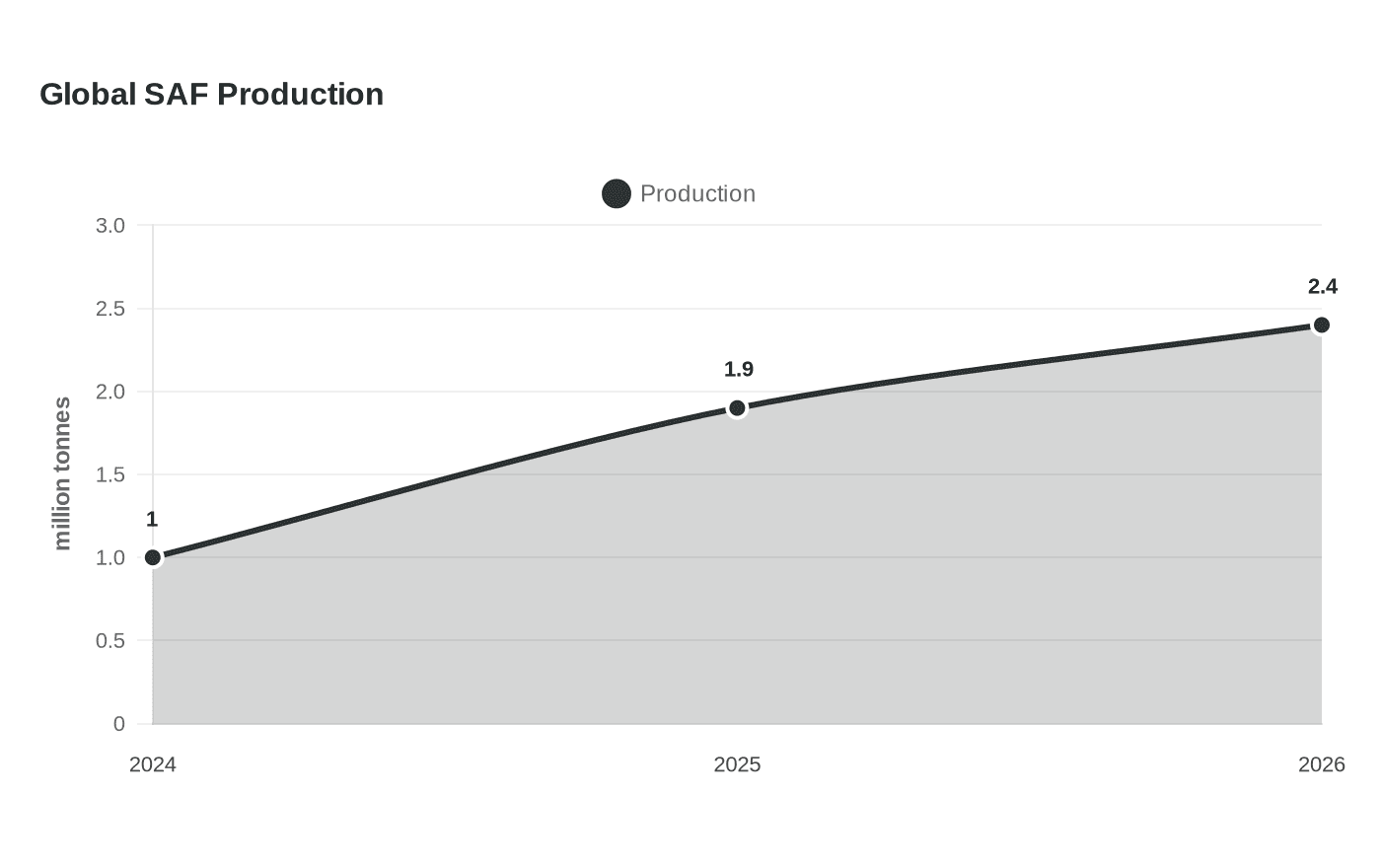

IATA on June 6 said global SAF production will reach 2.4 million tonnes in 2026. That would cover only 0.8% of aviation fuel use and cost airlines about $4.3 billion, a reminder that the market remains small even as U.S. farm groups chase it as a new outlet.

Why farmers are looking at SAF

Corn, soybean and ethanol interests have spent the past few years casting sustainable aviation fuel as one of the few new demand centers large enough to matter for U.S. agriculture. The Farm Bureau says farmers may benefit from stronger demand for corn oil, soybean oil, crop residues and animal fats, all of which already feed renewable diesel and are moving into the SAF pool.

The attraction is easy to see from the industry numbers. The U.S. Energy Information Administration said in 2024 that domestic SAF production capacity could jump by 1,400% if every announced addition comes online, while total U.S. biofuels output was expected to rise about 50% in 2024, led by SAF. That scale of buildout would be enough to change basis for some feedstocks, but only if the projects actually start up and keep running.

The problem is that the airline market is not expanding at the same speed as the project list. IATA said SAF output was expected to reach 1.9 million tonnes in 2025, up from 1 million tonnes in 2024, but growth is expected to slow in 2026 even as airlines are asked to absorb a costlier fuel pool. For farmers, that means the opportunity is real, but the size of the outlet is still far smaller than the rhetoric around it.

45Z is the main policy gate

The biggest policy lever is the Inflation Reduction Act’s Section 45Z Clean Fuel Production Credit. It applies to fuels produced after Dec. 31, 2024, and was originally set to expire at the end of 2027, which makes the Treasury and IRS rulebook critical for anyone trying to finance a plant or a feedstock supply chain.

Farm groups have pushed hard to make sure 45Z rewards the practices they say lower carbon intensity on U.S. farms. They want the credit calculations to account for cover crops, precision fertilizer applications and other regenerative practices, rather than relying on blunt assumptions that ignore how corn and soybean growers actually produce the crop.

That fight follows a rough first round. In 2024, Farm Bureau said the 40B SAF tax credit mostly missed the mark for farmers because it depended on a narrow pilot program tied to a specific package of climate-smart practices and a 50% greenhouse-gas reduction test versus petroleum jet fuel. USDA responded on Jan. 15, 2025, by publishing an interim rule with technical guidelines for climate-smart agriculture crops used as biofuel feedstocks, aimed at quantifying, reporting and verifying greenhouse-gas emissions from U.S.-grown commodity crops and helping recognize climate-smart agriculture in clean-fuel programs.

For the ag sector, the technical issue is not abstract. If a bushel of corn, a ton of soy oil or a load of crop residue cannot earn a strong carbon-intensity score under the final rules, it will not clear the economics of SAF at scale. The policy fight is therefore over who gets credit for the emissions profile, and whether domestic production gets preference over imported feedstocks that may already have an easier path into the system.

Congress is trying to widen the lane

On Jan. 16, 2025, senators including Jerry Moran, Chuck Grassley, Tammy Duckworth, Pete Ricketts, Amy Klobuchar and Joni Ernst reintroduced the Farm to Fly Act to support SAF development through USDA programs. Backers say the bill would help accelerate SAF through USDA tools and recognize it as an eligible resource under USDA bioenergy efforts.

That matters because USDA programs can do more than issue grants. They can help normalize SAF as a legitimate outlet for American feedstocks, link farm policy to clean fuel markets and give project developers a federal framework they can use when they sign supply and offtake agreements. Without that support, SAF remains vulnerable to the usual traps of first-generation policy: intermittent credits, weak demand signals and no dependable route from crop to contract.

Soybean groups have also pressed a separate point, arguing that 45Z should protect domestically grown feedstocks and remove incentives for imported waste feedstocks. That is not just a trade argument. It goes straight to the question of whether U.S. growers, crushers and biomass suppliers actually capture the value created by the federal credit structure.

What has to happen before SAF becomes a farm market

The path from hopeful forecast to bankable demand still has three hard checkpoints:

- The pathway has to be approved and usable at commercial scale.

- The feedstock has to score well on carbon intensity under the final rules.

- Airlines have to commit to long-term buying, not just one-off purchases.

Until those pieces line up, SAF will remain a promising but uneven market for agriculture. The numbers now on the table, 2.4 million tonnes globally in 2026, 1.9 million tonnes in 2025 and 1 million tonnes in 2024, show a sector that is growing but still too small to carry the policy burden that farm groups have placed on it. The upside is there, but American farmers will not see durable gains until federal credit design, USDA accounting and airline procurement all move in the same direction.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip