Insurance policy software market broadens across underwriting, billing and claims

Seventy-two tracked products make one thing clear: policy software is no longer a single category. Buyers now have to separate true core platforms from lighter tools that only cover part of the policy lifecycle.

Seventy-two products, one crowded category

Seventy-two tracked products sit inside SoftwareWorld’s insurance policy software directory, and that scale is the real story. The comparison page does not just list vendors; it exposes how far the category has stretched, with features that now run from rating engine and billing to claims tracking, underwriting management, and artificial intelligence.

That breadth matters because it turns policy software into a strategic infrastructure decision, not a simple procurement exercise. A buyer looking for policy issuance support may land on a different kind of product than a carrier trying to replace a full policy administration core, and the directory’s pricing models, company-size filters, and feature flags are useful precisely because they force that distinction.

Why the market feels harder to read

The confusion comes from overlap. SoftwareWorld’s feature set now spans billing and invoicing, forms management, renewal management, cancellation tracking, commission management, claims tracking, reinstatement tracking, quotes and estimates, and AI, which means vendors are competing across more of the insurance workflow than ever before. In practice, that makes the market look unified on the surface while hiding very different product depths underneath.

Celent’s North America report reinforces that point by profiling 50 policy administration systems for property and casualty carriers and comparing them by functionality, customer base, lines of business supported, technology, implementation, pricing, and support. That is a strong signal that the market is large enough, and varied enough, to require a more disciplined buyer map than a simple feature checklist.

How to sort vendors into buyer-friendly segments

The cleanest way to narrow the field is to split vendors into two broad camps: true core administration platforms and lighter policy tools. Core platforms are built to handle the policy lifecycle end to end, while lighter tools tend to sit around the edges, supporting quoting, forms, workflow, or a single operational step rather than the full administration stack.

For P&C carriers, the next filter is line-of-business complexity. A personal lines insurer, a commercial carrier, or a specialty writer will not place the same demands on product configuration, integrations, and servicing depth, which is why Celent’s emphasis on lines of business is so important. Implementation model also matters just as much, because cloud, on-premises, and hybrid approaches change deployment speed, maintenance burden, and the degree of control carriers keep over the platform.

A practical shortlist should usually ask four questions at once:

- Does the product run the full policy lifecycle, or only a slice of it?

- Can it support the carrier’s current and future lines of business without heavy custom work?

- Is the implementation model aligned with internal IT capacity and modernization goals?

- Does the vendor’s AI story support real workflow changes, or just marketing language?

What true core administration looks like

Guidewire’s PolicyCenter is a useful example of what a core administration system is supposed to do. Guidewire says it automates and streamlines policy administration tasks from quoting and underwriting to endorsements and renewals, while also working with billing and claims so data stays consistent across the business. That kind of scope is what separates a full core from a narrower policy utility.

Guidewire has also pushed that core model further with AI. On April 16, 2026, the company announced ProNavigator, embedding expert AI insights directly into insurance workflows so underwriters, claims adjusters, and customer service representatives can surface role-specific intelligence inside policy and claims processes. That is a strong example of how AI is being woven into operational systems rather than bolted on as a standalone layer.

Why modernization is driving the buying cycle

McKinsey’s May 2025 view explains why this market is moving now: modernization is one of the most pressing challenges for P&C insurers because many core systems were built for a slower, paper-driven model. Those legacy platforms create inefficiencies, higher IT maintenance costs, and trouble meeting customer expectations for instant quotes and faster claims payouts.

Donegal Mutual Insurance Company offers a concrete example of that pressure in action. On March 11, 2026, the company said it would migrate its claims, billing, and policy administration systems to the Guidewire Cloud platform, with claims and billing targeted for early 2027 and policy administration following in 2028. That phased move shows how carriers are balancing risk, modernization, and business continuity rather than trying to replace everything at once.

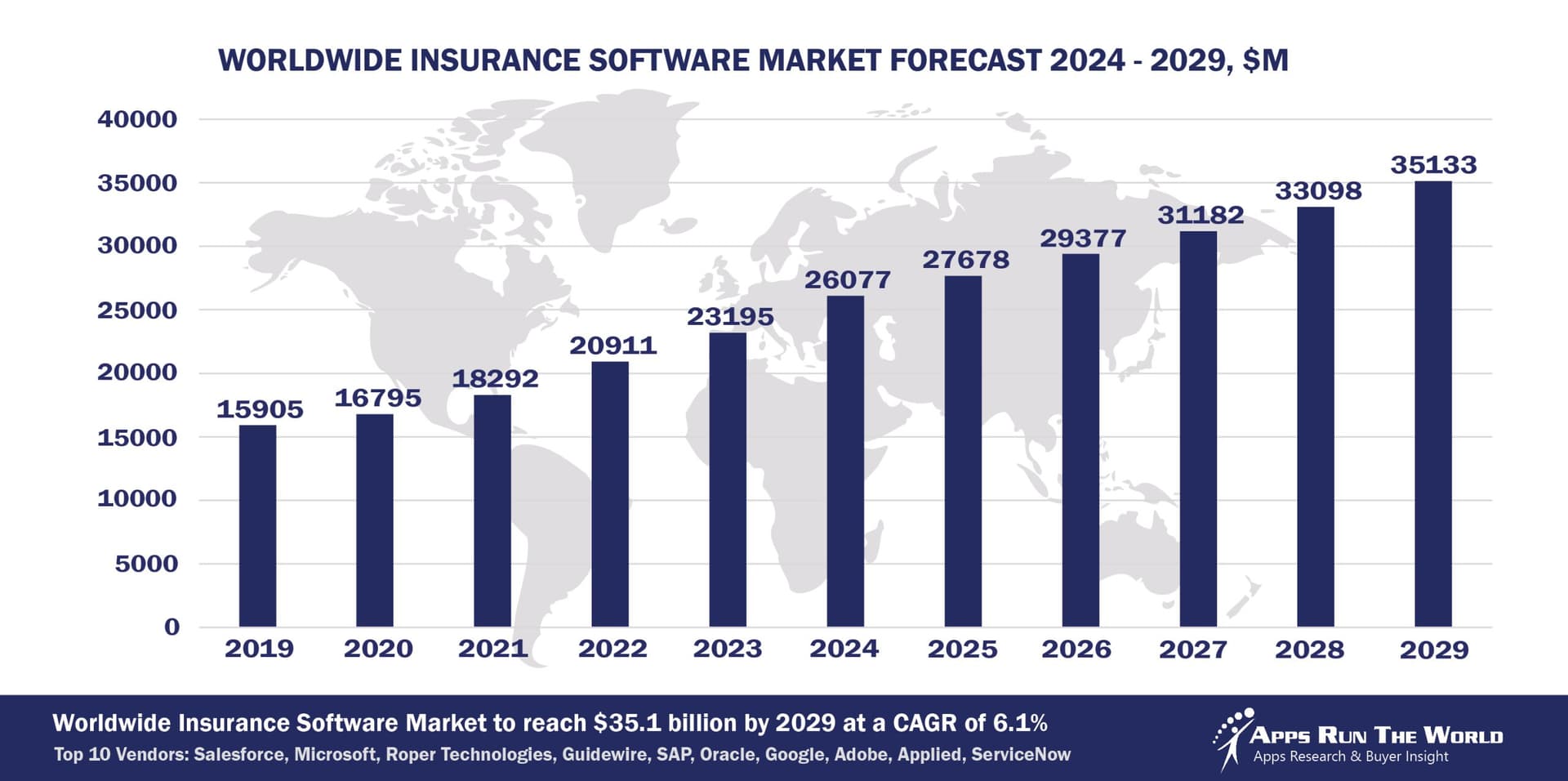

What the market size says about the opportunity

The market figures underline why vendors keep expanding their scope. One 2026 market report pegs the global P&C insurance software market at $24.85 billion in 2026, while another puts the insurance policy administration systems software market at $3.6 billion in 2025 and forecasts growth to $6.37 billion by 2030. Even allowing for different definitions, both numbers point to a sizeable and still-growing software category.

That scale helps explain why directories like SoftwareWorld’s matter so much right now. The challenge is no longer finding software; it is understanding which vendors are real core replacements, which are adjacent workflow tools, and which are only credible for a narrow use case. In a market this broad, the winners will be the buyers who can separate lifecycle depth from feature noise before the implementation clock starts ticking.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip