Alternative proteins face a commercialization test beyond scientific breakthroughs

The next alt protein winners will be the ones that can win shelf space, factory time, and financing. Better science alone no longer closes the deal.

The next winners in alternative protein will not be the ones with the fanciest bench-top demo. They will be the ones that can book manufacturing time, win a place on retail shelves or foodservice menus, and keep enough capital in reserve to survive the long ramp from prototype to repeat purchase. That is the real bottleneck now: access.

Distribution is the gatekeeper

The commercial test has shifted from “Can it be made?” to “Can it be sold, at scale, through real channels?” Access to manufacturing, access to customers, access to distribution partners, and access to capital all sit between a promising formulation and a product that can stay on the market. That matters because a technical breakthrough does not build an industry if the route to commercialization is too expensive, too narrow, or too dependent on one buyer.

This is why shelf placement and foodservice placement now matter as much as the headline science. A startup can impress investors with a clean protein profile or a clever fermentation process, but the category only matures when the product fits retailer requirements, buyer specs, and production economics well enough to move through a supply chain without constant heroics. Go-to-market competence is what turns a pilot run into a repeat order.

Capital is available, but it is not evenly spread

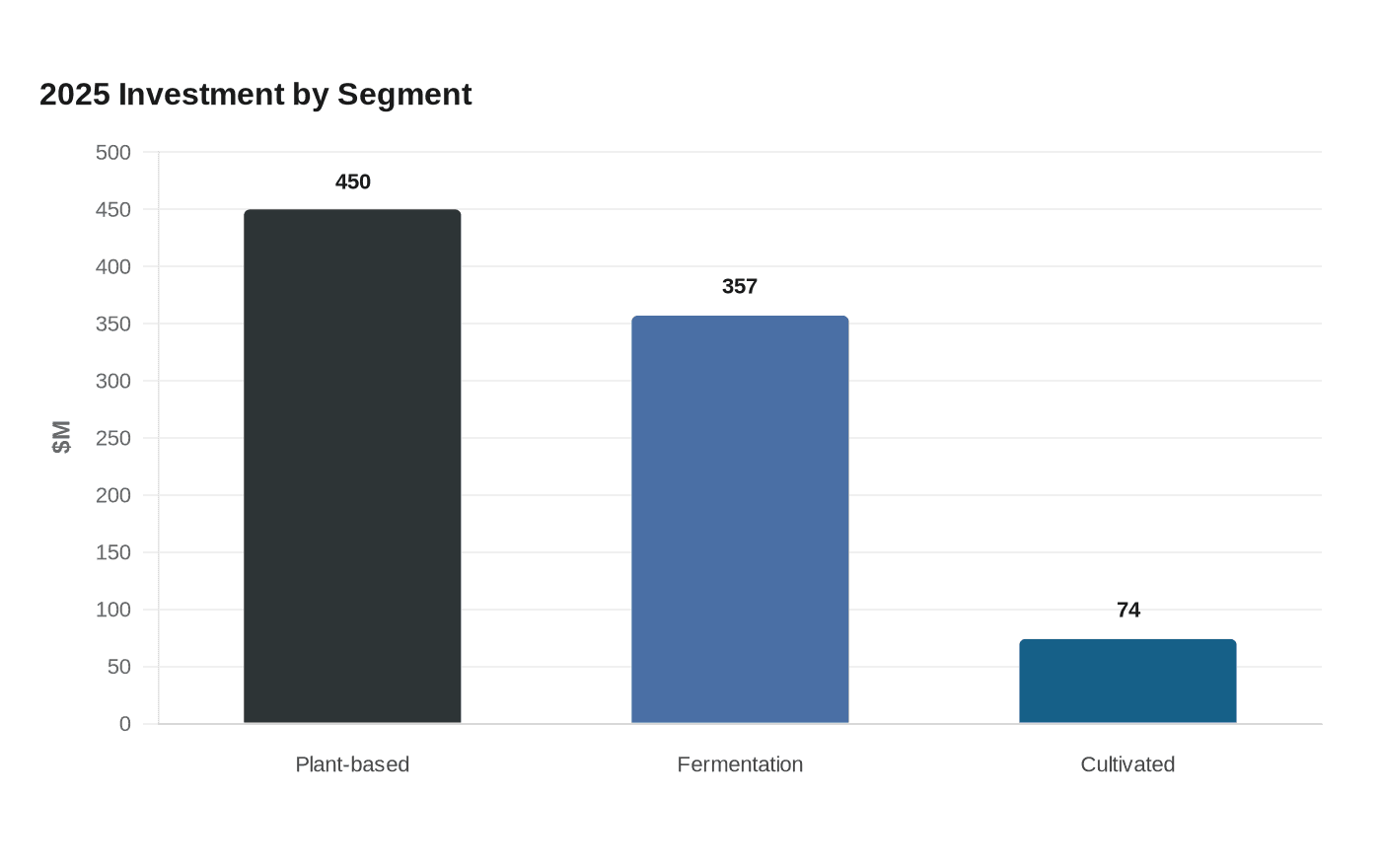

The money picture shows a category that is still funding up, just more selectively. The Good Food Institute’s 2025 investment analysis says alternative protein companies raised US$881 million in 2025, bringing total investment since 2016 to more than US$19.3 billion. Within that 2025 total, plant-based companies raised US$450 million, fermentation companies raised US$357 million, and cultivated meat and seafood companies raised US$74 million.

That split tells you where investors are finding the clearest path to near-term scale. Plant-based still pulls the largest share, fermentation has become a serious commercial lane, and cultivated meat and seafood remain capital-light compared with the others. GFI also says Q1 2026 investment reached US$208 million, which keeps the funding window open but makes the competition for those dollars more exacting.

Factories are now part of the strategy

The commercialization bottleneck is physical, not just financial. GFI’s State of Alternative Proteins report says at least 46 alternative protein facilities were launched, expanded, or announced in 2024, including four cultivated, 16 fermentation, and 26 plant-based facilities. That is the kind of buildout that tells you the category is moving from slide decks to industrial planning.

The plant-based side is especially instructive because it shows how much can be done by repurposing existing assets. GFI’s plant-based sector summary says at least 26 plant-based facilities were opened, expanded, or announced in 2024, including retrofits of conventional protein plants. Danone converted a conventional yogurt facility to plant-based yogurt production, and Lactalis Canada reopened a former dairy plant as a plant-based milk facility. Those are the kinds of moves that matter: not a theoretical plant someday, but existing equipment turned toward a new product line.

Go-to-market competence looks like infrastructure

The industry is also building the tools that make commercialization less improvisational. GFI’s alternative protein company database is meant to help users identify manufacturers and ingredient suppliers, while its contract manufacturing database includes co-manufacturers, co-packers, private labelers, and consultants for plant-based, cultivated, and fermentation-derived meat, seafood, egg, and dairy products. That is not glamorous work, but it is exactly what companies need when they are trying to bridge the gap between R&D and stable production.

The investor side is getting organized the same way. GFI’s investor directory features hundreds of investors interested in alternative protein companies, and its entrepreneurship resources say more than 200 investors have opted in to share information with fundraising startups. In practice, that means the category is now explicitly mapping the routes to capital and capacity instead of pretending every company can figure those links out alone.

Policy is starting to treat biomanufacturing like infrastructure

Public money is following the same logic. GFI’s State of Global Policy report says governments announced about US$510 million in new committed funding for alternative proteins in 2024, bringing cumulative government commitment to around US$2.1 billion. The report also points to China, the European Union, and other countries treating biomanufacturing capacity as strategic, including support for shared biomanufacturing facilities.

That is an important shift because it places alternative protein inside a larger industrial policy conversation. The issue is no longer just whether a specific startup can raise the next round. It is also whether a country or region can secure the manufacturing base, shared equipment, and supply-chain resilience needed to produce new proteins without depending on a single fragile path to scale.

Scale-up partnerships are replacing lab bragging rights

The broader market is moving in the same direction. Fermentation startups are attracting investment, regulatory approvals, and commercial partnerships as manufacturers look for alternatives to constrained conventional supply chains. That matters because it shows buyers are not just chasing novelty, they are chasing continuity, and continuity usually comes from production systems that can hold up under real demand.

Universities are becoming part of that commercialization bridge too. The University of Illinois is helping companies move from lab breakthroughs to commercial production, including work with ADM and Primient. That kind of pilot-plant support is where a lot of promising ingredients either become manufacturable or get exposed as too finicky for the line. The next wave of alternative protein companies will be judged less by what they can prove in the lab and more by what they can deliver through factories, partners, and distribution channels that already exist.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?