Plant-Based Market Extends Far Beyond Meat Alternatives, FoodNavigator Says

The plant-based market is bigger than meat analogues. New data shows the real scale sits in dairy, bakery, eggs, snacks and foodservice, not just burgers.

The plant-based aisle is much wider than the burger case

The biggest mistake in plant-based food is still the easiest one to make: treating it like a meat-replacement story. FoodNavigator’s latest framing pushes back hard on that habit, arguing that burgers, nuggets and sausages may grab the headlines, but they are only a small slice of a much broader market built on dairy alternatives, bakery, snacks, beverages, ready meals and functional foods.

That shift in perspective matters because it changes the commercial question entirely. The category is not just about whether a plant-based patty can mimic beef closely enough. It is about where shoppers already reach for plant-based products in ordinary routines, from coffee to lunch to pantry staples, and how brands can win by fitting those moments instead of chasing novelty alone.

Where the real volume sits

The better way to read the market is through use occasion, not just through imitation. A plant-based milk in the morning, a hybrid snack at midday and a meat alternative only occasionally tell a very different story from the one usually implied by burger launches and freezer-door theater.

That broader view is supported by the category mix itself. The plant-based story extends across traditional foods and everyday staples, where consumers are choosing plant-based ingredients for flavor, familiarity, nutrition or convenience. In practice, that means dairy alternatives, bakery items, snacks, ready meals and functional foods can all contribute materially to growth, even when they do not look like classic meat analogues.

Retail still shows a category with reach, but uneven momentum

The Good Food Institute’s 2024 executive summary shows the market is still expanding, but not in a single straight line. Global retail sales of plant-based meat, seafood, milk, yogurt, ice cream and cheese rose 5% in 2024 to $28.6 billion. In the U.S., retail sales reached $8.1 billion, above 2017 levels but still below the $8.5 billion peak hit in 2022.

That combination of growth and retrenchment is the point. It shows the category has moved beyond a start-up phase, yet it still faces technical hurdles, cost pressure, weaker investment and uneven sales by segment and geography. At the same time, new product launches and improved shelf velocity suggest the market has not stalled; it has simply matured into something more selective.

The industrial side of the story is moving too. GFI says at least 26 plant-based facilities were opened, expanded or announced in 2024, including conversions of conventional dairy plants to plant-based production. That is a supply-chain signal as much as a consumer signal: companies are not just testing labels, they are retooling assets to serve a more diversified plant-based portfolio.

The category is already far broader than six product types

The Plant Based Foods Association’s 2024 marketplace summary reinforces the same point from a different angle. It says the industry has grown from six primary categories in 2018 to more than 20 today, spreading across a much wider range of grocery aisles and menu placements.

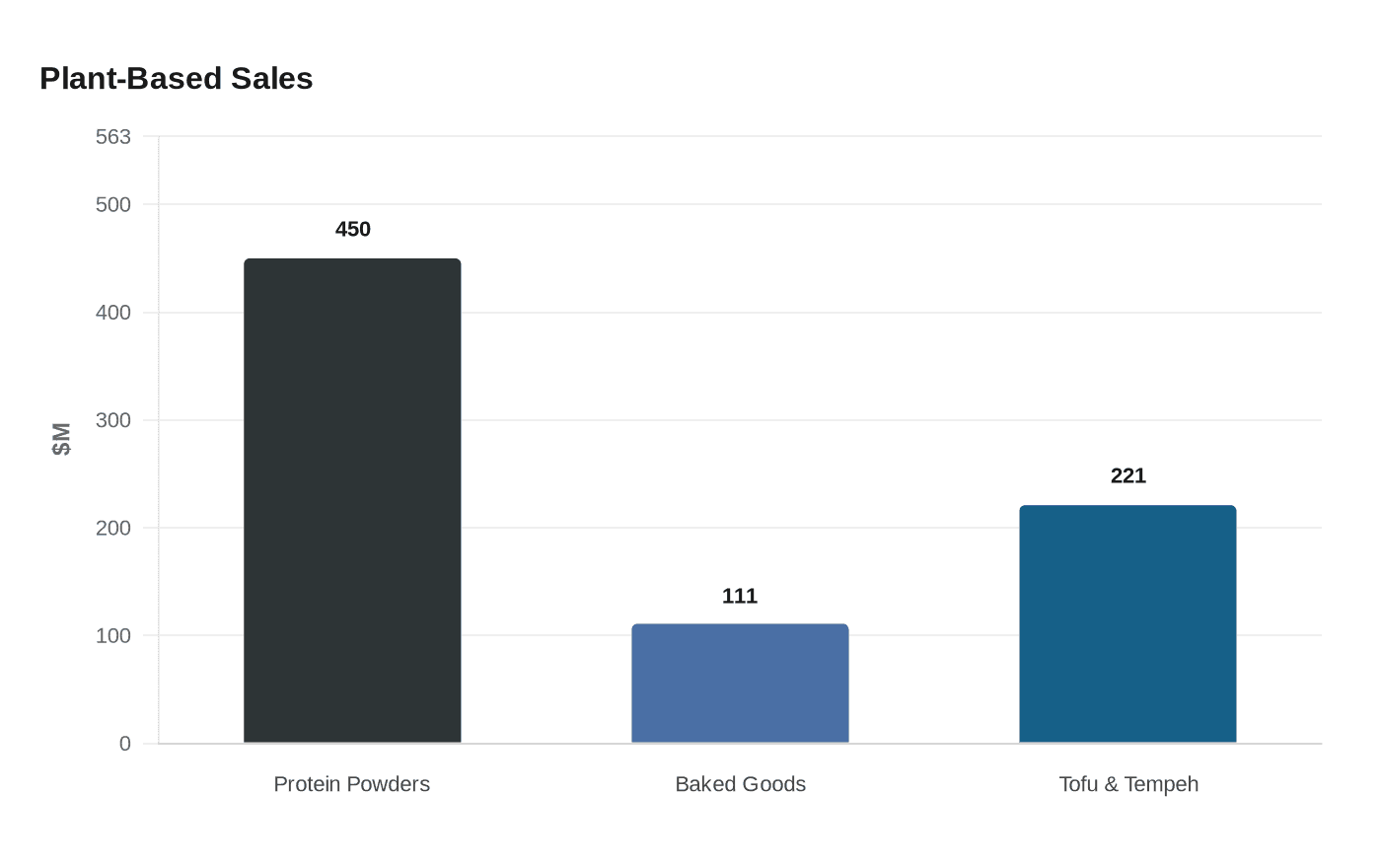

That expansion has not come from a single hero product. PBFA reports 59% household penetration and a 79% repeat purchase rate in U.S. grocery retail, which makes the category look less like a niche experiment and more like a mainstream repeat-buy set. Its retail breakdown shows where some of the action is: plant-based protein powders and liquids rose 11% in dollars to $450 million, baked goods grew 13% to $111 million, and tofu and tempeh climbed 7% to $221 million.

Those numbers matter because they expose how much plant-based growth lives outside the meat-alternative conversation. Protein powders, baked goods and tofu are not trying to win the same shelf battle as a frozen burger. They are winning by doing ordinary jobs well, which is often how a category becomes durable.

Foodservice shows the same diversification

The foodservice channel makes the case even more clearly. GFI says U.S. broadline distributor sales of plant-based protein reached $289 million in 2024, down 5% on the year, but still growing at a 4% compound annual rate since 2020. That is a reminder that short-term volatility does not erase medium-term traction.

Plant-based milk rose 9% in dollar sales in foodservice, and plant-based creamer rose 5%, reaching a 31% share of the total creamer market in that channel. Plant-based eggs were smaller but notably fast-growing, with dollar sales up 28% and pound sales up 30%. Those are the kinds of numbers that show where real menu integration is happening: beverages, coffee service, breakfast applications and back-of-house substitutions, not only headline-grabbing entrees.

Even in foodservice, analogues are not the whole story. GFI says analogues accounted for more than half of plant-based protein pound sales in the channel, but tofu, tempeh and grain, nut and vegetable items are also part of the mix. Restaurants remain the largest purchasers, while healthcare, business, industry and government operators expanded purchases in 2024, broadening the market well beyond the place where consumers first encountered plant-based food.

What this means for brands and investors

The strategic lesson is simple but easy to miss: plant-based scale is more likely to come from everyday foods than from constant comparison with meat. The products with the strongest long-term case are often the ones that disappear into normal habits, not the ones that demand a special eating occasion.

That is why the most useful lens is not “What is the next plant-based burger?” but “Where do plant-based ingredients already solve a consumer need?” The answer keeps pointing to dairy alternatives, snacks, bakery, eggs, beverages, convenience foods and ingredients that fit existing routines. NIQ’s broader trend view matches that direction, showing the category expanding beyond meat substitutes into dairy alternatives, snacks, beverages, seafood substitutes and plant-based eggs.

The market’s future will likely be built by products that are familiar before they are fashionable. The companies that understand that are not chasing a narrow protein trend; they are helping plant-based food become part of the everyday pantry, the everyday menu and the everyday grocery run.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?