UK Supermarkets Could Capture Billions by Championing Plant-Based Proteins

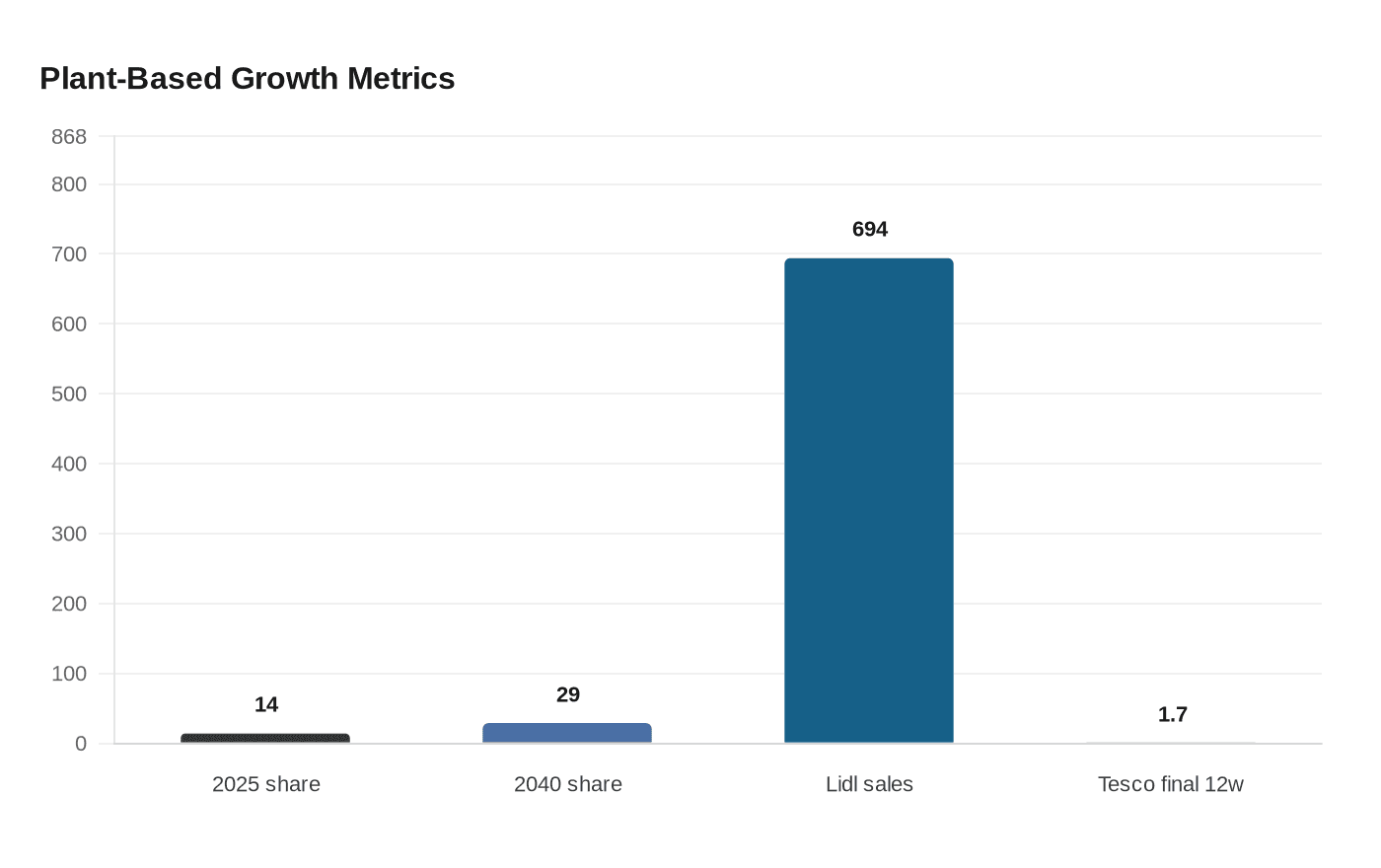

Supermarkets are leaving plant-based protein on the side aisle, even as its share of UK protein sales is set to climb from 14% to 29% by 2040.

British grocers are sitting on a bigger protein opportunity than their shelves suggest. A new Systemiq analysis says the UK plant-based share of protein sales is projected to rise from 14% in 2025 to 29% by 2040, but retailers are still not matching that growth with the kind of pricing, placement and own-label muscle that has long driven mainstream food sales.

The commercial gap is stark in private label. Systemiq found that own-brand products account for 69% to 82% of processed meat sales in the UK, but only 2% to 30% of plant-based protein sales. That imbalance leaves supermarkets exposed to a category that can feel like a branded add-on rather than a profitable staple, even though the report argues the opposite: if retailers treat plant-based proteins as a core range, they can win margin, control the shelf and shape consumer habits before competitors do.

The report, Taking Root: The Case for Plant-Based Proteins in UK Retail, was published on 22 April 2026 and draws on Euromonitor and NielsenIQ sales data, consumer research and life-cycle assessment evidence. It says animal-protein prices rose while plant-based prices fell between 2020 and 2025, and it projects meat analogues will reach price parity with processed meat by 2028. Systemiq also says visibility, expanded shelf space and promotional support have driven plant-based sales growth of 30% to 57% in recent case studies, a reminder that demand can move when stores merchandise the category like a serious business rather than a side aisle experiment.

The category is broader than burgers and sausages. Systemiq breaks its analysis into meat analogues, minimally processed plant proteins, legumes and nuts, plus a precision-fermentation case study. That matters for retailers trying to build a more resilient assortment, especially as the report says diversification can reduce exposure to animal-protein price volatility and support longer-term margin stability.

Some chains are already testing the commercial upside. Lidl GB said in September 2025 that its own-brand meat-free and alternative-milk sales had risen 694%, far above its 400% target, and that it wants 25% of all protein sold by 2030 to come from plant-based sources. Tesco said in February 2026 that chilled plant-based food in the UK had returned to growth for the first time in years, with Nielsen data showing volume demand rising by just under 1% across UK supermarkets in 2025 and reaching 1.7% in the final 12 weeks of the year.

The public-health case is lining up with the retail one. UK guidance recommends 30g of fibre a day for adults, but the NHS says most adults eat about 20g, and the National Diet and Nutrition Survey 2019 to 2023 says intakes are still missing dietary targets. GFI Europe says plant-based meat is higher in fibre and lower in saturated fat than processed meat, while the UK has imported an average of 2.6 million tonnes of meat and dairy a year since 2012. ProVeg says nine UK retailers, representing more than 80% of supermarket market share, now use the WWF Basket methodology to track protein sales, giving grocers a common yardstick. The next advantage will go to the chains that use it to set targets, move shelf space and build private label fast enough to own the category, not just stock it.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?