Goldman Sachs sees AI, geopolitics and energy supply driving commodities in 2026

Goldman is tying commodities to AI, geopolitics and energy supply at once, and its real message is that gold and copper may outrun oil if those forces collide.

The framework: three forces, one commodity map

Goldman Sachs is no longer treating commodities as a simple inflation trade. Its 2026 view ties the complex to three forces moving together, and sometimes against each other: the U.S.-China AI and geopolitical power race, global energy supply waves, and a macro backdrop of sturdy growth with 50 basis points of Fed rate cuts in 2026.

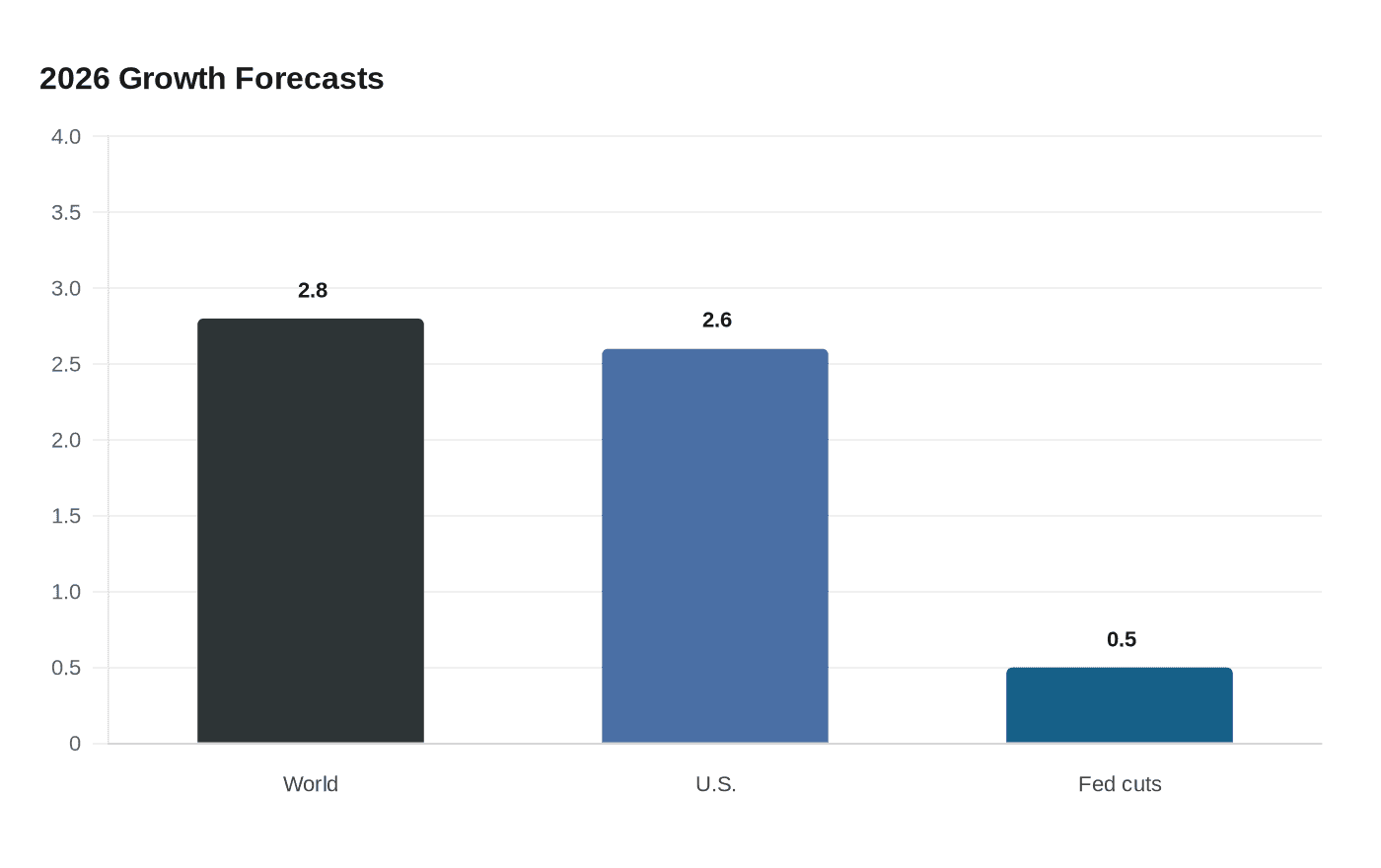

That matters because Goldman’s broader 2026 outlook still assumes the world economy can grow 2.8%, with the U.S. outperforming at 2.6% on reduced tariff drag, tax cuts and easier financial conditions. In other words, the bank is not calling for a crisis backdrop. It is arguing that commodities can still work because the demand side is being reshaped by AI build-out spending and the supply side is being constrained by geopolitics and energy-system bottlenecks.

The timing is also important. Commodity markets already spent 2025 splitting into winners and losers: precious and industrial metals posted strong gains, while oil was weaker. Goldman’s message is that this split is not a temporary anomaly. It is the shape of the next cycle.

Gold: reserve safety beats cyclical logic

Gold is the cleanest expression of Goldman’s thesis. Reuters reported the bank sees gold rising 14% to $4,900 an ounce by December 2026, with upside risks. That is not just a price call. It is a verdict on trust, reserve management and the willingness of official buyers to keep leaning in when policy and geopolitics stay unstable.

Goldman’s own earlier work explains why. The bank has said central banks hold more than $12 trillion in foreign-exchange reserves, and that the freezing of more than $280 billion of Russian central-bank assets after Russia invaded Ukraine changed perceptions about reserve safety. It also said gold trading tends to spike during geopolitical turmoil, which is why sanctions risk and conflict can matter just as much as rate cuts.

That is a sharp change from the old commodity playbook, where gold often traded mainly as a rates-sensitive hedge. Goldman has already forecast gold to rise 6% through the middle of 2026, and in one 2025 note it said gold rose more than 40% in 2025. The common thread is that the bank keeps coming back to multi-year central-bank demand and to the idea that geopolitical strain feeds official buying, not just retail speculation.

For anyone covering precious metals or macro products, the implication is blunt: gold is no longer just a reaction to real yields. It is also a proxy for reserve diversification, sanctions anxiety and policy credibility.

Oil: the supply wave still points lower

Goldman is much more cautious on oil. Reuters reported its 2026 base case for Brent is $56 a barrel and for WTI $52, with oil possibly hitting its lowest point around mid-2026 as the market begins to price rebalancing. Goldman also said lower prices may be needed to rebalance the market after 2026 unless there are large supply disruptions or OPEC production cuts.

That call fits the backdrop. Demand is still expected to grow, by about 1.2 million barrels a day, but Goldman sees that being offset by declining Russian supply if war and sanctions persist, and by slower non-OPEC ex-Russia growth. It has also said the physical oil market has not been impeded despite geopolitical turmoil in the Middle East and Ukraine, which is another way of saying the market has absorbed shocks better than headlines suggest.

For energy desks, this is the part of the outlook that separates near-term volatility from structural price direction. A geopolitical flare-up can still send crude higher in a hurry. But Goldman’s base case says the heavier force is supply normalization, not a permanent shortage. If AI and power demand are creating new structural winners elsewhere in commodities, oil is the market where the bank is most clearly betting that the cycle will have to clear lower prices first.

Copper: AI turns electrification into a commodity bid

Copper is where Goldman’s AI lens becomes tangible. Reuters reported that the bank expects copper to average $11,400 a metric ton in 2026 and still considers it its favorite industrial metal. The reason is simple: Goldman says electrification drives nearly half of copper demand, while mine supply faces unique constraints.

That is the bridge between the abstract and the physical. AI is not just a software story. It is a power story, a grid story and a metals story. Goldman has separately published research on data-center power demand, rising hyperscaler reinvestment and the scale of the AI build-out, which reinforces the same point: the capital spending tied to AI does not stay on a screen. It moves into wires, transformers, substations, backup systems and the metals that connect all of them.

For industrials and infrastructure coverage, that makes copper a better cross-asset signal than it used to be. It is not only about Chinese demand or a broad manufacturing upswing. It is also about how fast the AI economy can pull forward physical investment in electricity and the supply chain around it. That is why Goldman’s copper view sits so naturally beside its broader research on heavy assets, low obsolescence in the AI era and Europe’s shift to electrification.

What this means for coverage, client conversations and the old playbook

Inside Goldman, the practical value of this outlook is that it forces desks to talk to each other. Commodity traders need to think about supply shocks, sanctions and OPEC responses. Energy bankers need to think about whether data-center power demand and grid spending create new financing demand. Industrials and infrastructure teams need to decide whether AI is front-loading capex across the physical economy. Macro teams need to explain why sturdy growth does not automatically mean a generic commodity rally.

That is where the firm’s commodities bench, including Daan Struyven, Samantha Dart and Lina Thomas, matters. The useful client conversation is no longer a single-direction call on inflation. It is a layered argument about reserve safety in gold, supply discipline in oil and electrification demand in copper. It also means traders and strategists may need to watch a wider set of signals, from central-bank reserve behavior to LME copper inventories, CFTC positioning and OPEC policy, rather than relying on one cycle indicator.

If the three forces conflict, geopolitics is probably the most powerful near-term driver because it can move gold, oil, reserve flows and sanctions risk at the same time. AI is the slow structural force, while energy supply is the constraint that decides how much of that AI demand shows up in prices. Goldman’s message is that commodities are no longer a side bet on growth. They are becoming a direct read on power, security and the physical cost of the AI era.

Know something we missed? Have a correction or additional information?

Submit a Tip