Goldman Sachs sees broadening 2026 bull market, lower index returns

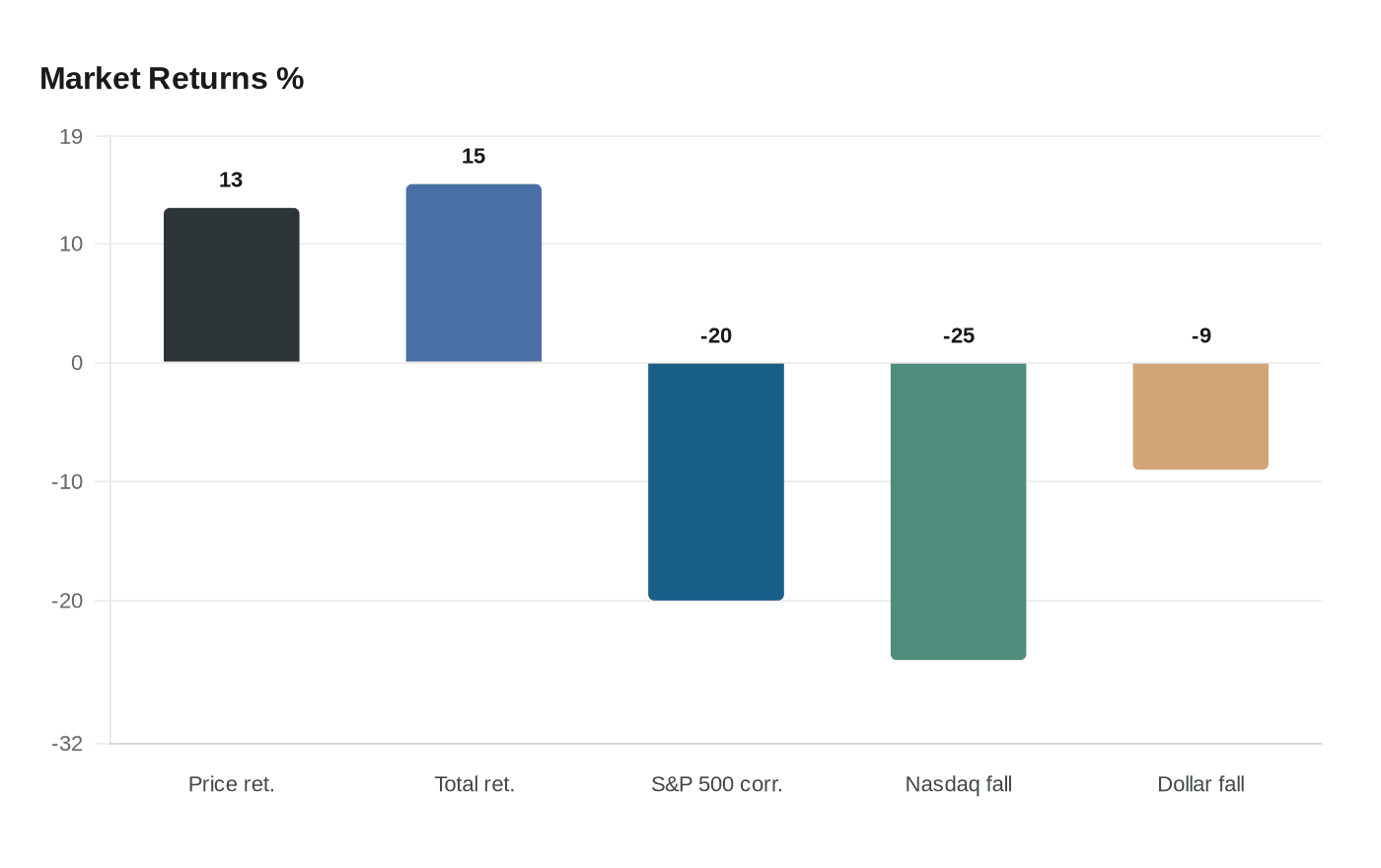

Goldman expects 2026 gains to come less from a few megacaps and more from wider earnings leadership, with 13% price returns and 15% total returns.

Goldman Sachs is betting the next leg of the bull market will look less like the AI-fueled sprint investors got used to and more like a wider, messier advance. In its 2026 equity outlook, titled “Tech Tonic — a broadening bull market,” the firm projected about 13% price returns and 15% total returns in U.S. dollars over the next 12 months, with most of the gain coming from earnings rather than a fresh surge in valuation multiples.

That distinction matters inside Goldman as much as it does for clients. A market driven by broader participation changes the job from explaining a handful of megacap winners to defending sector calls, stock selection and regional positioning. Goldman said tech still mattered, but the opportunity set was widening as earnings and performance dispersed more evenly across sectors and styles. It also said the setup fit continued economic expansion in all regions and further modest easing by the U.S. Federal Reserve.

Peter Oppenheimer, Goldman’s chief global equity strategist, said it would be unusual to see a significant equity setback or bear market without a recession, even from elevated valuations. That is not a blank check for risk taking. It is a reminder that the bull case depends on growth staying intact and on the rotation spreading beyond the same narrow leadership group that has dominated much of the last few years. Goldman said diversification mattered in 2025 and likely would matter again in 2026, especially across regions, investment factors and sectors, with more attention on emerging markets and on AI beneficiaries outside pure technology.

The backdrop to that call was a volatile 2025. Goldman said the S&P 500 corrected by just under 20% between mid-February and April, while the Nasdaq fell almost 25%, pressured by tariff fears and spillover effects from DeepSeek’s introduction. Both indexes then rebounded by close to 45% from the trough. Goldman also said U.S. markets underperformed for the first time in nearly fifteen years, while the dollar fell 9% and non-U.S. markets outperformed, a turn that sharpened client questions about U.S. exceptionalism.

Goldman Wealth Management said clients were already asking whether they should cut U.S. equity exposure in favor of other developed and emerging markets. That is the real test of the broadening thesis: not whether the market can keep rising, but whether earnings growth, low correlations and wider sector leadership can hold long enough to make the rotation feel durable instead of temporary.

Know something we missed? Have a correction or additional information?

Submit a Tip