Goldman Sachs sees larger 2026 copper surplus, cuts price outlook

Goldman lifted its 2026 copper surplus forecast to 490,000 tonnes and cut its price view, signaling a weaker demand backdrop for miners and electrification bets.

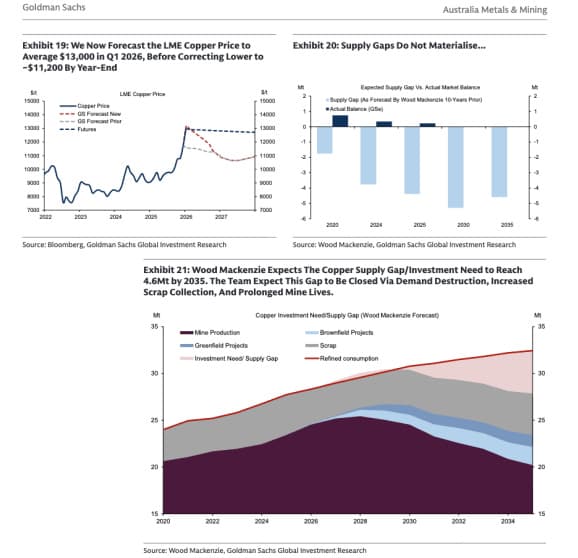

Goldman Sachs now sees a 490,000-tonne copper surplus in 2026, up from a prior forecast of 380,000 tonnes, and has trimmed its average price outlook to $12,650 a tonne from $12,850. The change is a clear reality check for a market that had been leaning on the electrification super-cycle to justify higher prices and tighter supply assumptions.

The bank also cut its forecast for 2026 refined copper demand growth to 1.6% from 2.0%, saying higher energy prices could shave 0.4 percentage points off global GDP growth. That is the kind of macro drag that matters for miners, smelters, and industrial clients that have spent the past few years planning around stronger demand from grids, power infrastructure, data centers and the broader energy transition.

Goldman’s earlier research had already warned that copper would struggle to hold above $11,000 for long in 2026, with the metal expected to trade in a $10,000 to $11,000 range and average $10,710 in the first half of the year. Even with the shorter-term downgrade, the bank has not abandoned the structural bull case. Goldman still sees copper demand supported by grid and power buildouts, AI-related infrastructure, and defense spending, and it has kept a long-term 2035 price target of $15,000 a tonne.

That split view is the one employees on the commodities side will have to carry into client calls. The near-term message is weaker demand and a looser balance. The longer-term message is that copper remains central to the same megatrends Goldman has been pitching across research and advisory work. For bankers covering miners, power companies, and industrials, that means more pressure to separate projects that can survive softer pricing from those that only work in a straight-line bull market.

The backdrop is volatile enough to keep both sides of the debate alive. Copper touched record highs in January 2026 before retreating, and other major forecasters remain more constructive. The International Copper Study Group has pointed to a 150,000-tonne deficit in 2026, while the World Bank has said base metal prices should firm in 2026 and 2027 as modest demand growth meets tighter supply. Goldman’s latest call is a reminder that the energy-transition trade is still vulnerable to growth shocks, geopolitics and energy costs, even if the long-run thesis has not broken.

Know something we missed? Have a correction or additional information?

Submit a Tip