Goldman Sachs sees strong fundamentals in its $130 billion private credit business

Goldman’s private credit book is big enough to shape where fee growth and career upside land. Rising stress is making underwriting and restructuring skills more valuable.

Private credit is no longer a side bet at Goldman

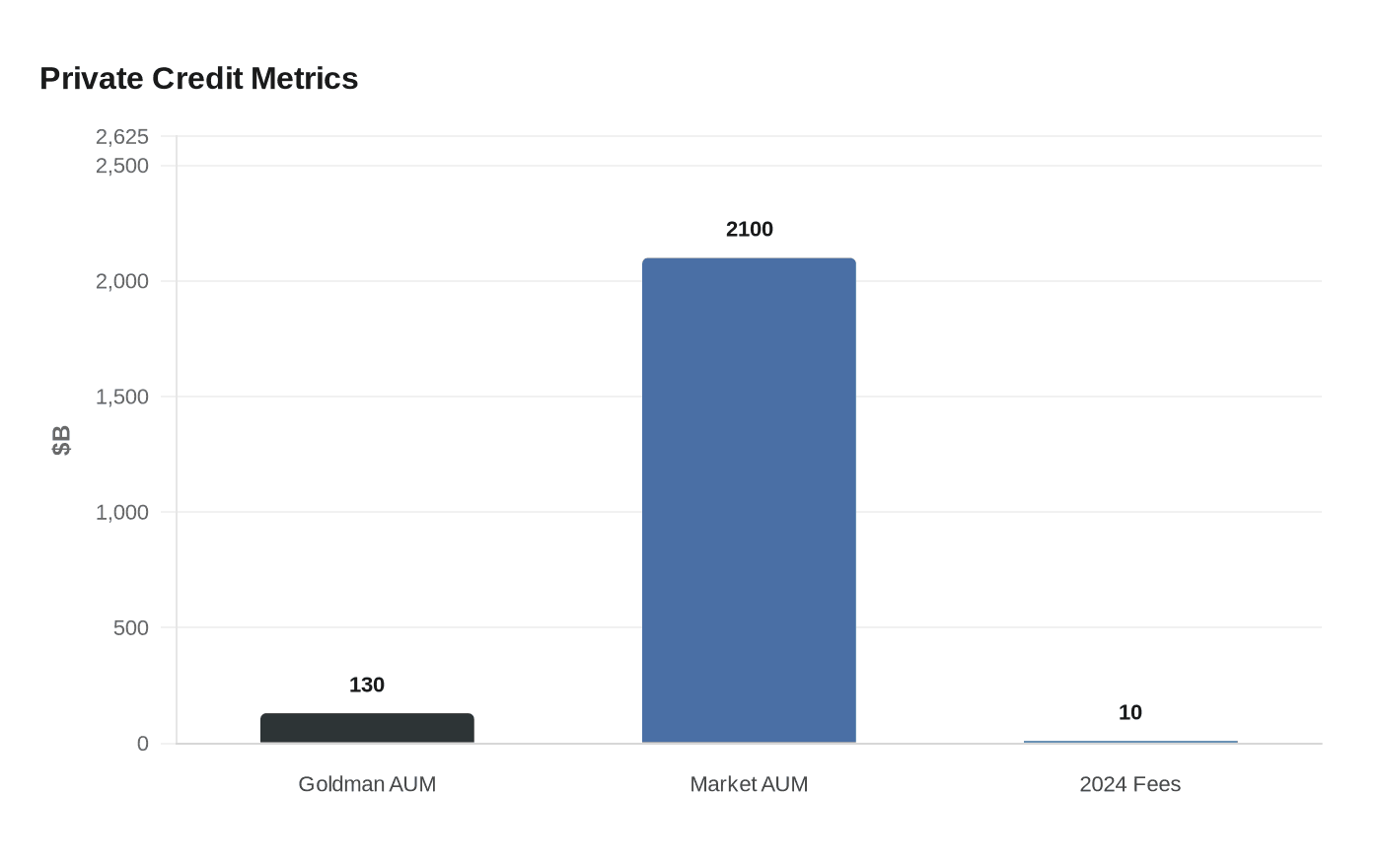

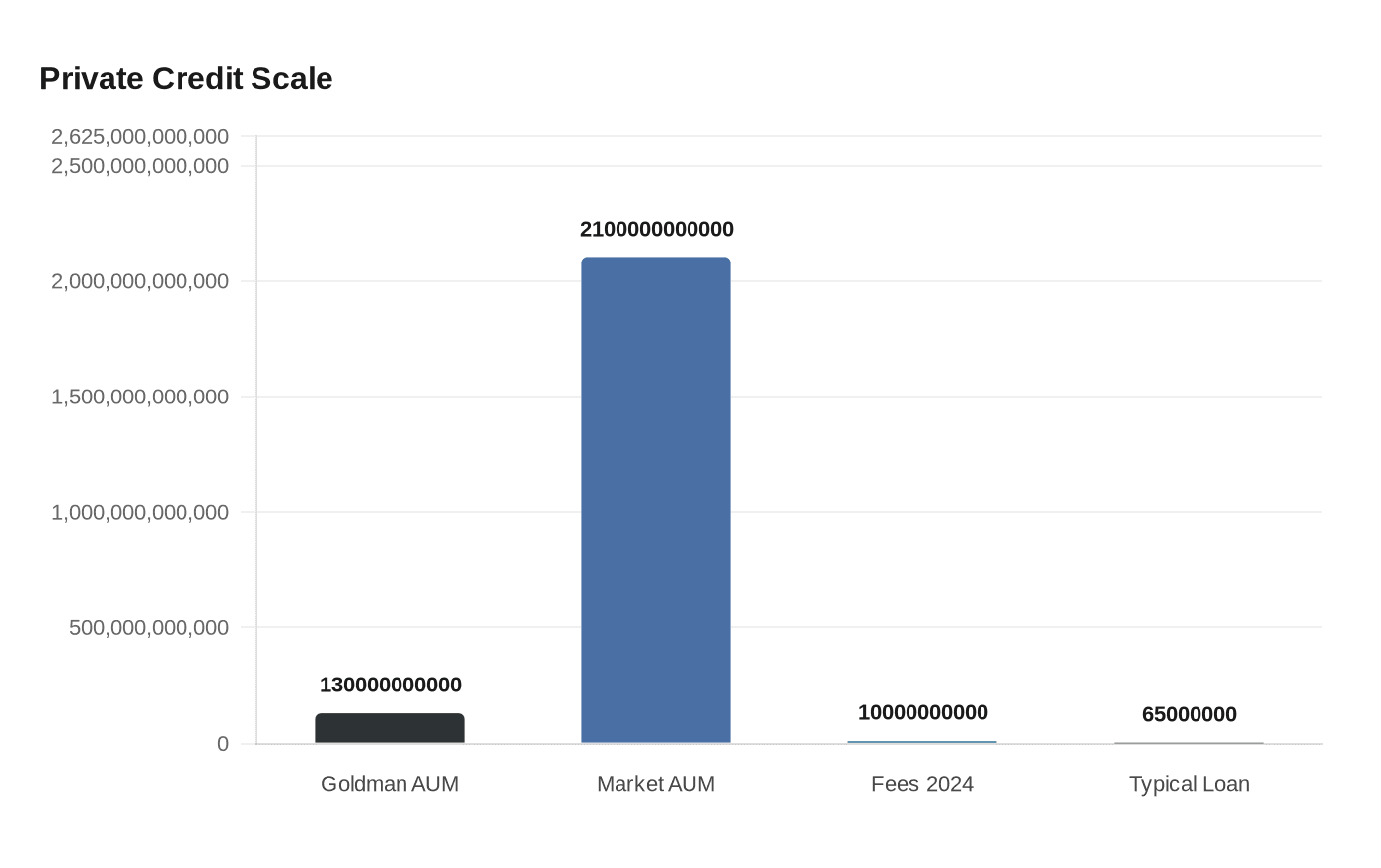

Goldman Sachs Asset Management says its private credit business now has about $130 billion in assets under management across more than 600 positions, a scale that makes the franchise hard to treat as anything other than a core growth engine. Goldman has been in private credit since 1996, which matters inside the firm because it suggests the business has already lived through multiple rate cycles, credit scares and market rewrites without losing relevance.

That history is a useful signal for employees trying to judge where Goldman’s influence is likely to deepen. Private credit sits at the intersection of asset management, lending, origination and structuring, which means it can pull in talent from different parts of the platform and reward people who can work across them. For a bank where prestige, promotion paths and bonus outcomes tend to follow the revenue mix, that combination is becoming strategically important.

Why the economics matter for the people inside the firm

Goldman’s 2024 annual report shows why businesses like private credit are drawing attention across the platform. Management and other fees, together with private banking and lending net revenues, have grown at a 12 percent compounded annual rate since 2019, and annual management and other fees topped $10 billion in 2024. That kind of fee growth is not just a corporate milestone; it is the kind of mix shift that can change which desks have influence, which teams get resourced and which skill sets are more likely to translate into stronger career mobility.

For analysts and associates, the appeal is obvious. Private credit work can be more technical than plain-vanilla lending, because the job often requires understanding how to build solutions when public markets are less attractive or less available. For VPs and managing directors, the franchise can offer a path to broader client ownership, since the product reaches across coverage, structuring and portfolio construction rather than staying boxed into one line of business.

A larger market, but not a simple one

Goldman says the private credit market now has about $2.1 trillion in assets under management, reflecting a fast expansion over the past decade and a half. The Federal Reserve’s view helps explain how the market got there: private credit traditionally served middle-market companies with a typical loan size of about $65 million, but direct lenders have increasingly been underwriting jumbo loans of $1 billion or more. That shift shows a market that is no longer confined to a niche corner of corporate finance.

The growth has been driven by several forces at once: regulatory and supervisory actions, the expansion of private equity and the appeal of private credit to both borrowers and investors. For Goldman employees, that means the business is not simply a response to one cycle, but a structural part of how financing gets arranged when traditional bank balance sheets, public bond markets or syndicated loans are less flexible.

Rising stress makes the underwriting work more valuable

Market stress is where the real test comes in, and Goldman’s own commentary is that private credit remains relatively stable. Vivek Bantwal has said the fundamentals remain strong and that systemic risk appears limited because leverage is modest and assets and liabilities are well matched. Goldman also says the business is unlikely to pose a significant financial system risk because investments are not concentrated, leverage is limited and balance-sheet timing is well aligned.

That matters because periods of volatility usually separate firms that can underwrite from firms that can only distribute. When spreads widen and financing gets tougher, the value of discipline rises. People who can judge credit quality, structure protections, manage downside and work through stressed situations become more valuable, and that tends to favor employees with experience in underwriting, restructuring and negotiation.

The practical career lesson for Goldman staff

If you work in asset management, financing or coverage, private credit is now part of the core language of the franchise. It is a product that can help clients when public-market financing is shut, expensive or simply too volatile, and it creates more chances for cross-platform collaboration than a single-purpose lending product would. That can widen opportunities for people who are comfortable moving between investing, origination and client service.

It also changes what “good performance” can look like internally. A business that generates recurring fees, supports complex client solutions and grows across market cycles can become a magnet for resources, leadership attention and the kind of visibility that often matters during compensation season. For employees thinking about long-term exits as well, private credit experience can be useful because it signals technical depth, risk judgment and familiarity with an asset class that has become central to institutional portfolios.

Institutional demand is still pointing in the same direction

Goldman Sachs Asset Management’s 2024 insurance survey found that insurers were accelerating allocations into private credit amid macroeconomic concerns and higher-for-longer rates. That is a reminder that the buyer base is not built on hype alone. Large institutional investors are still looking for yield, structure and flexibility, even as volatility rises.

For Goldman, that makes private credit less like a passing theme and more like a durable operating business. For the people inside the firm, it means the skills that matter most are likely to be the ones that combine technical underwriting, careful structuring and the judgment to navigate stress without losing discipline.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip