401(k) rollover options monday.com employees should know after leaving a job

Leaving monday.com can turn a routine exit into a tax trap. The right 401(k) move depends on fees, fund choices, and whether your next plan will take the money.

Start here: do not let the 401(k) sit in the background

The easiest mistake to make after leaving monday.com is treating your 401(k) like a loose end you can deal with later. The IRS says you generally have four paths: leave the money in the old plan, roll it into a new employer’s plan, roll it into an IRA, or cash it out. The first three keep the money tax-advantaged. Cashing out can trigger income taxes, and if you are under 59½, an early-withdrawal penalty can apply.

That matters in a workplace like monday.com, where employees may move between fast-growing SaaS teams, global roles, and the next startup or public-company stop. The company says more than 250,000 customers worldwide use its platform, which is a reminder that the business operates at scale and that employee exits often come with more moving pieces than people expect. A 401(k) should be part of your exit checklist, right alongside equity paperwork, benefits changes, and account access.

If this is your situation, start here: pick the outcome you actually want

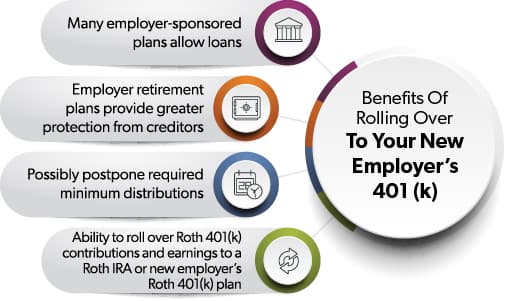

If you want the least disruption, compare the old plan with your next one before you move a dollar. If your current plan has low-cost funds, strong choices, and reasonable fees, leaving the money where it is can be a sensible move. If your new employer plan accepts incoming rollovers and has a menu you prefer, moving the money there can simplify your life.

If you want more control over investment selection, an IRA may give you a broader menu than either employer plan. If you need cash now, understand that you are giving up the tax shelter and possibly paying a penalty if you are under 59½. That is the decision most people regret, because it shrinks the account before it has more years to compound.

A simple way to think about the choice is this:

- Leave it in the old plan if the fees and funds are good and you do not need to move it.

- Roll it into a new employer’s plan if the new plan accepts rollovers and has the menu you want.

- Roll it into an IRA if you want more investing flexibility.

- Cash it out only if you truly need the money and understand the tax hit.

The 60-day clock is where many people make expensive mistakes

The IRS says a rollover can generally be completed within 60 days after you receive the distribution. It also says you can move many pre-retirement payments by direct transfer to another retirement plan or IRA, which is why the form of the transfer matters so much. Once the money leaves the plan, timing stops being a small detail and starts becoming the whole story.

That 60-day window is where people slip. If you receive the distribution and miss the deadline, what looked like a temporary move can become a taxable distribution. A direct transfer avoids that scramble because the money moves straight from one qualified account to another instead of passing through your hands first.

Why the investment menu matters more than people think

Investor.gov says 401(k) plans typically offer a choice of investment options, often various mutual funds, and that target-date funds are a common option inside these plans. It also notes that some retirement-plan investments are collective investment trusts, which are not regulated by the Securities and Exchange Commission. That is a good reminder to look beyond a fund name and ask what you are actually holding.

The behavioral trap is that people often change their investment mix after a rollover. Investor.gov warns that a rollover can lead to different investment choices, which can change the risk profile of money you spent years building. In plain terms, the move itself is not the only decision. The new menu can push you into more risk, less diversification, or higher fees if you do not compare carefully.

For monday.com employees, this is where the decision gets practical. If your current plan has a low-cost target-date fund and your next plan does not, leaving the money alone may preserve a setup you already know. If your new employer’s plan offers better fund choices or lower costs, consolidation might be the cleaner path. The key is not to assume that every rollover improves the account just because it moves the money.

What to compare before you move the balance

A rollover is not just a paperwork exercise. Before deciding, compare the fees, fund choices, and rollover flexibility in both plans. Also check whether your new employer plan will accept incoming rollovers, because not every plan does. If it does not, that can narrow your options quickly and make an IRA or a leave-it-where-it-is choice more realistic.

The most useful questions are the boring ones:

- What are the plan fees, and how do they affect my balance over time?

- What funds are actually available, including low-cost index or target-date options?

- Does the new plan accept rollovers from a former employer?

- Will I have enough control to keep the money invested the way I want?

- Is there any reason to keep the old account open for now?

Those questions matter because the wrong default choice can leave money scattered across plans, invested differently than you intended, or exposed to unnecessary tax costs.

Do not assume the old plan will always be there

The IRS says an employer is not required by law to provide a retirement plan and can terminate a plan. That is an easy detail to overlook when you leave a job, especially if you are focused on the next role and the next calendar. But it is another reason not to leave the account untouched without checking the plan rules.

If you stay in the old plan, make sure you know what happens if the employer changes providers, closes the plan, or alters the investment lineup. The account may remain available for a while, but “I will handle it later” is not a strategy. For a monday.com employee moving through a career that may include startups, scaleups, and larger public companies, the cleanest move is the one that keeps fees in check, preserves tax advantages, and avoids the cash-out trap.

The best rollover choice is usually the one you make deliberately. Once you leave a job, the clock starts, the investment menu changes, and every extra fee or tax bite works against the savings you already earned.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?