Microsoft and OpenAI loosen ties, signal more cloud flexibility for AI buyers

Microsoft and OpenAI kept Azure first, but loosened the rules around cloud access, IP and revenue sharing. For AI buyers, that means more leverage and less lock-in.

Microsoft and OpenAI rewrote the terms of their partnership on April 27, 2026, and the practical message for enterprise buyers is flexibility. OpenAI said Microsoft remains its primary cloud partner and its products will still ship first on Azure unless Microsoft cannot, or chooses not to, support the needed capabilities. But OpenAI can now serve all of its products across any cloud provider, Microsoft’s license to OpenAI intellectual property is now non-exclusive, and Microsoft will no longer pay a revenue share to OpenAI.

That matters because the AI market is moving from model access alone to infrastructure fit. Companies shopping for tools now care as much about where those tools run as what they can do. Security teams want systems that fit existing controls. Procurement wants more leverage. IT leaders want fewer dead ends if a vendor’s roadmap, cloud posture or regional hosting options do not line up with the business. The new Microsoft-OpenAI structure pushes in that direction, signaling that even the biggest AI partnerships are becoming less tied to one cloud stack and more open to multi-cloud deployment.

For monday.com, the timing is useful. The company said in February 2026 that it was reinforcing its AI-first strategy with an expanded partner program, then in March added dedicated infrastructure so external AI agents can access the platform and work alongside humans. That is exactly the kind of modularity enterprise buyers are starting to expect. If OpenAI can loosen its dependence on a single cloud without losing strategic direction, monday.com’s product teams will face more pressure to prove that work flows can move cleanly across cloud environments, model providers and customer security requirements.

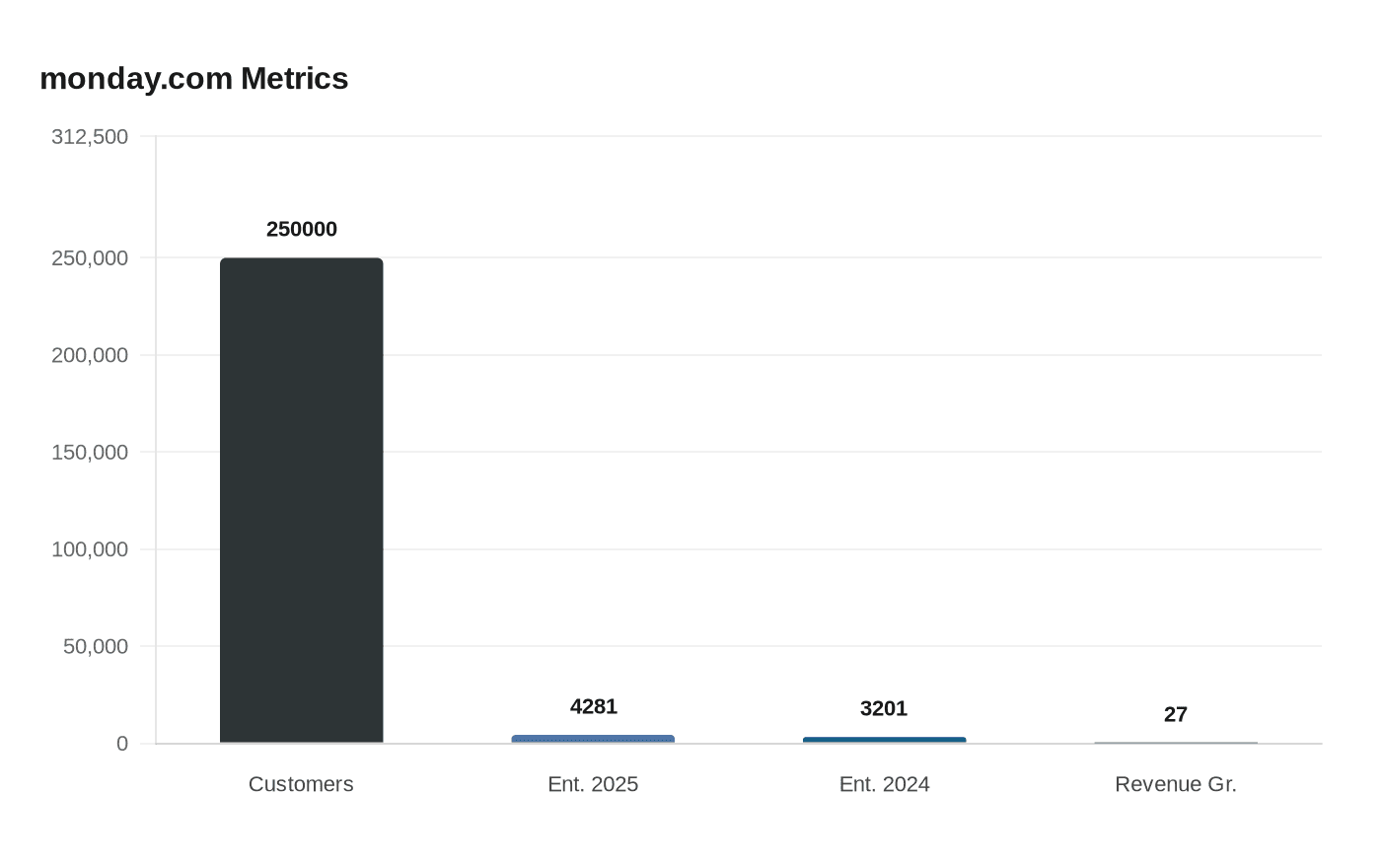

The commercial backdrop gives monday.com reason to lean into that argument. The company said it served more than 250,000 customers worldwide by early May 2026. It also reported 27% revenue growth in fiscal 2025, a 14% non-GAAP operating margin, and said customers with more than $50,000 in annual recurring revenue accounted for 41% of total ARR. Enterprise customers with more than $50,000 in ARR reached 4,281 at the end of 2025, up from 3,201 a year earlier. In a market where AI buyers are demanding less lock-in and more portability, that kind of upmarket mix makes platform flexibility a sales issue, not just a technical one.

Know something we missed? Have a correction or additional information?

Submit a Tip