Monday.com employees should know the 2026 401(k) limits

The easiest money in a monday.com paycheck is the match, but the 2026 IRS limits decide how much more can compound after that.

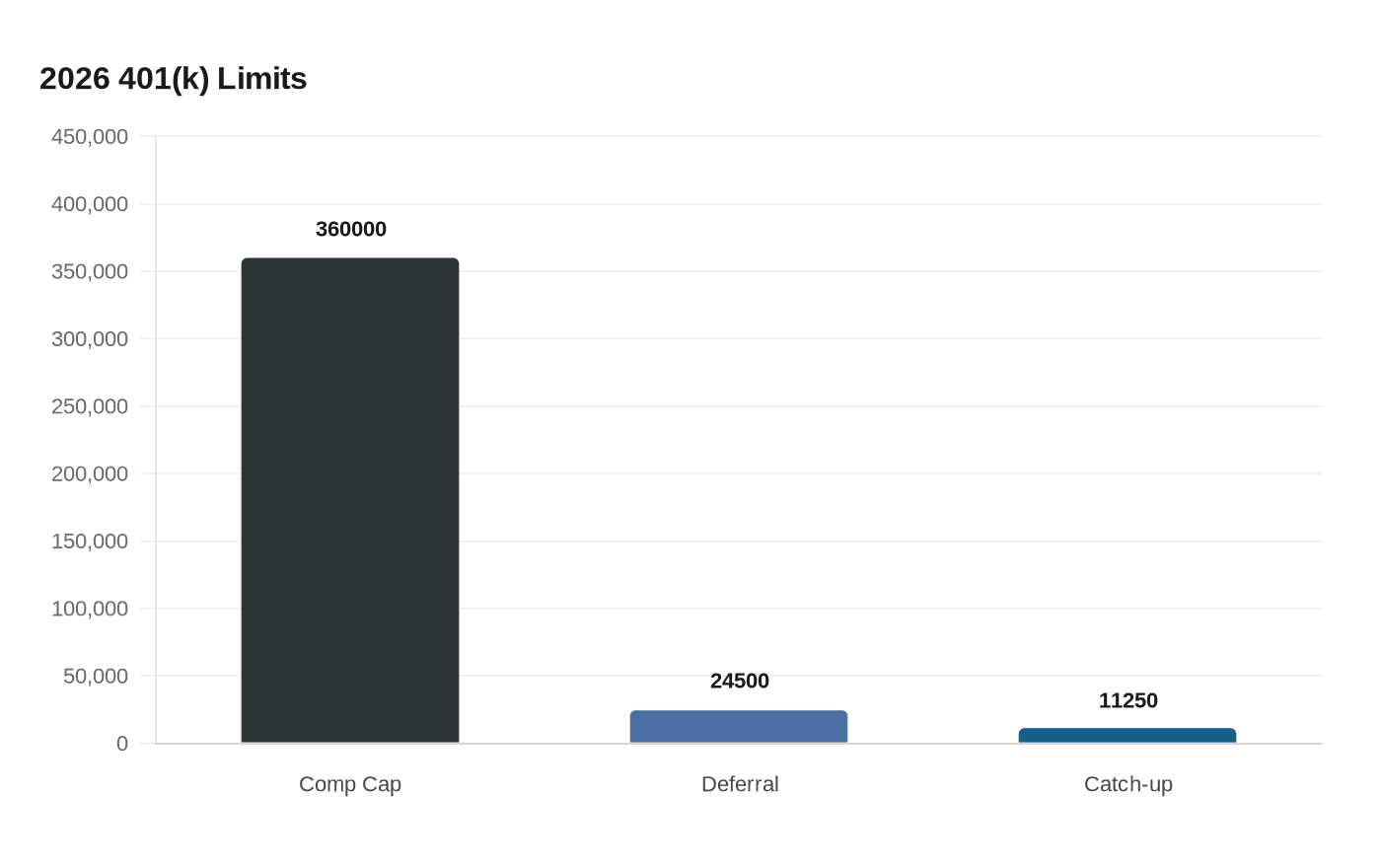

The easiest money in a monday.com paycheck is often the employer match, and the 2026 IRS rules set the ceiling for how far that money can go. The agency says the compensation limit used to calculate contributions is $360,000, while the elective deferral limit for most 401(k), 403(b), and governmental 457 plans rises to $24,500 for 2026.

That makes the first move simple: contribute enough to capture the full match before worrying about anything else. Employer matching is part of total compensation, not a perk to treat casually. For employees at a growth-stage public SaaS company like monday.com, where pay can include salary, bonus, and equity incentive participation, missing the match means leaving real money on the table and shrinking the compounding base that can grow over a long tenure.

The next decision is tax treatment. If monday.com’s plan offers both traditional pre-tax and Roth contributions, the right mix depends on your current tax rate and what your income may look like later. That matters more at a company where bonuses, equity, and promotions can shift your tax picture quickly. The IRS also announced final regulations on SECURE 2.0 catch-up rules in September 2025, including a Roth requirement for certain higher-income participants, which makes the plan design even more important for anyone trying to forecast take-home pay and retirement savings together.

Age also changes the math. The IRS says catch-up contributions remain available to eligible participants age 50 and older. Under SECURE 2.0, employees who attain age 60, 61, 62, or 63 in 2026 can make an even larger catch-up contribution, capped at $11,250 for applicable employer plans. For everyone else, the core limit is still the annual deferral cap of $24,500, and the agency raised that figure from $23,500 for 2025.

For monday.com employees, the practical mistake is not dramatic market timing or sophisticated portfolio theory. It is failing to re-check the deferral percentage after a raise, a job change, or a bigger bonus, then discovering at year-end that contributions lagged the limit. It is also easy to underestimate how much a steady match can add up for younger workers early in their careers, especially at a company that advertises competitive salary and benefits, bonus potential, and equity participation in some roles.

monday.com’s own benefits organization says it handles US health plans, 401(k), and annual open enrollment, which is exactly where this kind of planning becomes real. In a fast-moving tech career, the safest assumption is that income will change before retirement does. The smarter habit is to update the 401(k) election before the year runs away from you.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?