Monday.com growth strategy hinges on product-led adoption and expansion

PLG once meant cheap self-serve acquisition. For monday.com, the harder job now is keeping AI-rich products sticky enough that teams keep expanding inside the platform.

Product-led growth now has a tougher definition

OpenView’s original PLG playbook still explains why monday.com grew so efficiently: the product itself is supposed to drive acquisition, retention, and expansion. Blake Bartlett coined the term in 2016, and the logic was simple enough to remember but hard to execute well, build something useful enough that users adopt it first, then make it valuable enough that they pull more people in.

That framework still fits monday.com, but the stakes have changed. In an AI-saturated software market, the question is no longer only whether a user can sign up without friction. It is whether the product becomes the ongoing relationship, the place people return to, expand in, and standardize around before a competitor or a newer workflow model pulls attention away.

The scale story behind the strategy

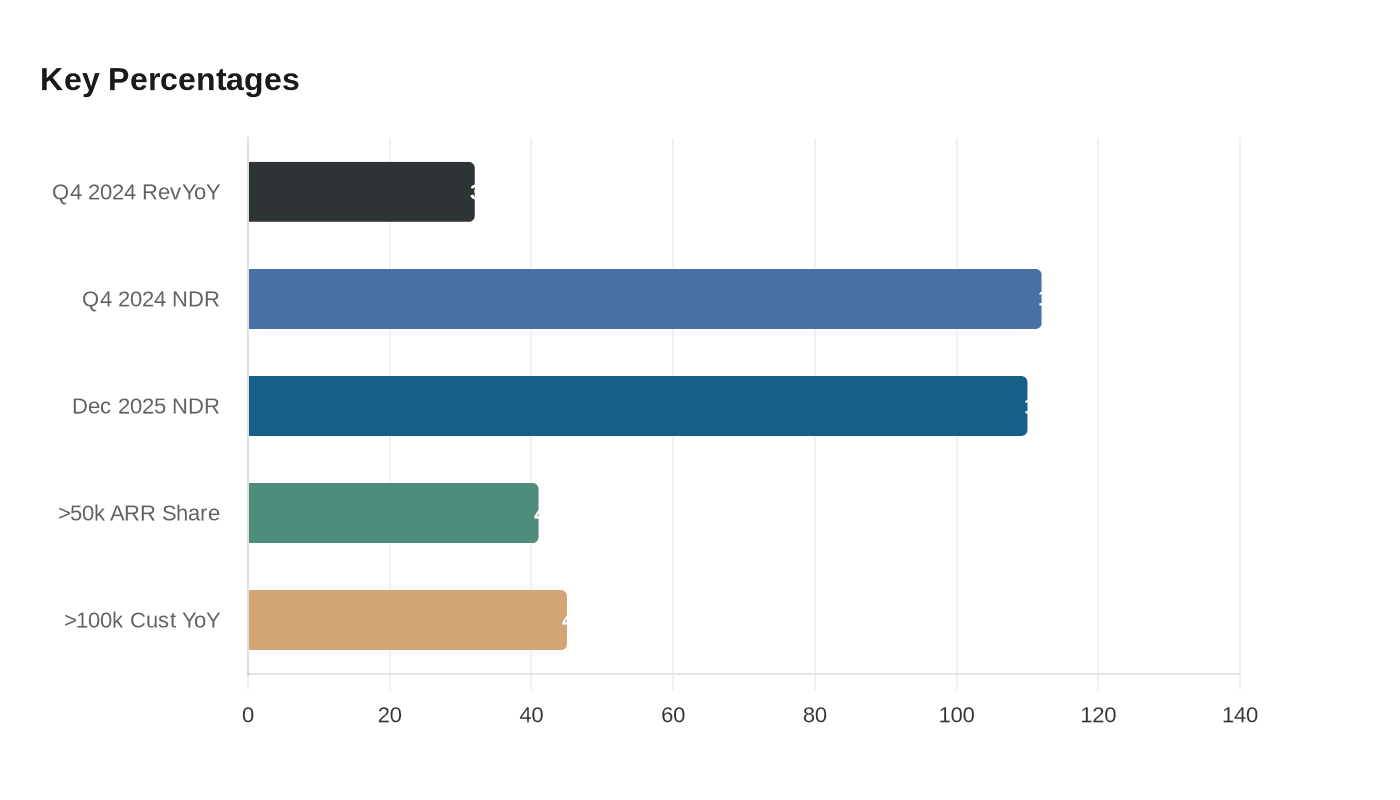

The numbers show a company that has already moved well beyond the early PLG phase. As of April 23, 2026, monday.com said more than 250,000 customers worldwide use its platform. As of December 31, 2025, it said it had 4,281 customers with more than $50,000 in annual recurring revenue, 3,155 employees, and a 110% net dollar retention rate.

That scale matters because it changes what product-led growth has to accomplish internally. For engineers, the product now has to do more than look polished or feel intuitive; it has to activate users quickly enough to turn first-time trials into repeated usage. For product managers, onboarding, collaboration, and habit formation are not soft metrics, they are the mechanics that decide whether a team stays small or becomes a repeatable account expansion.

The revenue trajectory backs that up. In the fourth quarter of 2024, monday.com reported revenue of $268.0 million, up 32% year over year, and said net dollar retention rose to 112%. The company also said it surpassed $1 billion in annual recurring revenue in 2024, a milestone that shows PLG was no longer just helping it grow, but helping it grow at scale.

AI is changing what sticky means

Monday.com’s own product story shows how PLG has evolved from a self-serve tactic into a broader platform bet. The company said it was expanding AI efforts with AI Blocks, Product Power-ups, and a Digital Workforce of AI Agents, then later introduced monday agents, monday magic, monday vibe, and monday sidekick at its Elevate customer conference. It also says its products now span work management, CRM, service, and dev on the same AI layer.

That is the crucial shift for anyone inside the company: the product no longer wins only because it is easy to start using. It has to prove that it can automate meaningful work after adoption, because the customer relationship increasingly depends on whether monday.com can stay embedded in daily workflows. In early 2025, monday service was made available to all customers and was seeing rapid adoption from both existing and new customers, which is exactly the kind of cross-sell motion that turns bottom-up usage into a broader platform foothold.

The fourth quarter of 2025 offered the clearest sign yet that the model is changing shape rather than disappearing. Revenue reached $333.9 million, up 25% year over year, and monday vibe became the fastest product to surpass $1 million in ARR in company history. The company also said customers with more than $50,000 in ARR represented 41% of total ARR, which shows the mix is moving toward larger, more embedded customers even as the product experience still does the opening work.

What the growth mix means for engineers, PMs, and sales

The middle of monday.com’s customer base tells the story best. In 2024, the company said the number of paid customers with more than $100,000 in ARR reached 1,207, up 45% from 833 a year earlier. By the second quarter of 2025, monday.com said it had added a record number of net new customers with more than $100,000 in ARR, while monday CRM had recently reached $100 million in ARR and net dollar retention among those larger customers stood at 117%.

That is the real product-led expansion loop. A user starts small, the workflow proves useful, then the company can land more modules, more teams, and more budget without needing to reset the relationship from scratch. Sales is still essential, but the job changes: the product has already done enough of the convincing that the conversation is about standardization, rollout, and how many teams can be pulled into the same system.

For engineers, that means reliability and usability are not separate from revenue strategy. For PMs, each new workflow has to reinforce the habit of coming back to monday.com instead of drifting into a one-off tool or a loosely connected AI assistant. For sales professionals, the most persuasive asset is still the product itself, because the best enterprise conversation begins after usage has already created trust.

The part that actually matters now

PLG used to be sold as the efficient way to grow software. At monday.com, the more important question is whether the product can own the relationship once users are in, especially as AI tools make it easier than ever for customers to experiment elsewhere. The company’s recent results suggest the answer is not just yes, but yes with more layers: more products, more AI, more larger customers, and more revenue concentrated in accounts that are standardizing on the platform.

That is a harder business than self-serve signups, and a more durable one if monday.com keeps getting it right. The next phase of product-led growth is not just about adoption. It is about becoming the system teams trust enough to keep expanding into, even when the software market gets noisier and faster than ever.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?