What the CFPB’s earned‑wage access guidance means for Taco Bell managers and payroll teams (practical compliance primer)

The CFPB drew a firm line on December 23, 2025: earned-wage access is not credit, but only if operators structure it correctly. Here is what Taco Bell payroll leads need to act on now.

The federal government finally drew a line

On December 23, 2025, the Consumer Financial Protection Bureau issued an advisory opinion that franchise operators and payroll administrators had been waiting on for years. The ruling affirmed that "covered" earned-wage access products fall outside the definition of credit under the Truth in Lending Act and its implementing Regulation Z, and it formally withdrew a Biden-era July 2024 proposed interpretive rule that would have subjected most EWA products to the same disclosure regime as a personal loan. For Taco Bell franchisees evaluating on-demand pay as a recruiting and retention tool, the ruling is consequential: it clears a path, but only for programs structured in a specific way. Get the structure wrong and the CFPB's consumer-protection authority, plus a patchwork of state wage laws, still apply.

What "covered" actually means, and why the definition is everything

Under the CFPB's guidance, "covered" EWA arrangements are limited to advances that do not exceed a worker's earned wages and that require repayment solely through employer-facilitated payroll deduction. That last phrase is doing most of the legal work. The 2025 advisory opinion shifts the analytical focus from the existence of an employer partnership to the method of repayment, with the Bureau emphasizing repayment through payroll deduction as the key determinant in assessing whether EWA constitutes credit. A vendor that routes repayment through a direct debit of the employee's bank account, rather than through the payroll process, falls outside the "covered" definition regardless of how the marketing material describes the product.

Covered EWA transactions must settle through "a payroll process deduction in connection with the worker's next payroll event." The advisory opinion permits one additional payroll-process deduction to correct technical or administrative errors, but that exception does not cover situations where an employer withholds garnished wages following an EWA transaction. That is a fine distinction, and one worth flagging with your payroll vendor before signing any contract.

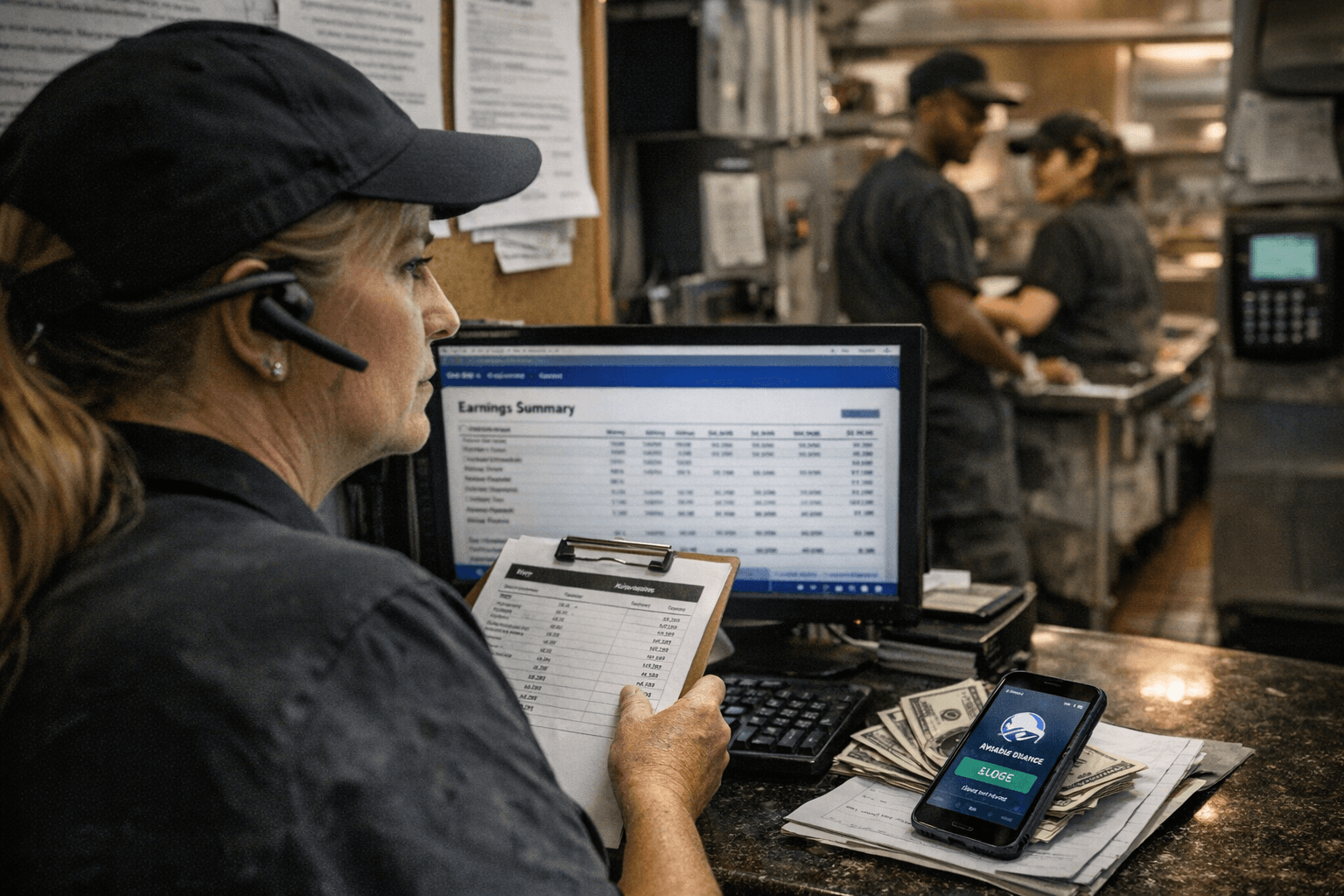

On fees: The CFPB also affirmed that optional expedited delivery fees and voluntary tips paid by workers are not "finance charges" under Regulation Z. As used in the advisory opinion, the term "payroll process deduction" is not strictly limited to an above-the-line deduction as it might appear on a paystub. That matters practically because crew members often see their paystub as the primary source of truth for what they were paid and what was deducted. Clear paystub language remains a best practice even if the fee structure escapes TILA classification.

The EWA-vs.-credit decision tree for franchise operators

Before a Taco Bell operator or payroll lead signs off on any EWA vendor, run this test sequentially:

1. Does the product advance only wages already earned, based on verified payroll data (not consumer-estimated or projected earnings)?

If no, treat as potential credit product and consult counsel before proceeding.

2. Is repayment structured exclusively through a payroll-process deduction at the next pay event, with no direct bank debit as the primary repayment mechanism?

If no, the product likely falls outside "covered" EWA.

3. Are any fees charged to the employee clearly labeled as optional expedited-delivery fees or voluntary tips, with no mandatory fee embedded in the advance itself?

If mandatory fees exist, the finance-charge analysis reopens.

4. Does the vendor clearly and conspicuously disclose the terms to the employee before each transaction, in plain language?

If no, UDAP exposure exists independent of TILA classification.

Only a product that passes all four gates earns the "covered" designation under current CFPB guidance. Anything that fails even one gate should be evaluated under full TILA and state consumer-finance requirements.

Concrete controls Taco Bell operators need to put in place

Fee caps and tip treatment. The CFPB's advisory opinion affirmed that optional expedited delivery fees and voluntary tips are not "finance charges" under TILA's Regulation Z, and that covered EWA providers are not "credit" products subject to TILA. That does not mean no limits apply. Some states impose their own fee caps on wage advances. Before launch, confirm in writing from the vendor whether their fee structure complies with the state laws governing each restaurant location, and specify in the vendor contract the maximum permissible fee per transaction and per pay period, so that a fee increase requires your written consent.

Disclosure language. Employee-facing disclosures must answer four questions in plain English: How much can I access? What does it cost me, and who pays any fees? How will the repayment appear on my paystub? Who do I contact if something goes wrong? Require the vendor to supply sample disclosure language and review it against your state's wage-statement requirements before rolling out. In tipped jurisdictions, disclosures should also clarify that EWA advances do not affect tip-pool calculations or tip credits.

Tip treatment and overtime calculations. This is the most under-examined risk in fast-food EWA deployments. Minimum wage protection means any EWA-related deduction must not reduce a worker's take-home pay below the state or federal minimum wage, and overtime compliance requires that advances not interfere with properly calculating and paying overtime. For Taco Bell crew members in jurisdictions where tip credits apply, a payroll deduction that inadvertently reduces the net wage below the tipped minimum wage floor creates wage-hour liability that no CFPB advisory opinion shields against. Map every advance-and-deduction scenario against your state's tipped minimum wage before going live.

Recordkeeping. Treat EWA transactions as payroll records. Maintain documentation of each advance, the payroll event at which it was repaid, the fee charged, and the employee's written acknowledgment of the disclosure. Retention periods should match your state's payroll-record requirements, typically three years at the federal level under the Fair Labor Standards Act, and longer in some states.

Vendor contract red flags. Watch for these provisions:

- Repayment via direct bank account debit rather than payroll-process deduction (disqualifies "covered" status)

- Mandatory fees framed as subscription charges that the employee cannot opt out of

- Advance amounts tied to projected or estimated future earnings rather than verified accrued wages

- Contract language that allows the vendor to modify fee structures without operator approval

- Absence of clear indemnification language if the vendor's product triggers regulatory action

- No audit-rights clause allowing the operator to inspect transaction records

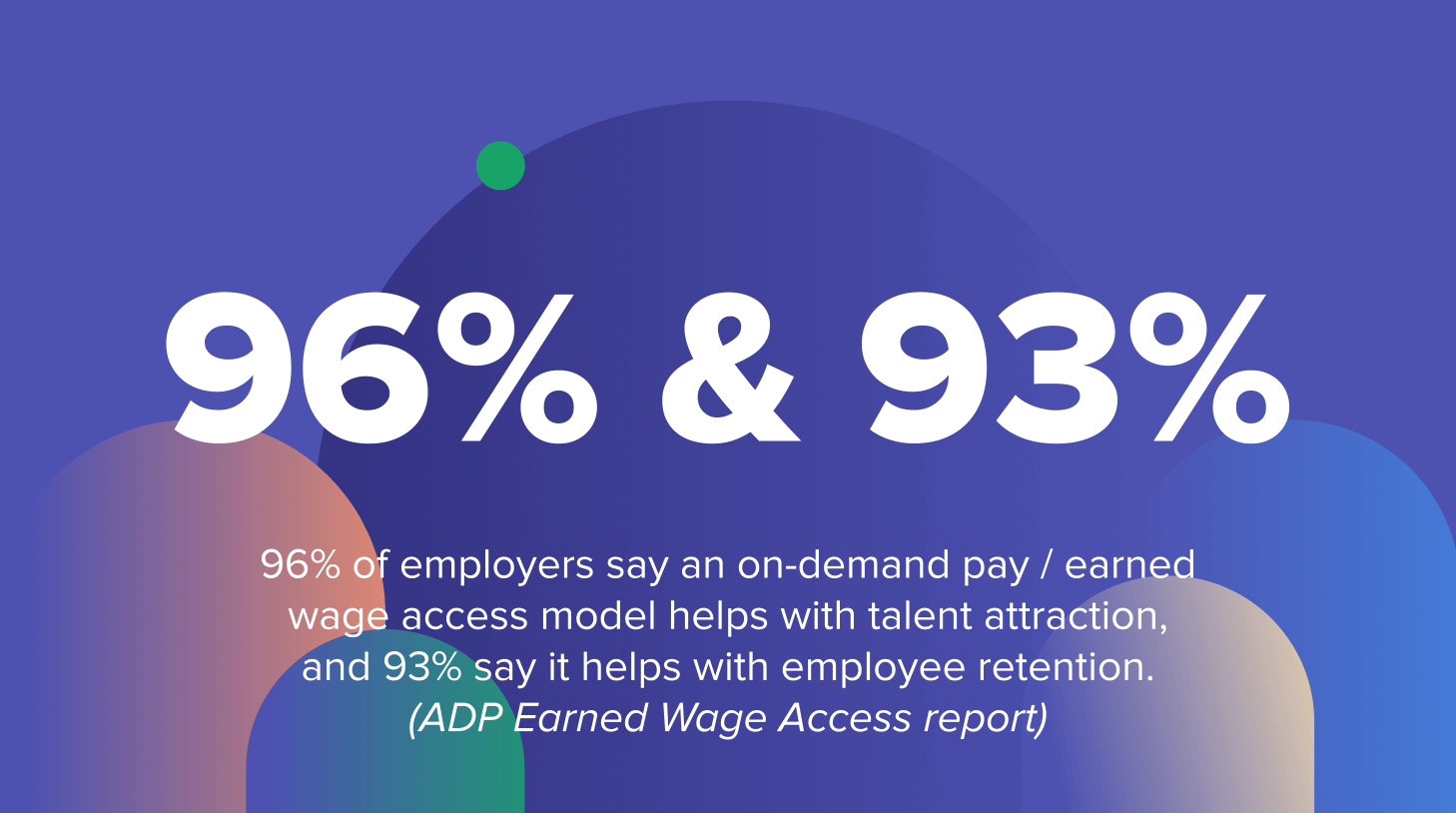

Although the advisory opinion is nonbinding and does not carry the force of law, it represents meaningful federal support for properly structured EWA programs. That "nonbinding" qualifier matters: a vendor claiming CFPB cover for a product that does not actually meet the covered-EWA criteria is a vendor that could expose your franchise to enforcement action.

One-page audit checklist: Run this before the end of the week

A general manager or franchise payroll lead can complete the following review without waiting for a formal compliance audit.

Vendor documentation

- Obtain the vendor's written compliance memo confirming the product meets covered-EWA criteria under the December 2025 advisory opinion

- Confirm the vendor's repayment mechanism is payroll-process deduction, not direct bank debit; get this in writing

- Review the vendor contract for fee-modification clauses, indemnification terms, and audit rights

- Verify the vendor's sample employee disclosure answers the four plain-English questions above

Payroll integration

- Confirm with your payroll provider how EWA advances and deductions will appear on paystubs

- Run a test payroll scenario involving an EWA advance to verify overtime calculations remain accurate

- In tipped jurisdictions: verify that tip credits and tip-pool calculations are unaffected by EWA deductions

- Confirm that no advance-plus-deduction combination can reduce net pay below your state's minimum wage floor

Employee communication

- Train shift managers on the three questions crew members are most likely to ask: What does this cost me? Will it affect my tips? What if there is a mistake?

- Designate a single point of contact (typically the GM or HR lead) for employee EWA disputes

- Post or distribute written disclosures in the language(s) spoken by your workforce before launch

State-law check

- Identify whether your state has a specific EWA licensing or registration requirement (Nevada, Missouri, and several others have enacted or proposed state EWA frameworks)

- Confirm state payroll-record retention requirements and align EWA transaction records accordingly

- If operating across multiple states, conduct this check for each state separately; the CFPB guidance does not preempt state consumer-finance law

Ongoing monitoring

- Schedule a 30-to-60-day post-launch review of employee questions and complaints to identify friction points

- Build a quarterly audit into your compliance calendar to confirm the vendor's product has not changed in ways that affect its covered-EWA status

- Document every compliance step; if a regulator asks, paper is your protection

The compliance window is now

The CFPB's December 23, 2025 advisory opinion restored and expanded the analytical framework originally established in the Bureau's 2020 advisory opinion, which had been withdrawn and subjected to a proposed interpretive rule that would have classified EWA as credit. The current guidance is more permissive than the 2024 proposal, but it is also more precise in what it requires. Franchisees who implemented EWA under older vendor agreements, before the December 2025 opinion, should review those contracts against the updated payroll-deduction and disclosure requirements. The operators who move carefully now, document their vendor due diligence, train their managers, and build in audit cycles, will be positioned to offer on-demand pay as a genuine competitive benefit rather than an unexamined liability sitting inside the payroll system.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?