Moody’s keeps negative retail outlook, Target still favored for value and convenience

Moody’s still sees a weak retail market, but Target’s edge is the faster, easier trip. More than half of its digital sales now run through stores.

Target’s real fight with shoppers is no longer just about price tags. It is about whether the trip feels easy enough to beat Walmart, Costco and every other place consumers can spend a dollar when budgets are tight.

That is the context behind Moody’s latest negative outlook for retail and apparel in 2026. The credit ratings firm said the sector still faces fragile consumption, high costs and slowing wage growth, with tariffs expected to keep weighing on apparel, footwear, big-box and department store earnings into the first half of the year. For Target, that means shoppers may keep hunting for the lowest visible price, while discretionary categories stay under pressure.

The company’s answer is to lean harder into the parts of the experience that make a trip feel worth it. Target says its stores fulfill the majority of digitally originated sales, including Order Pickup, Drive Up and Same Day Delivery. That makes store execution a core business function, not a back-room support task. A fast handoff at Drive Up, an accurate pickup order, stocked shelves and a clean front-end lane are now part of the same competitive battle.

Target’s 2025 annual report frames that battle in plain terms. The company says it is at its best when it delivers “style, design, experience and value,” and that its standard is “sharp pricing, strong in-stocks and fast fulfillment.” For store teams, that is the daily assignment. The company can spend on pricing messages and digital tools, but the guest still notices whether product is where it should be, whether a team member can solve a problem quickly, and whether checkout moves.

That is why the March 3 turnaround plan under CEO Michael Fiddelke matters so much on the floor. Target said it would add an incremental $2 billion in 2026 investments, more than $1 billion in extra capital expenditures and another $1 billion in operating investments, with total capital investment rising to about $5 billion. The money is aimed at transforming in-store floor plans and displays, increasing payroll and training, strengthening assortment and accelerating technology, including AI.

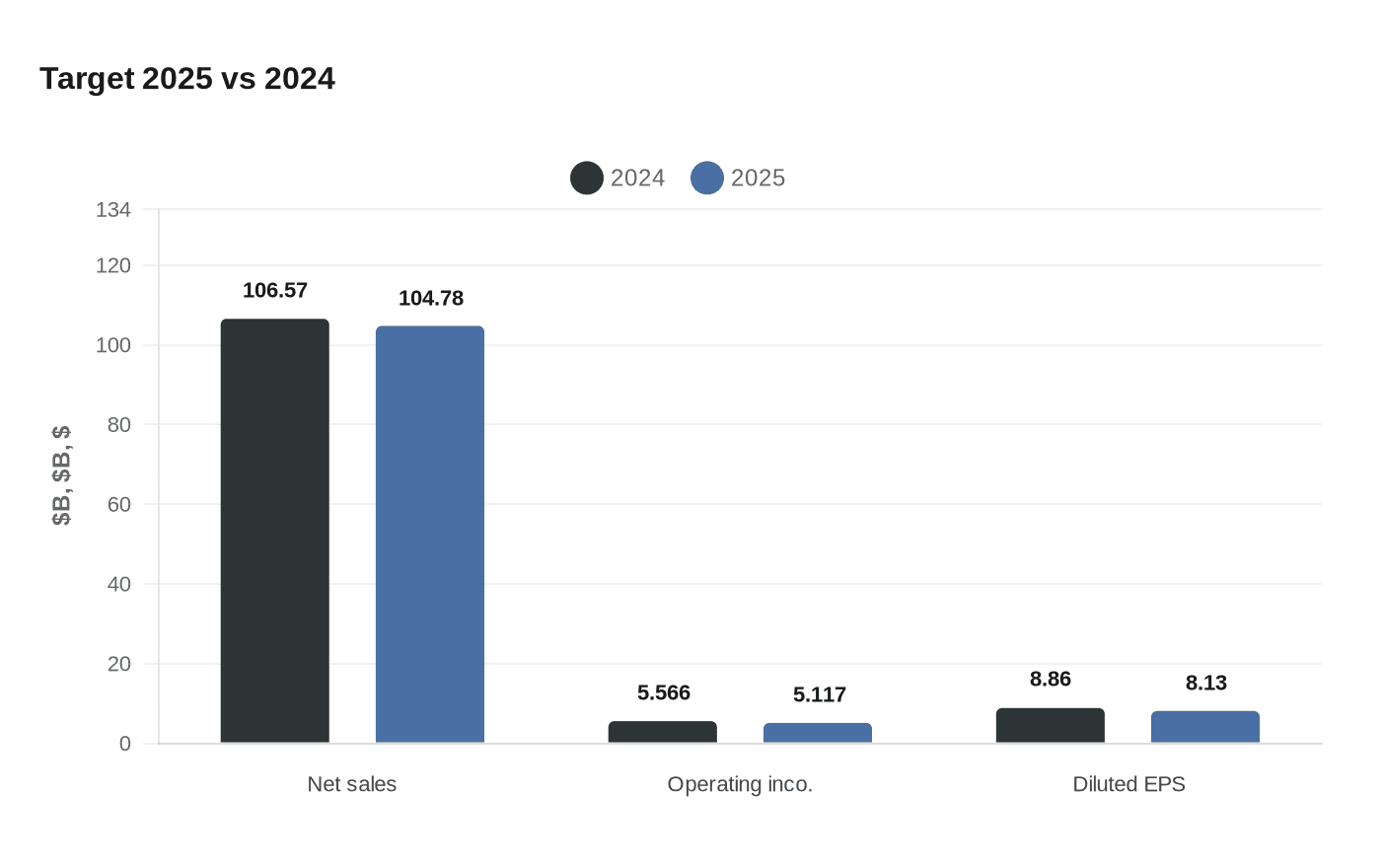

The stakes are visible in the numbers. Target’s 2025 net sales fell to $104.78 billion from $106.57 billion a year earlier. Operating income dropped to $5.117 billion from $5.566 billion, while diluted earnings per share fell to $8.13 from $8.86. Full-year adjusted EPS was $7.57, and fourth-quarter net sales were $30.5 billion.

For employees, the macro story explains the workload. Target is still being pushed to prove that convenience, speed and a better in-store experience can win customers who are comparing every trip against the cheapest option. The company’s next chapter depends on whether stores can make that promise feel real, every day.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?