Liveaboard Sailors Face Tighter Insurance Rules, More Documentation Demands

Liveaboard coverage now turns on cruising limits, paperwork, and maintenance proof. Treat insurance like another shipboard system and you improve your odds fast.

Why the policy is now part of the passage plan

A liveaboard boat does not just need a hull and rig, it needs an insurance story that makes sense to an underwriter. Jason Burke’s Practical Sailor piece makes the point plainly: for full-time cruisers and long-range sailors, marine insurance has shifted from a routine purchase to a strategic decision, and the easy, automatic coverage many owners expect is no longer the default. The market for hull and liability insurance has tightened most sharply for boats that live aboard or spend real time offshore, which means the way you document the boat, the way you cruise it, and the way you maintain it now affects whether you get covered at all.

That is the key mindset change. Insurance is no longer separate from maintenance, routing, or refit work. It sits in the same system as your rigging checks, your plumbing repairs, and the next haul-out, because a loss claim often leads straight into haul-out work, fiberglass repair, and a paper trail that has to line up with the policy.

Know where your risk is actually being placed

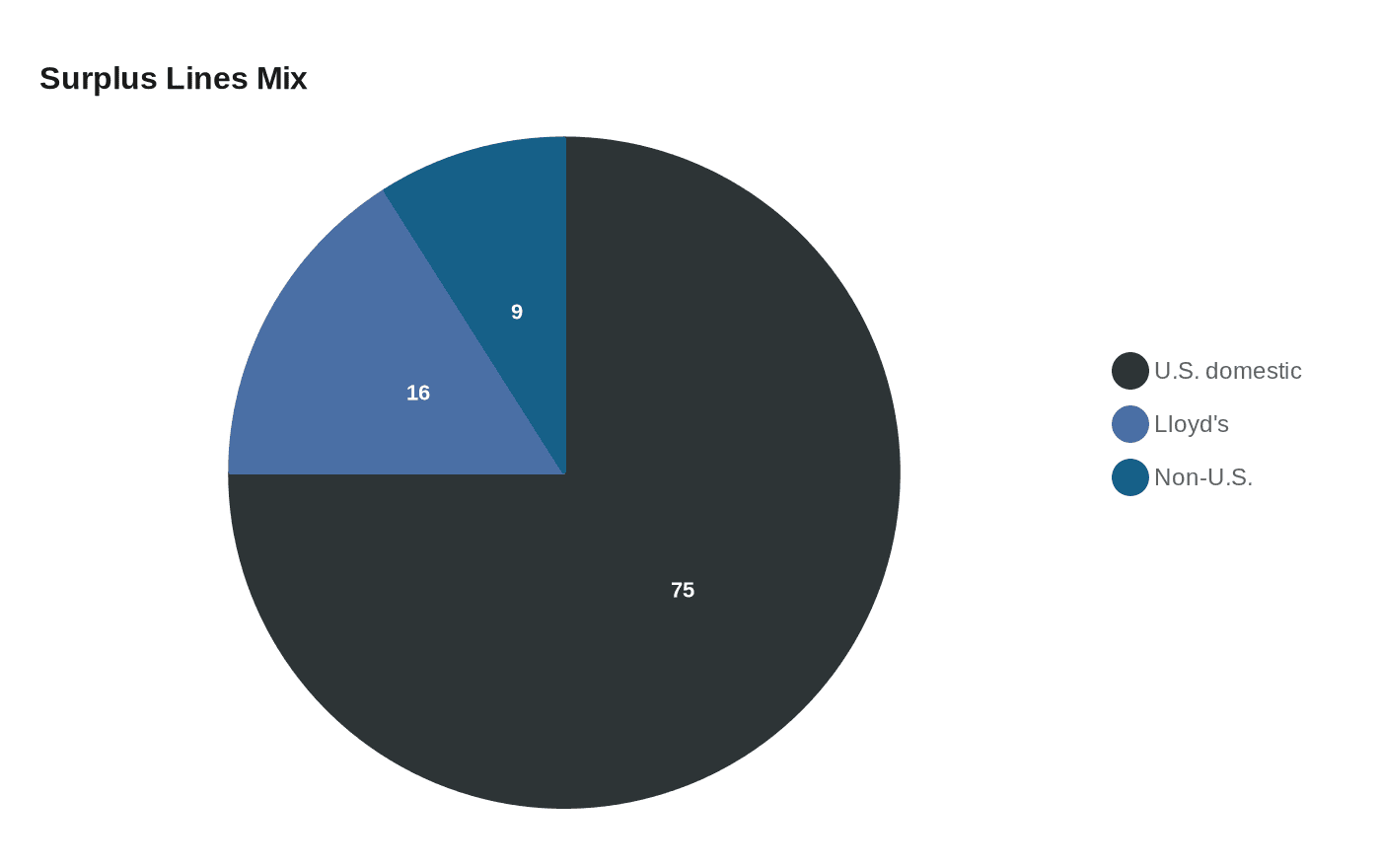

A lot of cruising sailors talk about “my insurer” as if every policy comes from one normal market. That is not how this segment works. The National Association of Insurance Commissioners says surplus lines exist for unique risks that are difficult to price with standard actuarial methods, and marine exposure often lands there. The U.S. surplus-lines market was already above $100 billion in direct premiums written in 2023 and grew to $131 billion in 2024, with U.S. domestic insurers writing 75% of the premium, Lloyd’s syndicates 16%, and non-U.S. insurers 9%.

That matters because liveaboard and offshore boats are often treated as specialty risks, not routine pleasure craft. Lloyd’s says U.S. surplus-lines marine business can be placed through approved Lloyd’s syndicates, and it also says the relevant territory for marine risk can depend on the vessel’s registration, the physical location of the property, and the insured’s residence or business establishment. In plain English, where you live, where the boat sits, and where it is flagged can all influence how the risk is written.

What that means for your application

If you want better odds, think like the underwriter. A boat that is clearly registered, clearly located, and clearly tied to a documented cruising plan is easier to place than one with vague home ports, fuzzy use patterns, and no paper trail for major work. That is especially true when the risk is being shopped through surplus lines, where the whole point is to price unusual exposure more carefully.

Survey currency is not optional theater

A current survey is not just a box to tick, it is one of the few documents that tells the insurer the boat still matches the story you are telling. For a liveaboard boat, that story needs to include condition, equipment, and any major changes since the last inspection. If you have upgraded through DIY work, the survey needs to reflect what is actually aboard, not what was there two seasons ago.

This is where owners get into trouble. A clean survey helps underwriting, but only if the repairs and upgrades are easy to verify. Keep invoices for materials, photos of the work in progress, and a simple log of what changed. A well-documented refit can help, but undocumented changes can create questions if the insurer thinks the boat now differs from the risk they agreed to cover.

DIY upgrades that help, and the ones that complicate things

Not every hands-on project works in your favor. Cleanly executed maintenance, properly documented fiberglass repairs, and sensible system replacements usually help because they show the boat is being kept in standard. The problem starts when the modification changes use, layout, or safety profile without a paper trail.

A solar install, a battery-bank upgrade, a new windvane, or a major deck penetration can all be positives if they are documented with photos, receipts, and a clear description of who did the work. They become complications when the insurer sees a significant change and no record of how it was installed, secured, or inspected. The same goes for homemade repairs that look fine from ten feet away but have no records behind them. Underwriting is not impressed by confidence; it is impressed by evidence.

Read the navigation limits like a chartplotter

The market is more cautious about where a boat may go, and those limits are contractual, not casual. If your policy draws a hard line around cruising grounds, hurricane seasons, or offshore distance, that language matters just as much as the premium. A liveaboard sailor who pushes outside the stated range can turn a valid policy into a headache exactly when the boat needs help most.

Burke’s point is that fewer carriers are willing to take on full-time offshore exposure, so the remaining policies tend to be more specific. That means you need to match the policy to the way you actually cruise, not the way you hope to cruise someday. If the plan is island-hopping, long-distance passagemaking, or living aboard through a storm season, the policy has to say so in a way the insurer accepts.

Hurricane planning is part of the underwriting conversation

BoatUS adds a useful example of how insurers now build pre-loss planning into coverage. Its hurricane haul-out benefit covers 50% of the cost, up to $1,000 per event, for professional haul-out or moving the boat in preparation for a NOAA named storm. That tells you a lot about the current market: insurers are rewarding preparation, geography-specific planning, and documented action before the storm, not just paying after the damage is done.

If you live aboard in hurricane country, the practical move is to show you have a real plan. Know your haul-out yard, your trailer or travel-lift options, your mooring backup, and your departure triggers. The more that plan is written down and tied to actual services, the easier it is to prove you are managing the risk instead of improvising at the last minute.

Mooring choice can change the insurance conversation

Where you keep the boat matters because insurers are looking at exposure, access, and the likelihood of storm damage. A protected marina slip, a well-documented mooring, or a yard with known haul-out capacity does not just make life easier, it can make the boat easier to place. That is especially true when Lloyd’s guidance says the vessel’s registration, the physical location of the property, and the insured’s residence or business location all feed into the risk picture.

So if you are choosing between a dock, a mooring ball, or a storage arrangement ashore, think beyond convenience. The best arrangement is the one you can explain clearly, support with photos or contracts, and keep consistent with the policy. A neat paper trail often matters as much as the physical setup.

Make claims easier before you ever need one

BoatUS and GEICO Marine Insurance Company say a claim may require an estimate broken down into parts and labor, plus statements, ownership documents, witness information, or diagrams depending on the loss. That is a strong clue about what you should already have in your file. If you can produce ownership paperwork instantly, show who touched the boat, and explain the damage with photos or sketches, you are making life easier for the adjuster and harder for a claim to stall.

It also explains why detailed maintenance records matter so much for liveaboards. A clean log of haul-outs, fiberglass work, gear replacements, and system checks can shorten the distance between damage and payment. The boat does not need to be museum-perfect; it needs to be documented well enough that the insurer can understand what happened and what was already in place.

The bottom line for liveaboards

BoatUS has been providing an insurance program since 1966, which is a reminder that marine insurance is nothing new. What is new is how much more selective the liveaboard and offshore corner has become, and how much more the insurer wants in writing before it will take the risk. The boats still get covered, but the owners who stay organized, keep surveys current, document refits, and respect navigation limits are the ones who look easiest to insure.

For a cruising sailor, that is the real tactical shift. Coverage is no longer something you buy once and forget. It is part of the operating plan, and the boats that fare best in this market are the ones whose paper trail is as seaworthy as their rig.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?