Alternative protein sector sees lower investment, stronger fundamentals in 2025

Capital got tighter, but the category kept building: 2025 brought cheaper production, new approvals, and real sales in plant-based and cultivated protein.

The right read on alternative protein in 2025 is not up or down

The cleanest way to read the year is to stop treating alternative protein like a single trade. The Good Food Institute’s 2026 State of the Industry series shows a sector with lower funding but sturdier operating fundamentals, and that is a very different story from the boom-bust shorthand that usually gets attached to it. Private capital cooled, yet the category kept posting measurable progress in sales, approvals, and cost reduction.

That matters because the money that did flow in 2025 looks more selective. Instead of chasing broad hype, investors and strategists were increasingly backing the hard stuff: scale-up, manufacturing efficiency, and routes to market. For anyone watching the aisle, the lab, or the bioreactor, that is the real tell. The sector is not disappearing into a funding winter. It is becoming more disciplined, more selective, and more dependent on execution.

What the GFI reports are actually measuring

GFI frames the State of the Industry series as a global snapshot of the alternative protein ecosystem. The reports synthesize company landscapes, product trends, investment and sales data, scientific advances, and public investment and regulatory updates, which makes them useful as a sector-wide benchmark rather than a single-category scorecard.

GFI also changed the naming convention in 2026 so the title now reflects the publication year while the content still covers the prior year. That sounds minor, but it matters when you are tracking trends across plant-based, fermentation-derived, and cultivated protein. The 2026 reports are really the cleanest read on what happened in 2025.

Plant-based is not dead, it is getting more conventional

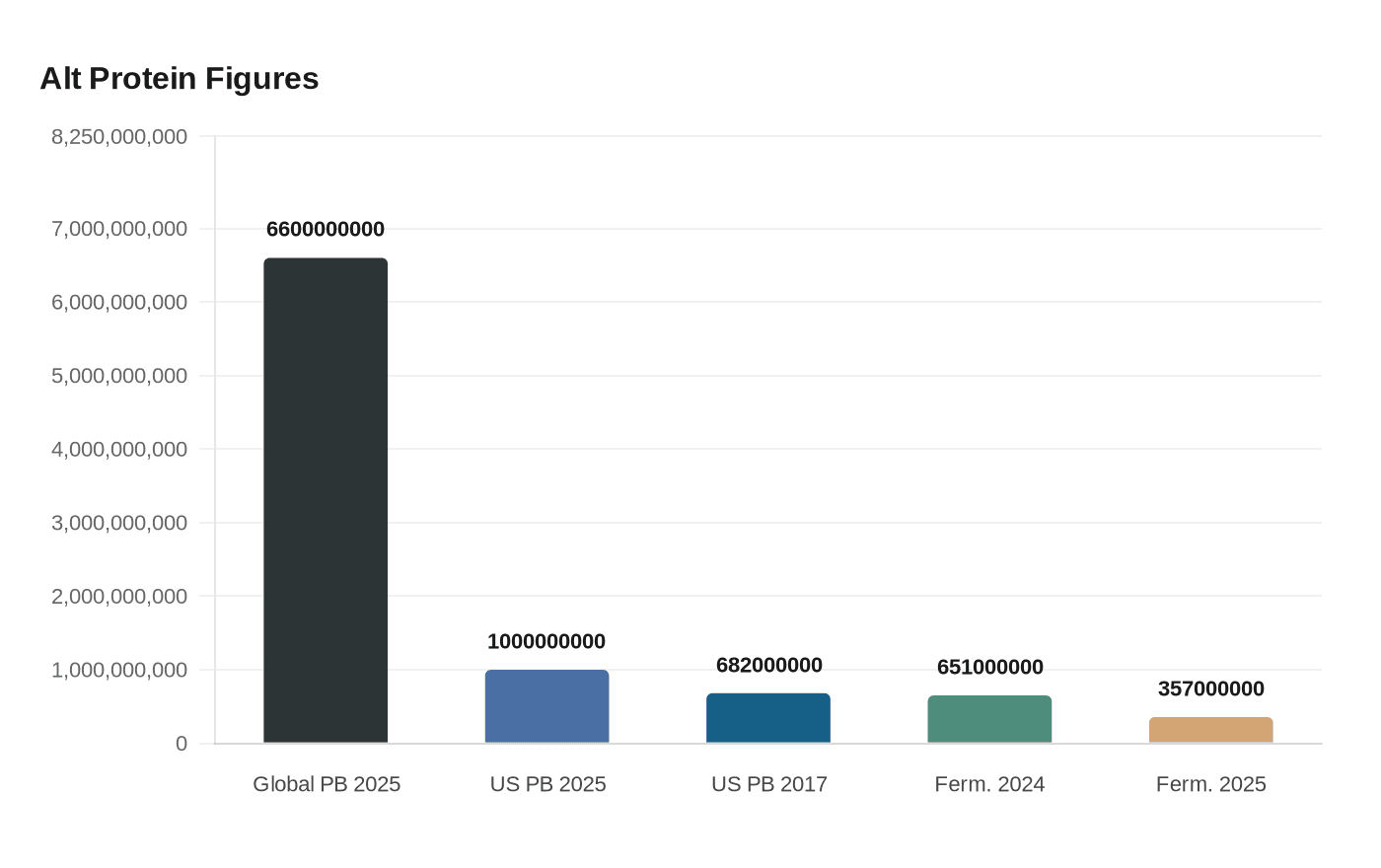

Plant-based remains the most commercially legible part of the category, and the numbers show why. GFI says global retail sales of plant-based meat and seafood reached an estimated $6.6 billion in 2025. In the United States, the plant-based meat and seafood retail market was estimated at $1.0 billion, up from $682 million in 2017.

That growth is not being driven by novelty alone. GFI says much of the expansion has come from products that more closely replicate conventional meat, which is exactly where the category has learned some hard lessons. The products that win now tend to look, cook, and fit into normal mealtime routines without demanding a consumer education campaign at every purchase.

That is the practical takeaway for buyers and CPG teams: the market is not just rewarding “plant-based” as a label. It is rewarding products that behave like the foods they are replacing, with better repeat purchase potential and a clearer place in mainstream supply chains.

Fermentation is under pressure, but not standing still

Fermentation is where the funding reset is easiest to see. Companies operating primarily in the fermentation ecosystem raised $357 million in 2025, down sharply from $651 million in 2024. That is a big drop, but it does not mean the segment has stalled. It means investors are asking for tighter economics and more credible commercialization paths.

That shift is already changing how the category is judged. Precision fermentation and adjacent companies are increasingly measured on cost, throughput, and ingredient reliability, not on story alone. If a company cannot explain how it will make enough material, at the right price, with the right spec and shelf stability, the pitch is weak no matter how elegant the science sounds.

The regulatory and naming environment is becoming a real variable too. GFI says EU policymakers agreed in March 2026 to ban the use of the word “meat” and 31 meat-related terms for fermentation-enabled, plant-based, and cultivated options, even though GFI says consumer surveys show European consumers support those terms. That creates a naming problem, a labeling problem, and ultimately a market access problem. In a category that already has to work harder to explain itself, language rules can shape what shoppers see before the product itself ever gets a chance.

Cultivated meat is still early, but the path is clearer

Cultivated meat remains the smallest investment bucket, but 2025 delivered something the sector has spent years chasing: regulatory traction. GFI says seven companies received regulatory clearance to sell different cultivated meat products during the year, and as of the 2026 report, cultivated meat could be sold in Singapore, the United States, and Australia.

That is a meaningful list because regulatory clearance is the bridge between technical proof and real commercial access. The cultivated category has always been forced to prove more than just scientific feasibility. It has to prove price progress, taste, texture, and availability, all while operating at a manufacturing standard that can hold up outside the lab.

GFI’s cultivated summary makes that framing explicit. The report is meant to evaluate progress toward competing on price, taste, and availability with conventional meat. That is the right lens. In cultivated protein, the real story is not whether a company can make something in a controlled environment. It is whether it can make enough of it, cheaply enough, consistently enough, and with enough regulatory clarity to matter.

The funding backdrop is still small relative to the ambition. GFI says privately held cultivated meat companies have raised more than $3 billion since the first disclosed investment in 2013, but in 2025 the cultivated meat and seafood slice of total alternative protein investment was just $74 million. GFI’s 2024 cultivated report said the category secured $139 million that year, so the decline is real. Even so, the growing list of clearances suggests the category is trading some speculative capital for concrete milestones.

The capital pool is smaller, but the whole category still has depth

Across alternative proteins, GFI says the sector raised $881 million in 2025, bringing total investment since 2016 to more than $19.4 billion. The mix was $450 million for plant-based companies, $357 million for fermentation companies, and $74 million for cultivated meat and seafood companies.

That breakdown tells you where conviction still lives. Plant-based remains the broadest commercial lane. Fermentation is still attracting meaningful money because its outputs can plug into multiple food and ingredient applications. Cultivated meat remains the most capital-intensive and longest-horizon bet, which is why its funding profile is so much smaller even as the science and regulation move forward.

For ingredient suppliers and CPG companies, the signal is not retreat. It is consolidation around what can actually be manufactured, sold, and defended in the market. The companies that survive this phase will be the ones that can show a path from pilot to plant, from approval to shelf, and from promise to repeatable unit economics.

What to watch next

The next phase of alternative protein will reward proof over projection. Watch for cost reductions, more manufacturing discipline, clearer regulatory access, and partnerships that show how these ingredients fit into existing supply chains. Those are the indicators that matter now, not the old hype cycle of broad category enthusiasm.

The sector’s 2025 numbers do not describe collapse. They describe maturation. Less money is chasing the story, but more of the remaining capital is going toward the work that actually decides whether alternative proteins become everyday inputs or stay as well-funded experiments.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?