Hormel beats quarterly estimates as chicken and turkey demand rises

Hormel’s sales and profit topped estimates as chicken and turkey drove organic growth, sending shares up about 8% in premarket trading.

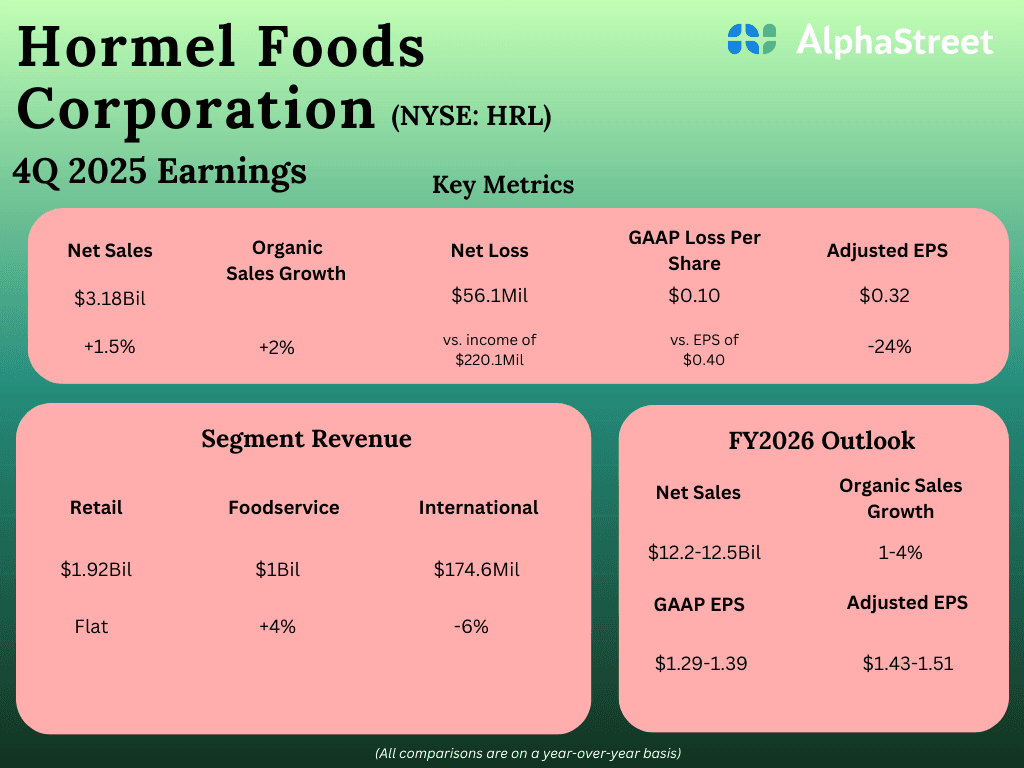

Chicken and turkey carried Hormel’s latest quarter, giving the packaged-meat company a cleaner read on what is still working in protein. Second-quarter fiscal 2026 net sales reached $2.97 billion, organic sales rose 3%, and adjusted diluted EPS came in at $0.40, enough to extend a run of six straight quarters of organic top-line growth and push the stock up about 8% in premarket trading.

The strength was not broad-based protein hype so much as a very specific mix of categories. Hormel said retail profit grew 13%, while Jennie-O ground turkey delivered another quarter of double-digit dollar sales growth. Applegate added momentum through frozen breaded chicken and chicken breakfast sausage, underscoring how poultry, not beef, is doing the heavy lifting for shoppers looking for lower-cost animal protein without giving up convenience.

That matters for a company that has spent years trying to tilt its lineup toward more value-added products. Hormel completed the sale of its whole-bird turkey business during the quarter, a move that shifts the portfolio further away from commodity exposure and toward branded items with more pricing power and less dependence on bird-by-bird economics. The divestiture included assets in Melrose and Swanville, Minnesota, which now sit with Life-Science Innovations under the Legacy Turkey name. Hormel said the sale also forced a lower full-year GAAP earnings outlook, even as it held its adjusted earnings and sales targets steady.

Management used the quarter to argue that the demand backdrop is still holding. Interim CEO Jeff Ettinger said the results gave Hormel greater confidence in delivering its full-year outlook, and President John Ghingo pointed to the company’s “protein-centric portfolio” as the engine behind the performance. That language fits the numbers. Hormel reaffirmed fiscal 2026 net sales guidance of $12.2 billion to $12.5 billion and adjusted diluted EPS guidance of $1.43 to $1.51, while updating GAAP diluted EPS guidance to $1.28 to $1.37 because of the turkey sale loss.

The bigger question for the category is whether this is a durable growth story or a temporary trade-down. Hormel’s quarter suggests consumers are still willing to pay for convenient animal protein, but they are choosing more selectively, with chicken and turkey taking share inside the protein aisle. Skippy still gives Hormel a broader protein story, but this quarter’s momentum came from poultry, and that is a useful signal for a sector still balancing inflation, budget pressure and a more promotional retail environment. The company’s first quarter already showed $3.03 billion in sales and 2% organic growth, so the second quarter did not look like a one-off bounce. It looked like a category that is still doing real work.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Know something we missed? Have a correction or additional information?

Submit a Tip