Analysts See Monday.com Trading Below Cash Value Amid SaaS Selloff

Monday.com now holds about $1.67 billion in cash and securities, or 56% of its market cap, as Wall Street argues over whether SaaS pessimism has gone too far.

Monday.com is becoming a market test of a bigger question hanging over software stocks: when a company has a huge cash cushion, growing revenue and a fast-moving AI roadmap, how much downside should the market really price in?

At $70.50 a share on April 21, monday.com’s balance sheet carried about $1.67 billion in cash and marketable securities, a sum that equals roughly 56% of its market value. That kind of reserve has led some analysts to argue the stock is trading at a discount in the broader SaaS selloff, with the business still producing the kind of revenue and margin profile that can fund product development for years.

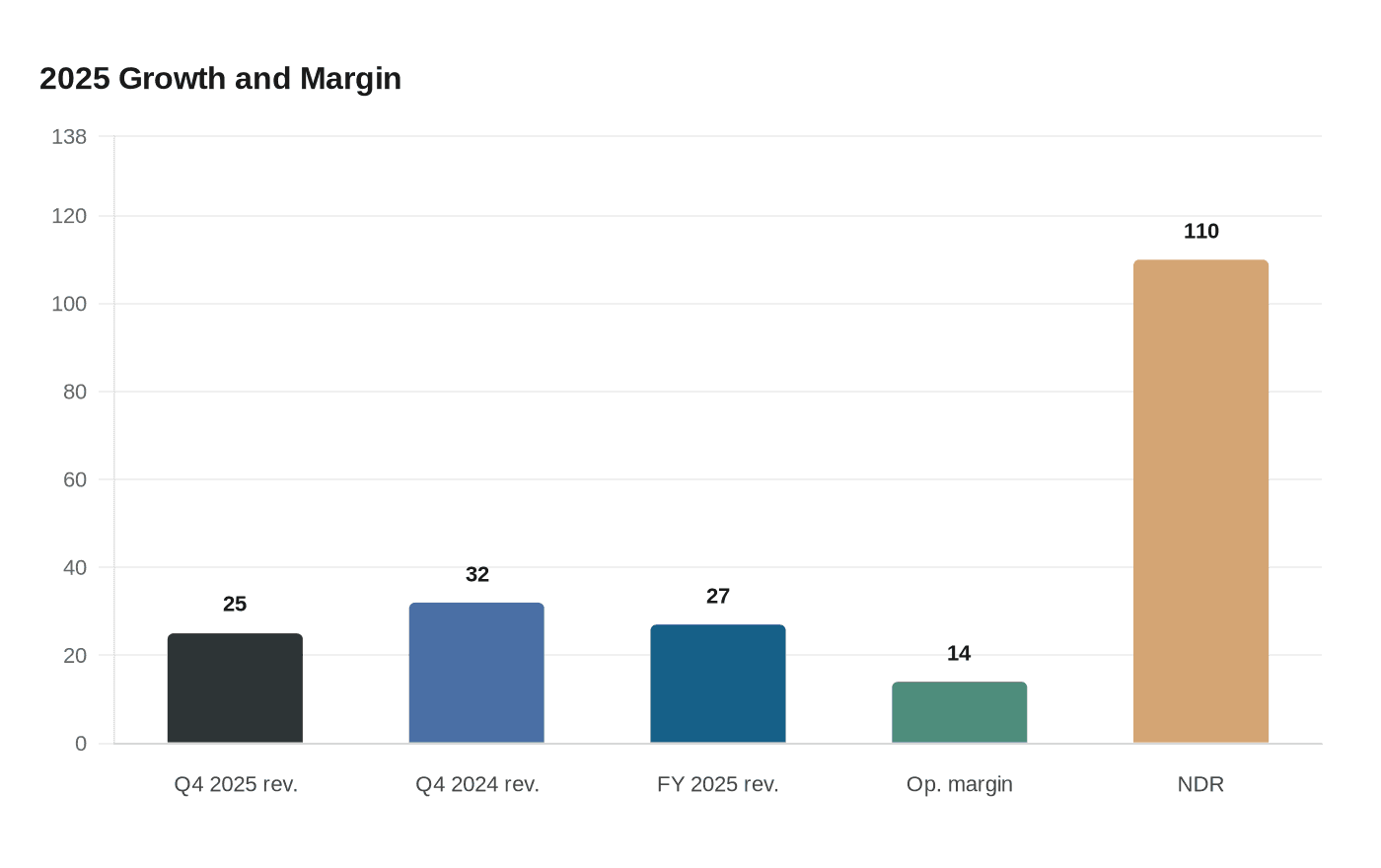

The operating numbers help explain why the debate is not just about sentiment. Monday.com said it ended 2025 with more than 250,000 customers worldwide, 110% net dollar retention, and 4,281 customers paying more than $50,000 a year in recurring revenue. Those larger accounts accounted for 41% of total annual recurring revenue in the fourth quarter, a sign that the company is still pushing deeper into enterprise workflows while keeping its self-serve roots. It also had 3,155 employees at year-end, giving the Tel Aviv-based company enough scale to keep building while rivals slow hiring or trim product bets.

The company’s growth has not stalled. Fourth-quarter 2025 revenue rose 25% from a year earlier to $333.9 million, after a 32% jump in the same quarter of 2024. Full-year revenue grew 27% in 2025, and monday.com posted a 14% non-GAAP operating margin. Monday vibe, the company’s AI product push, was its fastest product ever to reach $1 million in annual recurring revenue. For product managers and engineers inside monday.com, that is the kind of metric that turns AI from a presentation slide into an internal mandate.

Still, Wall Street has not stopped questioning whether the market is underestimating disruption risk. Bank of America downgraded monday.com to Neutral from Buy in August 2025, citing Google’s AI Overviews as a threat to web traffic and to the company’s self-serve model. Jefferies followed with a Hold rating in February 2026 and sharply cut its price target in a sector-wide review. The tension is clear: monday.com has enough cash to keep investing, but it still has to prove that AI strengthens its workflow software before cheaper, faster rivals take that leverage away.

That is why the next earnings update matters. Monday.com plans to report first-quarter 2026 results on May 11, and investors will be watching less for a clean beat than for evidence that the company can keep outbuilding the market’s doubts.

Know something we missed? Have a correction or additional information?

Submit a Tip