How Monday.com workers can lose part of their 401(k) match

A 3% 401(k) contribution can look like free money, but vesting decides whether monday.com workers keep it or leave part of it behind.

The match is not the money

A 401(k) match sounds simple until you leave the company and realize some of it may never have been yours. At monday.com, public benefit listings say the company contributes 3% of an employee’s annual gross pay, regardless of what the employee contributes. That headline number can make the benefit look richer than it really is if vesting rules delay ownership.

That is the costly misconception: employees hear “401(k) match” and assume the money is immediately theirs. In reality, the employer can set the formula, the timing, and the limits, which means two workers can both say they have a match and still end up with very different take-home retirement dollars.

How vesting changes the math

The Internal Revenue Service defines vesting as ownership. If a contribution is vested, it belongs to the worker; if it is not vested yet, the employer can take it back when the employee leaves under the plan’s rules. Qualified defined contribution plans can use immediate vesting, a three-year cliff, or a graded schedule that increases ownership over time.

That distinction matters in three concrete departure scenarios. If a monday.com employee leaves after 6 months and the company’s contribution is immediately vested, the worker keeps the full 3% employer contribution already credited. If the same employee is under a three-year cliff schedule, leaving after 6 months means none of the employer money is owned yet. After 2 years, the result depends on the schedule again: immediate vesting still means the full amount is kept, while a cliff schedule still means zero vested employer money, and a graded schedule would usually mean partial ownership.

The “after the cliff” moment is where the numbers can change fast. Under a cliff schedule, once the vesting date arrives, the employee can move from owning nothing of the employer contribution to owning all of it at once. The IRS also notes that top-heavy plans must use either three-year cliff vesting or six-year graded vesting, which is why vesting schedules vary so much from employer to employer.

Vanguard’s research adds an important reality check: more than half of 401(k) plans use vesting schedules, often as a retention tool, but vesting is not magic. It can slow exits and reward tenure, but it also means a benefit that looks generous on paper can be worth less if someone changes jobs before the vesting clock runs out.

What monday.com workers are actually looking at

monday.com’s public benefit listings say the company offers a 401(k) matching plan, and one listing says it is managed by ADP while another says TriNet. That split suggests the public summaries may reflect different reporting snapshots or plan-administration details, but the more important point for workers is unchanged: the current plan documents matter more than the marketing shorthand.

The company also describes itself as a global software company hiring to build AI-powered work products. That makes retirement benefits part of the broader compensation picture for engineers, product managers, and sales staff who may already be weighing equity, cash pay, and the pace of change in a public SaaS business. monday.com filed its 2024 Form 20-F with the Securities and Exchange Commission on March 17, 2025, and its 2025 Form 20-F on March 13, 2026, a reminder that compensation practices at a public company sit under investor and candidate scrutiny alike.

In a company like monday.com, where teams work in a fast-moving software environment and talent can move quickly, vesting is not an abstract HR footnote. It affects the realized value of compensation, especially for workers who stay long enough to build product but not long enough to cross a vesting threshold.

Why the broader labor market context matters

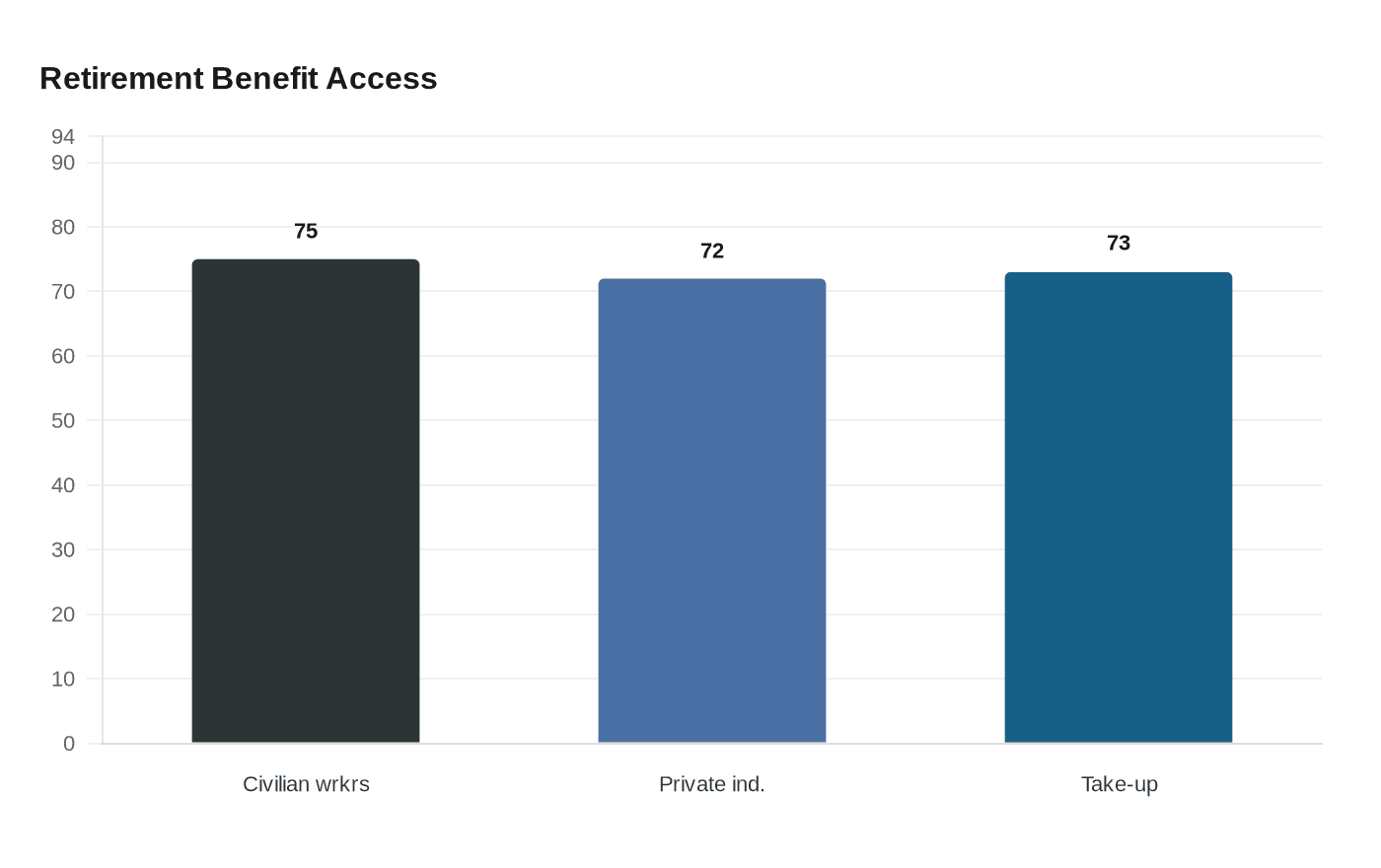

The Bureau of Labor Statistics reported that in March 2025, 75% of civilian workers had access to retirement benefits. Among private-industry workers, access was 72% and take-up was 73%, which shows that simply offering a plan does not guarantee employees are using it fully. The BLS also says access is much higher at establishments with 100 or more workers than at smaller workplaces.

That is relevant to monday.com because larger employers generally have more room to offer structured benefits, but structure is not the same as certainty. A company can advertise a retirement benefit and still leave workers exposed to vesting rules, contribution formulas, and waiting periods that shrink the real value of the package.

What to check before you count the match as yours

Before treating any employer contribution as guaranteed compensation, monday.com workers should verify four things:

- Whether the 3% company contribution is a true match or a nonelective contribution

- Whether the money is vested immediately, on a cliff schedule, or on a graded schedule

- How much of the employer contribution would be owned after 6 months, 2 years, and at the vesting milestone

- What happens if you leave before the cliff date, especially if you are mid-career and likely to move again

The headline number is only the first layer. For workers at monday.com, the real question is when the money becomes fully theirs, because that is where a generous retirement benefit turns into actual compensation.

Know something we missed? Have a correction or additional information?

Submit a Tip