monday.com stock rebounds, analysts still see 53% upside

monday.com’s rebound lifts the value of RSUs, while analysts still price in 53% more upside as AI and enterprise growth stay central.

monday.com’s stock has bounced enough to change how employees think about pay, even if nobody inside the company can control the tape. With shares around $78.01 on May 20 and an average analyst target of $119.36, Wall Street is still pricing in about 53% upside, a gap that matters most to workers whose compensation lives partly in RSUs and other equity awards.

That gap is more than a headline for engineers, product managers, and sellers. A lower share price can make equity grants feel less valuable in the moment, even when the company’s operating story is improving. A rebound can do the opposite, strengthening retention psychology and giving recruiters a better answer when candidates ask what the stock could be worth if monday.com keeps executing. The practical question for employees is not whether the market is right today, but whether the business can keep turning product adoption into a higher valuation later.

The latest quarter gave bulls enough fuel to stay constructive. monday.com reported first-quarter revenue of $351.3 million, up 24% year over year, along with GAAP operating income of $19.8 million and non-GAAP operating income of $49.0 million. Net cash from operations reached $104.7 million, adjusted free cash flow was $102.8 million, and net dollar retention held at 110%. The company also said it had 65,016 paid customers with more than 10 users as of March 31, up 7% from a year earlier, and record net adds of customers with more than $500,000 in annual recurring revenue.

Management tied that performance to the company’s current product push. Co-CEOs Roy Mann and Eran Zinman said the quarter reflected a business “executing with discipline,” while monday.com highlighted the launch of its AI Work Platform with native agents. The company also pointed to a May 6 AI product announcement and a March 23 launch of Agentalent.ai, reinforcing that the AI story is no longer a side narrative. For employees, that matters because valuation is increasingly linked to whether AI becomes a real usage driver, not just a pitch deck theme.

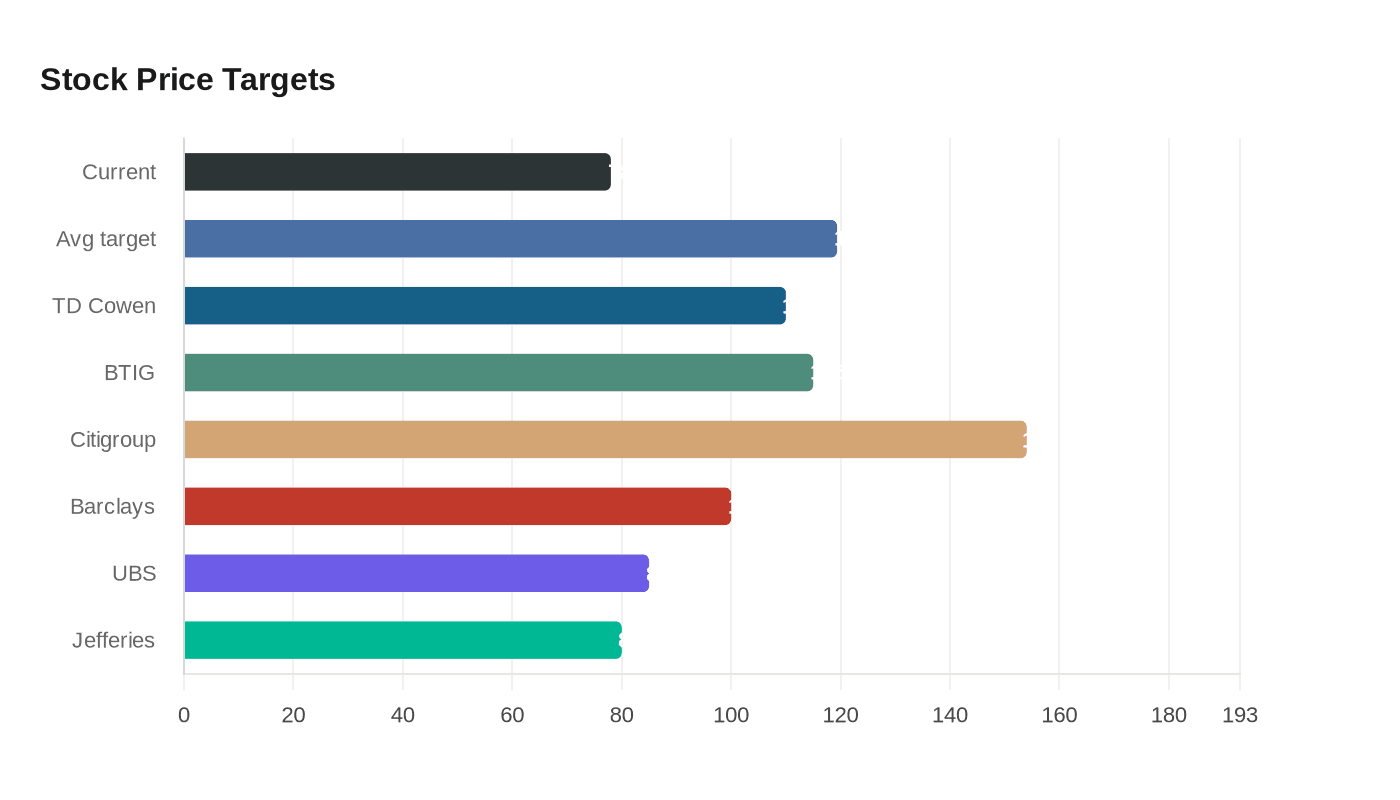

Analysts have mostly stayed on board. StockAnalysis showed 26 analysts covering monday.com with a consensus Buy rating, though recent target changes were mixed, including TD Cowen at $110, BTIG at $115, Citigroup at $154, Barclays at $100, UBS at $85, and Jefferies at $80. That split says the market is rewarding execution but still debating durability and valuation.

The stock also feeds back into the company’s own economics. monday.com has said share-based compensation expense can be highly variable and significant in future periods, which makes the share price relevant not just to morale and recruiting, but to margins as well. Against a base of more than 186,000 customers across 200-plus countries and territories, and four straight years as a Gartner Magic Quadrant leader, the company is still trying to prove that product expansion, enterprise wins, and AI adoption can support a higher rerating over time.

Know something we missed? Have a correction or additional information?

Submit a Tip