Target’s grocery push gains as value and fresh formats expand

A stronger grocery lane is reshaping Target’s local competition, and the ripple effects show up in hours, hiring, and traffic before they reach the earnings call.

The new fight around Target is happening at the edge of the parking lot

When a value grocer or discount chain opens nearby, the first thing that changes at Target is usually not the balance sheet. It is the next schedule, the next hiring round, and the next rush of guests deciding where to shop for milk, pantry staples, and dinner tonight.

That is the real story inside JLL’s latest retail and grocery outlook. The U.S. retail market entered 2026 with negative net absorption of 4.4 million square feet, vacancy held at 4.4%, and new supply stayed near historic lows. But the bigger signal for Target team members is which formats are still winning space and labor: restaurants, discount retailers, and grocery operators are expanding, while apparel and electronics are contracting more sharply.

Why this matters on the floor

For Target stores, those shifts can hit in very specific ways. When discount and grocery traffic stays strong, store leaders usually get more pressure to keep essentials in stock, keep fulfillment moving, and protect guest experience in the busiest parts of the building. That can mean more labor attention in Food & Beverage, more payroll tied to peak hours, and more competition for dependable team members who can handle fast-moving zones.

At the same time, weaker apparel and electronics trends can change how hours and attention get divided. If those departments need more markdowns, more resets, or more inventory correction, the work becomes less about selling and more about managing complexity. That is where workers can feel the squeeze: scheduling can tighten, promotional intensity can rise, and the store’s energy can shift toward value messaging instead of discretionary buys.

Grocery is still pulling two ways at once

Target’s grocery push sits in the middle of a market that is being split by shopper behavior. JLL says value-focused and premium fresh-format grocers are both gaining momentum, driven by consumer price sensitivity on one side and demand for freshness and convenience on the other. Private-label grocery products have surged 30% since 2021 to more than 21% of all grocery spending, a record $282.8 billion, and nearly half of shoppers say they actively choose store brands over name brands to save money.

That helps explain why grocery-anchored retail still has room to grow even when the broader market looks sluggish. For Target, it also clarifies where the company’s own emphasis is likely to land: store brands, fresh food, and the kind of everyday value that keeps guests coming back more often. If you work in a store with a strong grocery set, that usually means more scrutiny on fill rates, more importance placed on fast trips, and a sharper connection between what is on shelf and what guests trust the brand to deliver.

Target is leaning harder into the same lanes that are still expanding

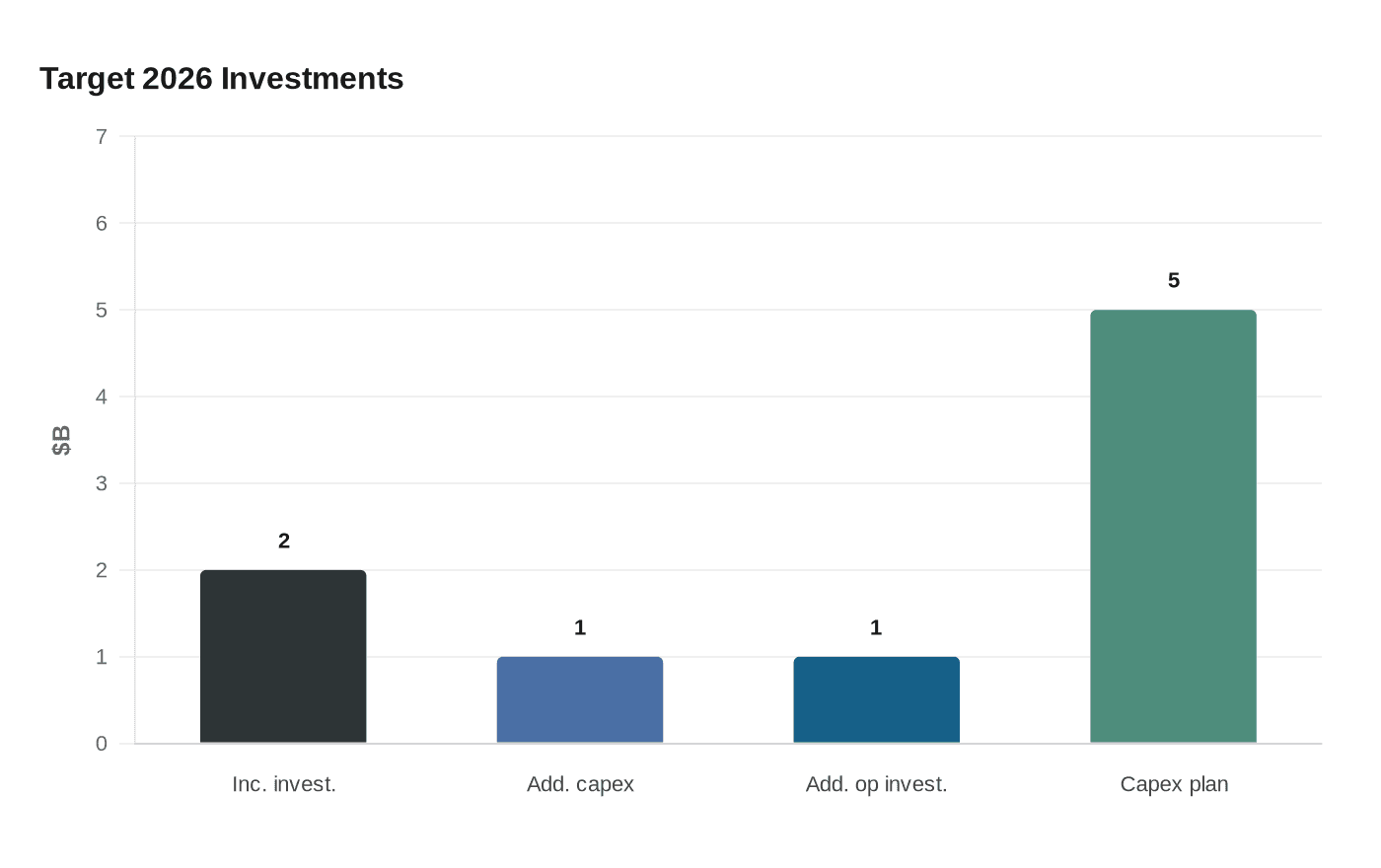

Target leadership, including Brian Cornell and Michael Fiddelke, has been signaling that it wants the chain to look and act more like the parts of retail still taking share. On March 3, 2026, the company said it would make more than $2 billion in incremental investments in 2026, including more than $1 billion in additional capital expenditures and $1 billion in additional operating investments. The company said guests should expect more change in what Target sells and how it sells it than they have in a decade, with a focus on merchandising authority, guest experience, technology, and AI.

That is not abstract for team members. More operating investment usually means more pressure on execution, training, and store-level consistency, especially if leadership wants faster trips and tighter in-stocks in the categories that matter most. Target also said it is raising capital investment plans to approximately $5 billion in 2026, with spending aimed at new stores, remodels, technology, and supply chain work. In practice, that means the chain is trying to make the selling floor, the back room, and the fulfillment path work together more smoothly.

The openings that could change your market

On March 5, 2026, Target said it plans to open more than 30 new stores this year, including its 2,000th location in Fuquay-Varina, North Carolina. The first seven openings were scheduled for March, which tells you the company is not treating growth as a distant plan but as an active rollout.

For existing stores, the local impact matters more than the national count. A nearby opening can create immediate headaches, like hiring competition for the same pool of applicants, higher wage pressure for hourly roles, and a split in customer traffic if the new box is closer to growing neighborhoods or better parking. It can also create opportunities, especially if a new location lifts brand awareness in a market, but the day-to-day effect usually lands first in scheduling, recruitment, and the way store managers protect their best performers.

Sun Belt markets deserve special attention because rent growth there is running ahead of the national average. That does not just tell landlords where demand is strongest. It also suggests where Target may face the most intense competition for sites, shoppers, and workers as expansion-heavy categories keep pushing into the same corridors.

What Target’s own sales mix says about where the company is headed

Target’s latest full-year and fourth-quarter results show why grocery and essentials are getting more weight. Food & Beverage, Beauty, and Toys posted sales growth in the fourth quarter of 2025, while Essentials and Home improved versus the third quarter. Same-day delivery through Target Circle 360 grew more than 30% in the quarter, and membership revenue more than doubled year over year.

Those numbers matter because they point to the businesses that can keep a store relevant when discretionary categories soften. Grocery and essentials drive frequency; same-day delivery deepens convenience; and membership helps lock in repeat visits. Target also guided 2026 net sales growth to around 2%, which is a reminder that the company is looking for steadier execution, not just a big top-line bounce.

What team members should watch next

- More space and staffing emphasis in Food & Beverage, fresh, and fulfillment.

- Tighter labor battles if a discount grocer opens within the same trade area.

- More value messaging on endcaps and in circulars as private label becomes more important.

- Continued pressure in apparel and electronics if those categories stay softer than essentials.

- Greater attention to training, because faster fulfillment and stronger in-stocks are now part of the job, not just the promise.

A market like this usually shows up in the store long before it shows up in headlines. Watch for:

Target has more than 14,000 corporate team members in Minnesota and more than 60,000 team members across 66 supply chain facilities in 25 states, so the store strategy is tied to a much wider labor and logistics network than the sales floor suggests. That is exactly why the grocery push matters: it is not just about what guests put in the cart. It is about which jobs get more hours, which stores get more investment, and which formats keep pulling traffic when the market gets pickier about where every dollar goes.

This article was produced by Prism’s automated news system from verified source data, official records, and press releases, then run through automated quality and moderation checks before publishing. The system is built and supervised by the people who set the standards it runs under. Read our full AI policy.

Did this article answer your question?